This is a very interesting thread.

I wonder now, the health insurance fees differ from canton to canton. Will there be a “foreigner-tarif” for people living abroad? And that should be lower as health costs anywhere else is lower too.

An interesting question. How do you even get a quote? Most seem to do online now and you have to enter a Swiss postcode to get a quote.

2 Likes

At this link you can see the premiums from all the main KK for CH health insurance for people retired in various countries. This is a good reference document to keep.

https://www.priminfo.admin.ch/downloads/gesamtbericht_eu.pdf

3 Likes

Thanks for sharing. Some staggering differences there. For the UK, cheapest was 285 and most expensive 715! ![]()

The webpage for pensioners overseas is also useful:

1 Like

Hm, for the UK I wonder if you take out private health insurance if that counts and you don’t then pay Swiss one. Then just cancel the private UK one and stick with NHS after.

When you leave CH, your Swiss health insurance covers you for 3 months as a tourist, so you need to show that you are covered for medical treatment by either social security or insurance in the new country.

As far as cashing in, it depends on if you are required to have ‘compulsory insurance’ If you are working you probably do unless if you are self employed or choosing not to work. I cashed out a Swiss Pillar 2 aged 52 moving to an EU country as I chose not to work & therefore not subject to insurance.

If you receive a Swiss pension you are required to take out Swiss medical insurance unless you have a UK pension when living in the UK. Taking out a UK private insurance would not solve the problem & with a Swiss pension you would not be entitled to the NHS.

Since the Swiss pillar 1 can be taken form age 63, yet the UK one will be close to 67. The other solution is delaying taking the Swiss pension until after the UK one, which is what I intend to do.

1 Like

Do have both. I think I paid slightly more into the UK one, but not sure how I could check that. Hubby paid for the Swiss one since I never worked here. Got the Swiss one a year earlier than the UK because of the age differences.

If you have a Government gateway account you can see the no of years you have a full National Insurance record, 35 years gives a full UK one & 44 years for a full Swiss one.

1 Like

Sadly not any more since HMRC told us we didn’t need to fill in UK tax returns.

I know I don’t get a full pension for either; Swiss is 25 years, but I think the UK one might be a bit more than that.

You don’t need to do tax returns to get a gateway account, I got one roughly 25 years after leaving the UK & never did a tax return in that time. There was also the option to pay back years at class 2 rate, roughly £160 a year if you were employed in the UK & then in Switzerland after you moved. You have to specifically ask for class 2, which was an option from about 15 years ago, previously only class 3 possible which cost far more.

Full UK pension requires 35 years, with any time spent in education after your 16th birthday credited, it’s worth checking your record as 3 years from my earnings were lost & eventually found after I made a fuss.

1 Like

The theory about what you should & shouldn’t do is all good but how does it actually work in practice?

By the time I claim my Swiss pillar 1 & 2 I will have been away from Switzerland for 5-7 years (depending on when I claim it). During that time I will have been registered for the NHS equivalent in my new EU residence for several years as well as having private health insurance.

Do the Swiss authorities send you a demand to take out health insurance at the time you receive your first Swiss pension payment & what happens if you don’t file for an exemption? Can they stop your pension, sue you etc?

The reason I ask is that whilst on paper the guidance is clear cut I have had an awful experience with the KVG, going back and forth and exchanging at least 10 letters but am no closer to resolving the problem & at this stage I’m just asking a simple question. I can just envisage all sorts of bureaucratic nonsense when the time comes to file for an exemption.

What would happen if you didn’t get an exemption and just stopped paying the Swiss health insurance? Don’t plan to keep our Swiss accounts open once we’ve finished everything so would they raid your pension to get the money? Even though you’re perfectly covered by the NHS?

1 Like

Exactly my thoughts. I have stopped paying the Swiss insurance (after a fight with my insurer), but both they & the KVG tell me that as soon as I receive my pillar 1 & the mandatory part of my pillar 2 then I have to apply for exemption & if I dont then I will have to take out Swiss insurance even though it will be several years since I will have lived in Switzerland and I’ll be happily insured elsewhere. If I don’t apply could they stop the pension?

Do the Swiss authorities send you a demand to take out health insurance at the time you receive your first Swiss pension payment & what happens if you don’t file for an exemption?

As mentioned above, you need to provide evidence of Swiss health insurance, or they will sign you up for one.

Can they stop your pension

Not sure if they have that power.

sue you etc?

But the health insurance can sue you for it and you will pay, or it will go to the court and then you will pay and pay fees on top.

I can just envisage all sorts of bureaucratic nonsense when the time comes to file for an exemption.

I think they exemption will go smoother as you are within the normal bureaucratic process. When you do something outside it e.g. asking them hypothetical questions, then you get stuck

- As far as the Swiss are concerned, once you apply and get Pillar1-Pillar2, this ‘triggers’ the requirement to insure in CH. It’s up to you (not them) to prove otherwise.

- This based on the treaty conventions, saying this is what should happen.

- You argue that since the EU country has accepted you on their health system (BTW, as a working-age person or pensioner ? not specified), the Swiss should let you go. However, it could be that the EU country is the one that has to stop insuring you and the Swiss takes over, based on the rules. (This argument reminds me of the 'this country has already taxed this income, you cannot tax it again" logic). Once the EU country becomes aware of your Swiss pension, they stop insuring you.

- Note that there are special rules for France, Germany, Austria, Denmark, Spain, Finland, Italy, Portugal, Sweden, Liechtenstein.

- Finally, in all cases you may get away from the Swiss compulsory insurance with the rare “catch-all principle” if you prove that you have some extra private insurance in that country that outperforms what is offered by that country.

2 Likes

You won’t be covered by the UK’s NHS as you are in receipt of a Swiss pension, so Switzerland is responsible for your healthcare costs, hence the requirement for Swiss insurance.

The health insurance can make a claim against you & the Swiss court will grant a deduction against your pension.

I guess another option is to get a pension in the country you are living in. Though given your age, I guess there’s no time for that now. But it might be worth checking just in case there is some special way to get it.

Some additional information on S1 from the UK NHS here:

-

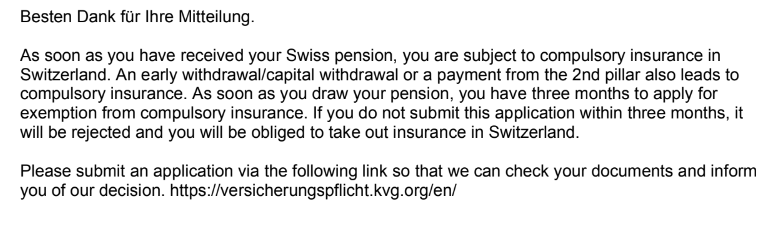

Are you sure this is right? When I contacted the KVG, they replied stating that any capital withdrawal from the pillar 2 triggers the requirement to request exemption, & the 3 month clock starts ticking from the date of withdrawal:

-

What is the rule about not keeping compulsory health insurance when relocating? I informed both my Swiss health insurer and the KVG that I wouldn’t be working when I moved to an EU country but they either ignored that or it didn’t make any difference to them.

-

Did you submit an exemption request at the time?