How does this work in practice ? since currently the Swiss pension arrives at a YOUNGER age than the UK ?

So when the Swiss start paying you a pension (and you are obliged to sign up to Swiss insurance), for the UK you are still “working age” and cannot get this confirmation.

So what happens if you get the Swiss pension first, then another pension where you have contributed for more years?

The difference is that the person in question only has a UK pension so it’s a totally different situation.

This is the link to the Swiss Government organisation who are supposed to advise you on this topic of which health insurance you must pay when you move to the UK with pensions from different countries

The original poster will have both a Swiss & a UK pension, same with Media, so an interesting question & one worth answering

Yes, but if you are still working and living in the UK, you’d be entitled to be covered by the UK would you not?

Both will have been taken into account in the initial calculation - the calculation is to determine how to maximise your contribution of your life time, not a point in time.

Since in my case the Swiss one can be taken 4 years before the UK one, I don’t live in Switzerland or the UK… The Swiss pension will be based on my 20 years of Swiss contributions & my UK one based on 35 years of contributions. No calculation or communication between them will occur as I claim the Swiss one from CH & The UK one from the UK.

I have to have health insurance from CH & then when I get a UK pension as it’s more years the UK should be responsible for my healthcare from age 67

1 Like

I keep stumbling upon AHV pension and health insurance bundle, can someone please clarify, when person is not living in EU/Switzerland and wants to receive his AHV pension it is not obligatory swiss health insurance, right? i read here

Bezügerinnen und Bezüger einer Schweizer Rente mit Wohnsitz in der EU/EFTA oder im Vereinigten Königreich (UK) sind in der Schweiz versicherungspflichtig. Liegt der Wohnsitz ausserhalb EU/EFTA/UK, sind sie nicht in der Schweiz, sondern in ihrem Wohnsitzstaat krankenversicherungspflichtig.

It is because Switzertrald is responsible for your health care, price dependent ant on which country you live in.

If you google “Grundversicherungsprämien EU/EFTA/UK” you get this PDF that shows various companies prices in each country https://www.priminfo.admin.ch/downloads/gesamtbericht_eu.pdf

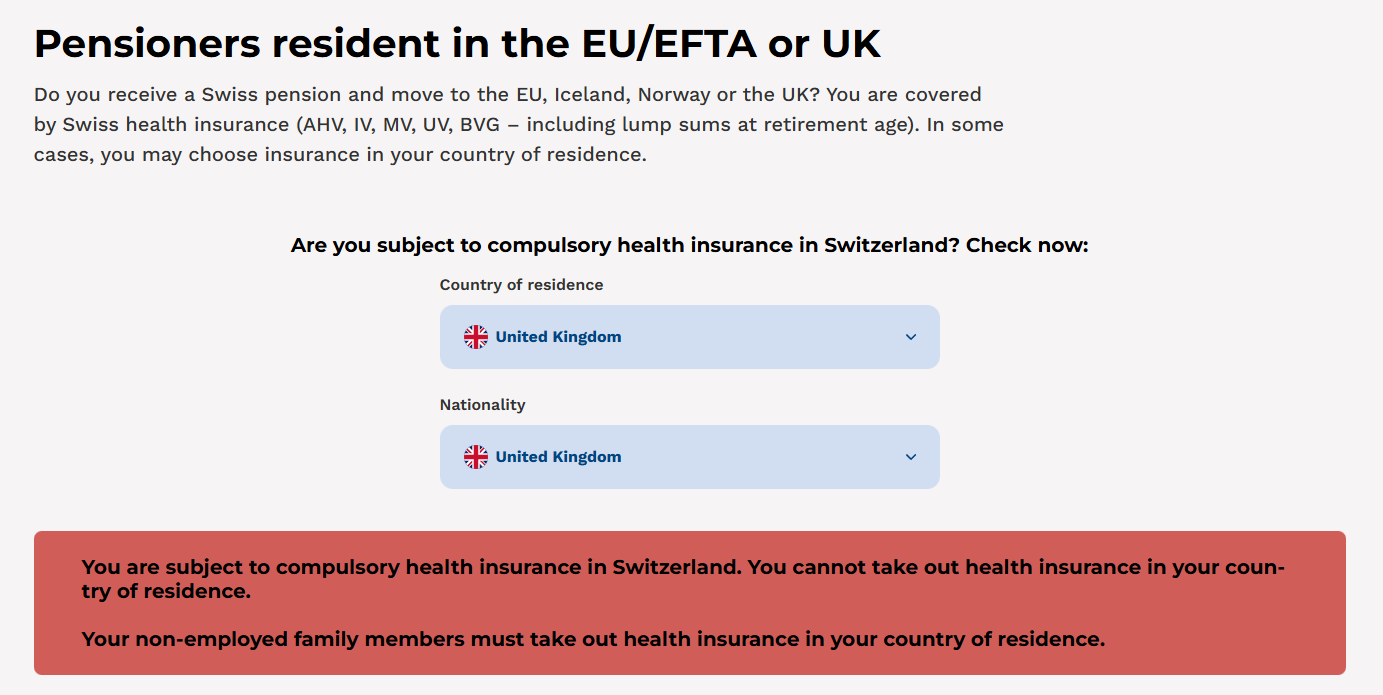

Okay, looking at this since hopefully we’ll get this darned move done early next year this just doesn’t make sense since we’re both pensioners so how can one have to pay while the other “non employed” doesn’t? Neither of us will be working. ![]()

Tbh I’m tempted to just ignore Swiss health insurance side except I don’t know what would happen when I stop paying the premiums. UK we’re already set up with a GP and they’re quite happy to treat us for free; didn’t even need to provide the paperwork suggested here.

Can’t remember if we did that form or not when we registered, but they’re happy with what they have on us including our NHS numbers.

And this contradicts that we need to continue to pay Swiss health insurance premiums.

" Returning to the UK to settle

UK citizens who return to the UK on a settled basis will be considered as ordinarily resident and will be eligible for free NHS care immediately."

Were you ever employed in Switzerland?

I’m guessing you’re the non employed one and your husband is the one on the hook for Swiss insurance since he has been employed here.

What the UK accept and what the Swiss consider acceptable are not necessarily the same thing.

Yes, I never worked here.

The KVG website is very misleading. It’s the default, for which one has to apply for exemption which in fact sometimes is mandatory ![]() a nice AI summary below. For UK resident it seems to be the “option right”, though I wonder if KVG has any room to refuse such exemption if requested timely

a nice AI summary below. For UK resident it seems to be the “option right”, though I wonder if KVG has any room to refuse such exemption if requested timely

- Default rule – When a Swiss pensioner moves to an EU/EFTA country (or the UK), the KVG treats them as still subject to compulsory Swiss basic health insurance. The Common Institution under the KVG in Olten verifies the affiliation.

- Option right (the “exemption”) – Within three months of the first pension payment or of establishing residence in the EU/EFTA country, the pensioner may submit a formal request to be exempted from Swiss compulsory insurance and to be covered by the host‑country system. The request must be accompanied by a confirmation from the local insurer that it will accept the pensioner. If approved, Swiss compulsory insurance ends.

- When the exemption is mandatory – If the pensioner receives a pension from the country of residence, EU coordination rules require that the health‑care be provided by that country’s system (the “benefits in kind” rule). In that situation the exemption from the KVG is not optional – the pensioner must be insured locally.

Well, we both receive UK and Swiss pensions so … Iirc I got my UK one before the Swiss because of the age difference while hubby’s only just started getting his UK one while having the Swiss for a couple of years now.