Next up (in the series of going through my stock picks):

AMGN

Amgen, Inc. is a biotechnology company, which engages in the discovery, development, manufacture, and marketing of human therapeutics. For company profile details see footnote.[1]

FASTgraphs score:

Historical earnings graph, price chart, etc:

Steadily growing earnings at a nice clip of ~10%, stellar dividend CAGR of ~20% since they initiated one, 14 years of consecutive and rising dividends.

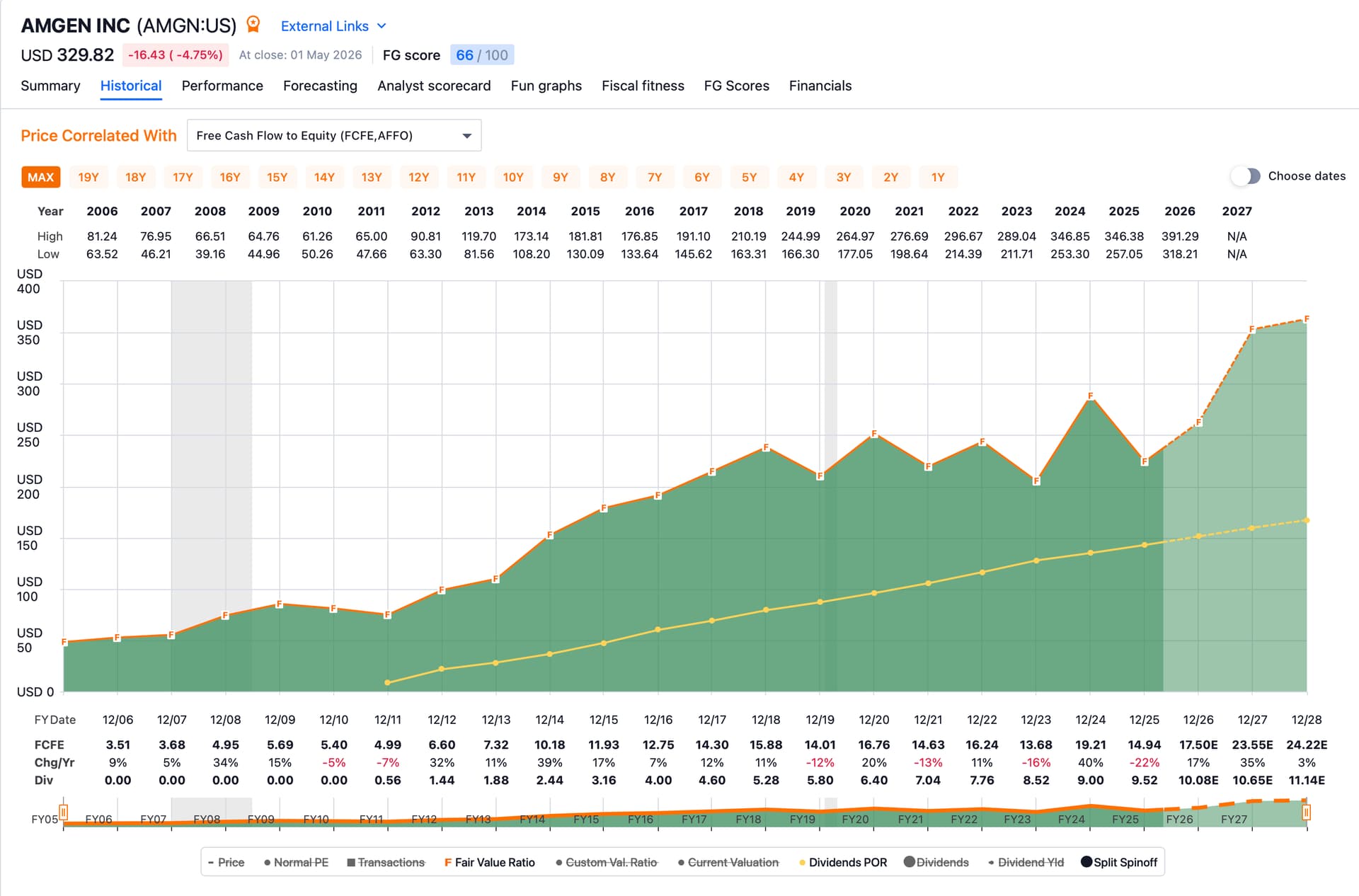

Free Cash Flow is similarly strong:

High on long term debt, but great BBB+ credit rating. Their strong cash flow easily allows them to service their debt.

Forward looking earnings:

They’re just about fairly valued right now. As the chart indicates, they can be purchased below fair value regularly (and can be sold above fair value regularly as well). Price always stays pretty close to its normal valuation of around 14 x P/E.

Also visible on the chart above: AMGN never misses analyst estimates for earnings.

AMGN is one of my favorite positions. It’s already an almost full position, alas. If I loosened my risk management[$] this is a position that I’d grow a lot.

Currently a hold, but easily a buy if its PE dips below 14.

$ Company profile:

Company description:

Amgen, Inc. is a biotechnology company, which engages in the discovery, development, manufacture, and marketing of human therapeutics. The company was founded by William K. Bowes, Jr., Franklin Pitcher Johnson, Jr., George B. Rathmann, and Joseph Rubinfeld on April 8, 1980 and is headquartered in Thousand Oaks, CA.

GICS Information:

Health Care >Pharmaceuticals Biotechnology & Life Sciences >Biotechnology >Biotechnology

Company website:

http://www.amgen.com

$ Maximum position size is limited to contributing max 2% of all dividend income.