i know there have been a few other threads (which I have a searching through).

I simply wanted to ask (to help me optimize time and searching) for recommendations of financial institutions where I could open pillars 2a and 3a type of account. I’m aware that 2nd pillar needs to go with my employer, but I also think it is possible to open similar accounts individually (e.g. for a self-employed person), etc.

Requirements:

high rate of return

low overhead / cost

possibility to choose ‘funds’ to invest into?

no or minimum limitations / restricitons / holding period to taking out the money in 5-8 years

what other financially advantageous considerations should I take into account?

You have limited control of the 2nd pillar while you’re employed. For 3rd pillar I’d recommend Finpension and there are loads of strategies with different ROI.

Not exactly sure what you mean by that.

When you quit your job, you can transfer the money of the pension fund to a vested benefits account. Depending on your level of self employment, no need to join a pension fund, so the money can stay in vested benefits.

If you are self employed you can pay a higher amount into 3a.

Other than that, I second @SoSwiss . Finpension is definitely the way to go.

what I really was asking is even if I am employed, can I still (legally) open a 2nd pillar freizuzigkeitskonto (sp?), contribute into it and claim the tax deferral or am I ‘forced’ to use the employer’s 2nd pillar account (if I dont like the terms and conditions, for example) for additional contribution into the 2nd pillar ?

To clairfy, as an example, I’m changing employers and I dont like the terms and conditions of the new employer’s 2nd pillar funds. Can I take my existing 2nd pillar and perhaps have a second 2nd pillar account, say with with Finpension, and contribute additional directly to this account and still have the contributions as tax deferred (i.e. not contribute the additional into the employer’s 2nd pillar scheme)?

No. You’re supposed to transfer all the 2nd pillar from prior employer’s fund to the new employer’s fund.

Some people avoid this when they quit their job by transferring to a VB account and then not transferring this to the new employer’s account, though technically this is not allowed.

When you quit, you can split your account into 2 separate VB accounts. Some naughty people have done this and transferred just one of them to new employer and ‘forgotten’ about the other one which they continue to invest in more flexible institutions like finpension and VIAC.

In a word NO. We had grey ways to hide part of a 2nd Pillar (by accident) but then it reminds hidden for everything. You can’t contribute or claim tax relief. And without collaboration from the financial institution making it reappear is extremely challenging.

The nauthy Finpension, a well respected and often recommended company for 3rd pillar, investements and vested benefits, has an article about this topic. See especially ‘Was passiert, wenn ich der neuen Pensionskasse Freizügigkeitsguthaben verschweige?’

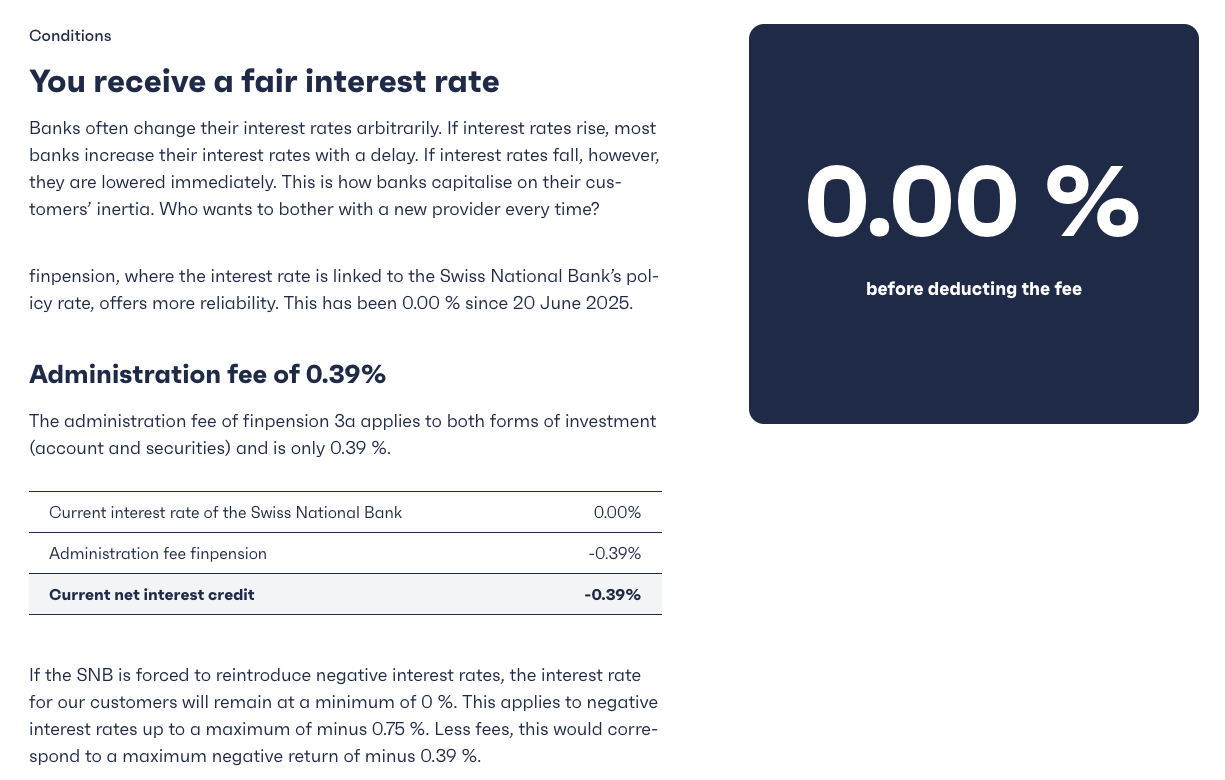

I am trying to understand the benefits.. On their site, “advantages of 3a account with Finpension”, they say “you receive a fair interest rate linked to the SNB, current intrest rate = 0% - 0.39% admin fee = net inerest -0.39%”, i.e would receive negative interest…

For comparison, eg PostFinance offers 0.05% with no amin fee, not much but at least positive..

You’re spot on. My comment was referring to your question about the location of the foundation being in SZ.

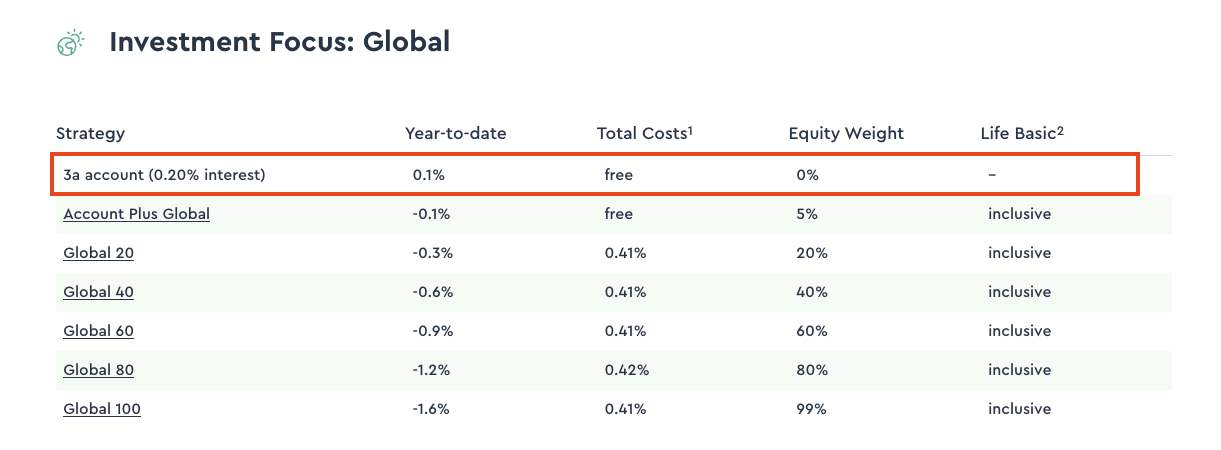

Holding cash is one of the few reasons not to use Finpension. Other 3rd pillar and vested benefit providers such as frankly, Viac and PF offer more attractive conditions for cash.