ZKB article on changes to imputed rental values in the Canton of Zurich:

New imputed rental values in the Canton of Zurich

November 26, 2024

For the 2026 tax period, homeowners in the canton of Zurich will receive a new assessment of their imputed rental value. However, the impact of the new system on their tax bill can vary greatly depending on the location and age of the property. We’ve done the math.

Good news for a quarter of property owners: Their imputed rental value is expected to fall by 2026. (Illustration: JoosWolfangel)

Property owners are concerned about the imputed rental value. This has made the Swiss-wide debate about abolishing the imputed rental value all the more tense in recent years. Following the discussions in parliament, it seems increasingly likely that the much-discussed tax will be abolished in the coming years.

Against the backdrop of this discussion, property owners in the canton of Zurich may have reacted with particular surprise to the headline that has been circulating for several months: The canton will update imputed rental values starting with the 2026 tax year. The adjustment was necessary because the existing calculation basis dates back to 2009, and property values and rents have increased significantly since then. Uncertainty about the revaluation is therefore considerable. The canton has now presented the public with new directives on imputed rental value taxation. They allow us to get to the bottom of owners’ pressing questions. Which property owners will have to bear the highest increase in their tax bill? Are owners of older properties at a disadvantage because they have experienced larger increases in value since their purchase? We have examined the new directive and simulated how the imputed rental value will change for every owner-occupied home (single-family homes and condominiums) in the canton of Zurich .

Rising land values are the main drivers of imputed rental value growth

Since the imputed rental value is fictitious, it is derived using a formula. The calculation is based on two components: the current construction value and the land value of the property. The land value is calculated, simplified, by multiplying the property size by the site value of the property per square meter.

The imputed rental value is derived from the land value and the building value

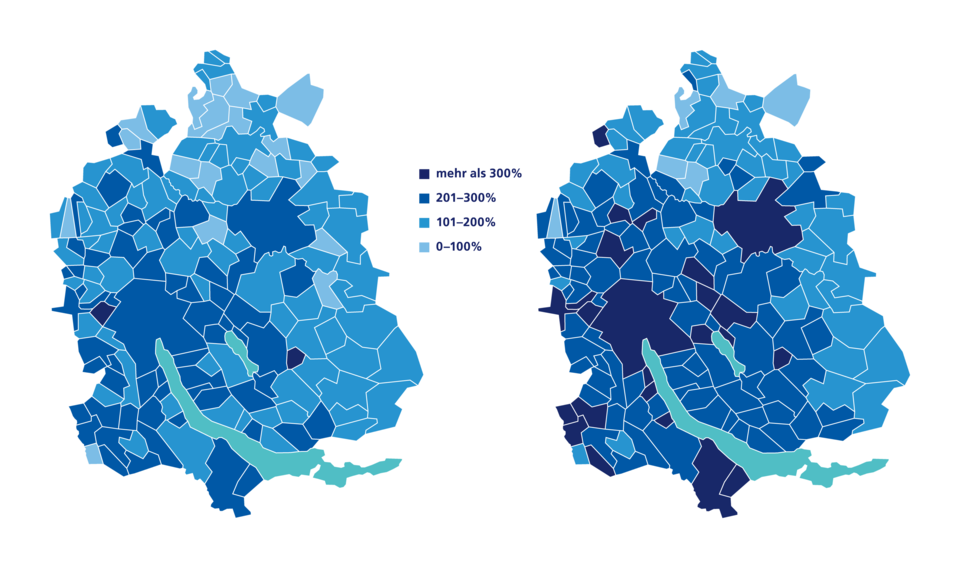

The Canton of Zurich has adjusted its location values for the 2026 tax year. Separate values are reported for single-family homes and condominiums. In recent years, the supply of owner-occupied properties has not been able to keep pace with the additional demand, which has driven up real estate prices and thus land values. This applies to both single-family homes and condominiums, where land values have risen even more sharply due to increasing popularity and more central locations. Condominiums in the city of Zurich saw a particularly significant increase, with location values rising by an average of almost 480 percent. The land value of condominiums in municipalities such as Winterthur and Kilchberg has also increased significantly. These growth rates may alarm some condominium owners. However, the land value, like the value of the building, only contributes a certain proportion to the imputed rental value. Therefore, a tripling of the land value does not automatically mean a tripling of the imputed rental value.

Land value: expensive land

Average increase in land values of single-family homes (left) and condominiums (right) after the new directive 2026

Sources: Canton of Zurich, Zurich Cantonal Bank

Owners of older properties benefit from lower building values

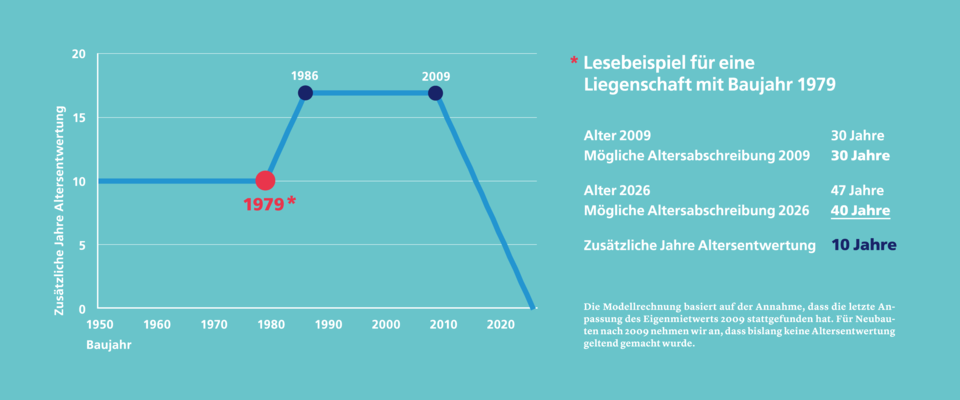

In addition to the land value, which will increase following the tax reform, the imputed rental value depends on the building value of the property, the so-called time-based construction value. For the calculation, the replacement value of the property according to the building insurance is depreciated using an age factor. Currently, property owners are allowed to claim an age-related depreciation of 1 percent per year for aging up to 2009, with a maximum of 30 years being credited. For example, a single-family home built in 1984 was already 25 years old in 2009, which corresponds to a creditable age-related depreciation of 25 percent. With the new tax regulation, an age-related depreciation can now be claimed up to 2026 for a building age of up to 40 years. For the example house, a new age-related depreciation of 40 percent would now be credited, as it will already be 42 years old in 2026. This means that 15 additional years are creditable due to the new regulation. The situation is less positive for a condominium built in 2022, for example. Previously, no age-related depreciation could be claimed here. Now, four additional years will be possible. The new building values are therefore welcome news for owners of older properties. Specifically, owner-occupied properties built between 1986 and 2009 enjoy the greatest additional age-related depreciation (see chart below). Those who recently moved into their newly built home are unlikely to benefit from additional depreciation on the building value. This leads to a surprising result: Owners of older properties, who have enjoyed the greatest increase in value in terms of building value, are in a better position than new owners of new buildings. In addition to the age-related depreciation, it is often overlooked that the assessment of the imputed rental value for new buildings was also based on old data.

Time-based construction value: New buildings at a disadvantage

Additional creditable years Age depreciation according to year of construction

Source: Zurich Cantonal Bank

Moderate increase in imputed rental values for most – some even pay less

We have estimated how the imputed rental value will change for all owner-occupied properties in the canton due to the adjusted location values and the changed age-related depreciation. Despite the sharp increase in land values, the results, as the bar chart below shows, suggest a surprising all-clear for most owners. Residents of around half of the properties expect an increase in their imputed rental value of more than 5 percent. On average, it is +14 percent for single-family homes and +19 percent for condominiums. In our estimate, the residents of one in five properties will be affected by an increase in their imputed rental value of more than 15 percent. 27 percent (single-family homes) and 31 percent (single-family houses) can view the reform with more confidence, as they do not have to expect a significant change in their imputed rental value. Another pleasant surprise is that the property owners of the remaining quarter actually have reason to be happy: their imputed rental value is expected to decrease.

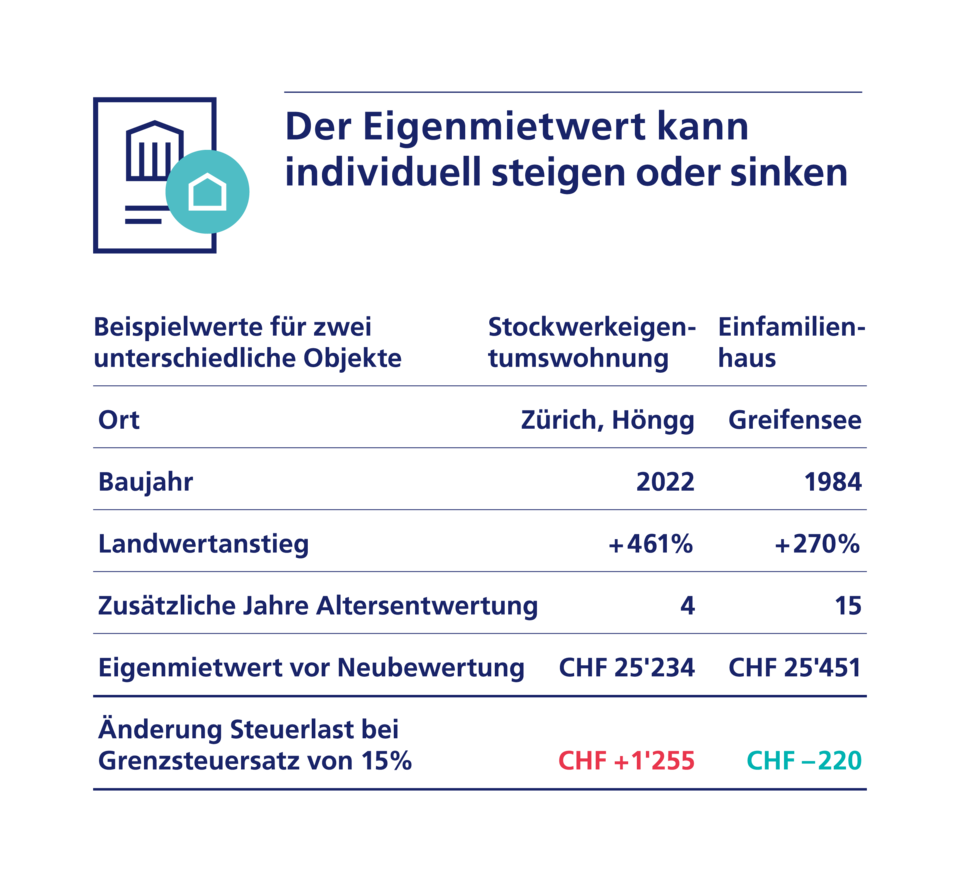

Two typical examples illustrate why some owners pay a higher amount while others can even expect a reduction in their imputed rental value. For an example apartment in the Zurich district of Höngg, built in 2022, the imputed rental value will soon rise by around 30 percent. At a typical marginal tax rate of 15 percent, this increase would mean an annual tax increase of well over CHF 1,250 – a paradoxical development in the eyes of owners, especially since many hope for the imputed rental value to be abolished soon. The increase is primarily caused by the significantly increased land value. However, the owners of an example house in Greifensee, built in 1984, can breathe a sigh of relief. Since the land value here is not increasing too sharply and, in addition, a significantly higher age-related depreciation can be claimed, the imputed rental value will actually decrease slightly.

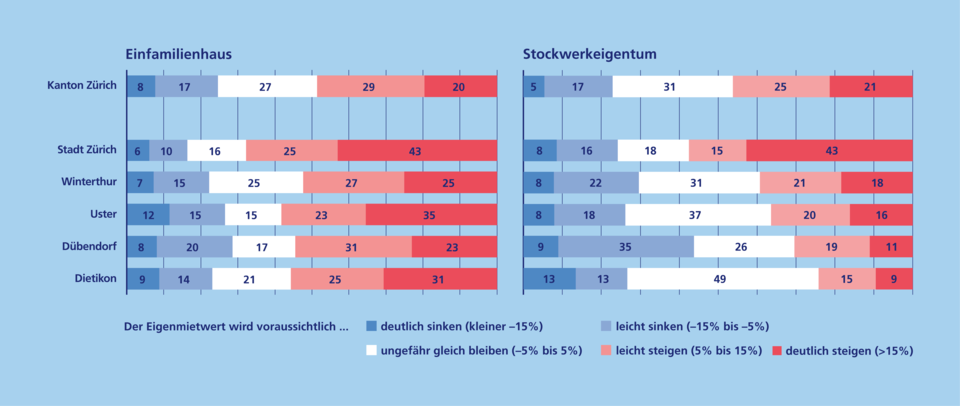

Generally, imputed rental values tend to rise primarily in metropolitan areas. The figure below illustrates this finding for the canton’s five largest municipalities. The city of Zurich stands out in particular. The imputed rental values of the city’s rare single-family homes and condominiums are increasing for a large proportion of them. Tax practice here is thus closer to reality, which not only property owners have noticed: Rent prices in the canton’s largest city have risen more sharply in recent years than in the surrounding areas. Surprisingly, imputed rental values for condominiums – with the exception of the city of Zurich – have changed less than for single-family homes, even though land values for apartments are rising particularly sharply. However, the effect of the sharp rise in land values is mitigated by the fact that the proportion of land per apartment is small. Many condominium owners in large apartment buildings in Dübendorf also benefit from this phenomenon, as their imputed rental values are less strongly influenced by land values and thus fall more frequently.

Depending on the municipality, the imputed rental values develop differently

Percentage of single-family homes and condominiums where the imputed rental value decreases, remains the same or increases in the simulation calculation, in percent

Source: Zurich Cantonal Bank

Not so bad?

All in all, there is no cause for undue concern for most property owners who were surprised by the announcement of higher imputed rental values. Anyone who also feels that the determined imputed rental value is too high can request an individual assessment of the achievable market rent. This ensures that the determined imputed rental value is between 60 and 70 percent of this market rent. A hardship rule was also announced, which should provide relief in the special case of excessive living costs. Property owners facing a significant tax increase can also look hopefully to the federal government in Bern. With a bit of luck, the imputed rental value will soon be abolished for good.

1 The model calculation provides an indication of how the imputed rental value will change. It is based on information on location classes, land area, and building volume. In individual cases, the result may therefore differ from the actual increase in imputed rental value determined by the tax office.