Not sure if many of you invest in stocks. I do, since like 45 years. Took out my pension in 2014 (2nd and 3rd pillar) and did invest it in the stock market. Working is nice, I even liked it, but it takes too much time. I started to make real money when I stopped working.

The most important thing to know in the stock market: you don’t know nothing! Nobody knows the future and anything may happen. Our brain is not made for stock trading because a lot of automatism that helped us survive do very bad in trading stocks. I call it our cavemen brain.

I think most of private stock traders lose money. That is why ETF are that popular. I’m not very keen of ETF for various reason, I may go into detail if you like.

There are over 100 bias that make us do the wrong thing in the stock market. That is why I concentrate on mechanical systems. If interested I can go into more details here too.

Since 2014 I do a high cash flow low risk dividend strategy (I call this the MOFO-home strategy). The CAGR since 2014, calculated with the XIRR function, is 11.61%. Changed the rules a bit in 2020 and since then the CAGR is 14.9%. In 2020 I found that I make too much money to spend it so I could gamble it away in a high-risk momentum strategy. That one made me a incredible 29.76% CAGR and did overpass my MOFO home strategy in value last year.

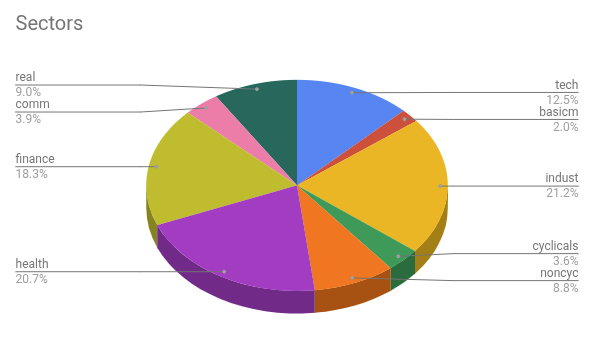

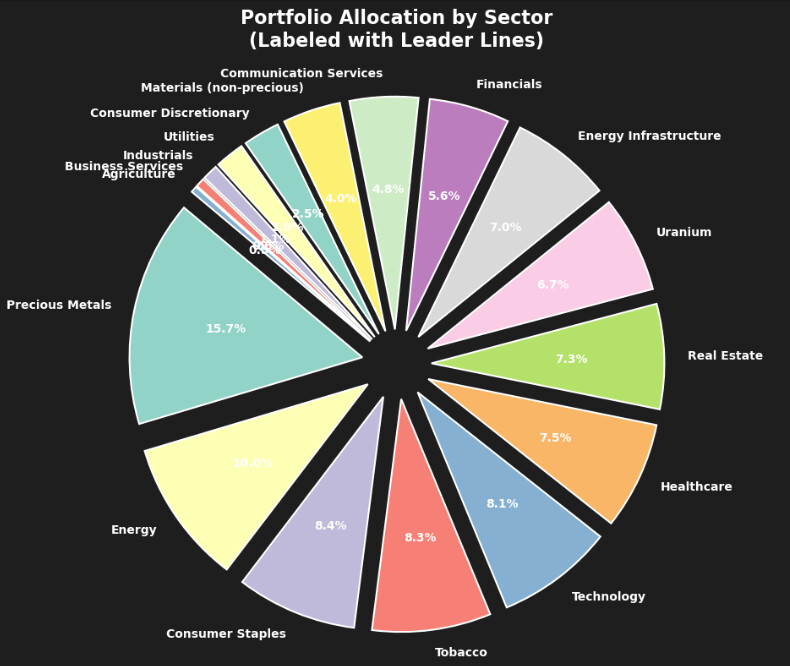

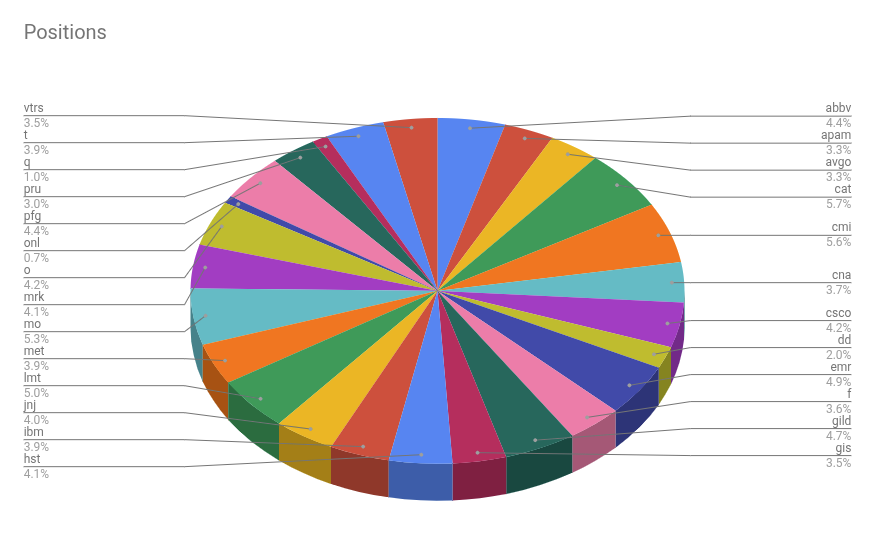

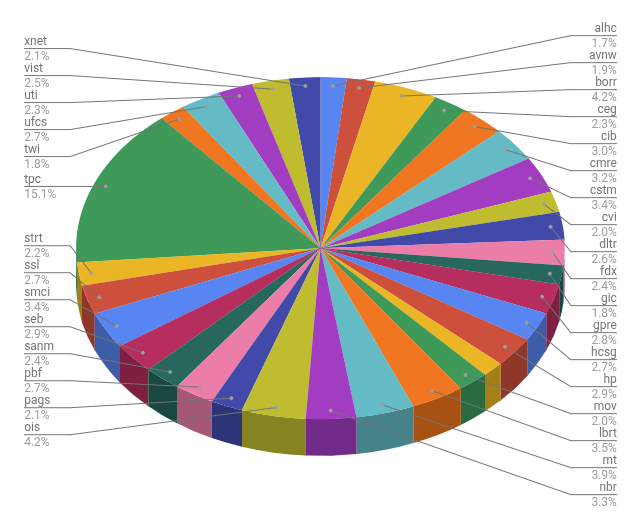

Here the contents of my MOFO-home and my gambling strategy in form of a “wheel of fortune”:

BTW: Much volatility today, but seems I am positioned quite nicely. In the MOFO home strategy I use sector and company diversification, in the gambling strategy I do not and hold a lot of oil stocks.

Don’t do that at home, the risk is gigantic! Stock market gains are paid with the currency called volatility. While the MOFO home strategy tries to reduce risk in any way the gambling strategy aims to take as much risk as possible, but only if the risk brings performance. The main task for an investor is to find out how much risk he can stand and then which risks bring the highest probable gain.

And don’t get blinded by the performance numbers. That were historically very good stock markets. There were only 3 minor bear markets and they did not last for long. My performance therefor may be pure luck!