People talk about the relentless bid from passive investing driving this continued momentum.

1 Like

Market capital based weighting of stock in ETF is momentum investing, that is true. But not the best one if you compare with my momentum strategy, the one I post the results every month here.

I did beat “the market” in form of the most used indices in 6 of 7 years that I follow that strategy. Currently the CAGR since 01jan2020 is at 30.03% per year, capital weighted method (XIRR).

Momentum works, but probably not in the way the indices do it.

NOW jumps on news Trump acquired stake in the company. Are investors going to track Trump trades as they do for famous investors?

Some more trades in the past couple of days:

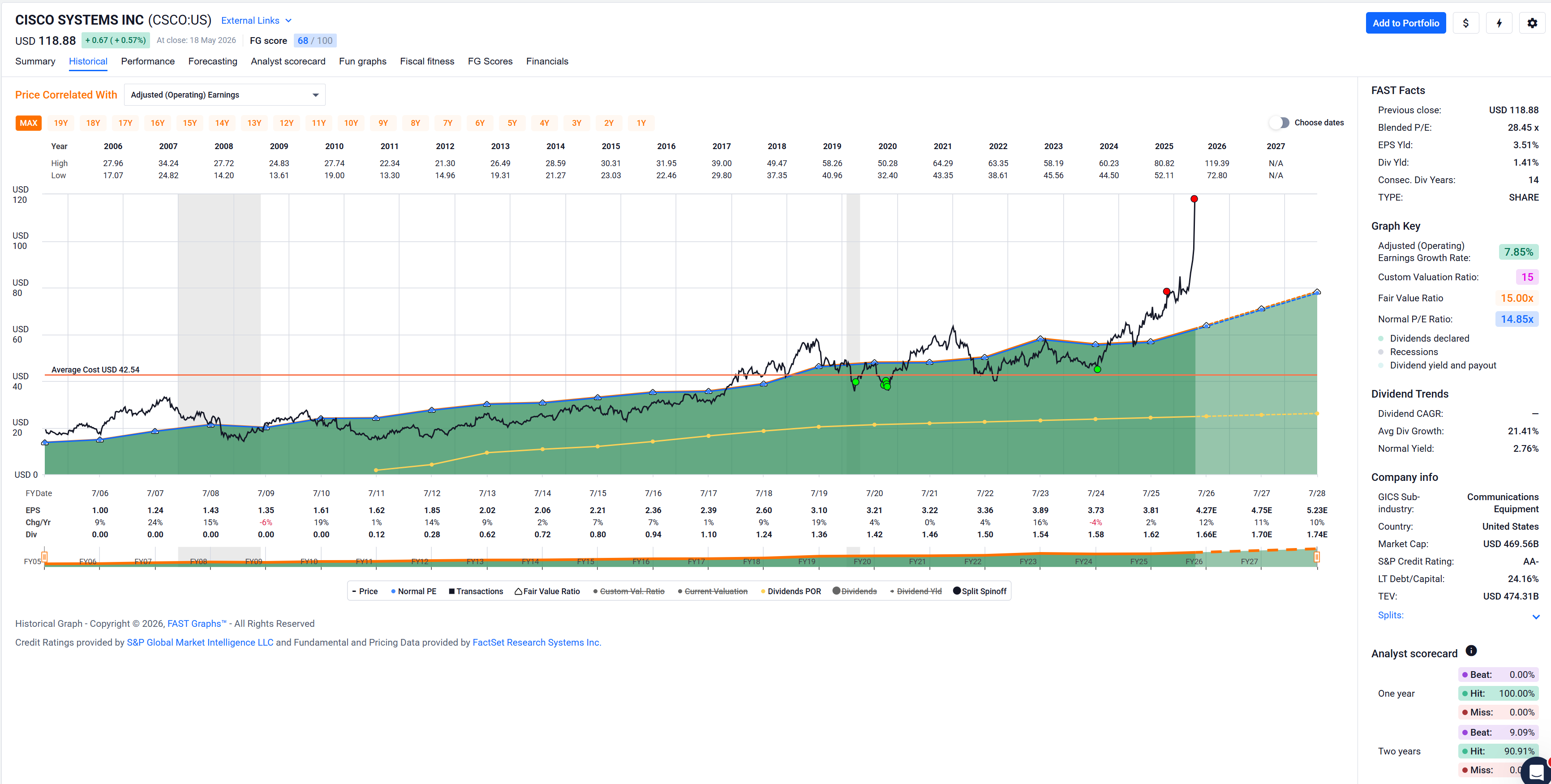

- got rid of another slice of CSCO

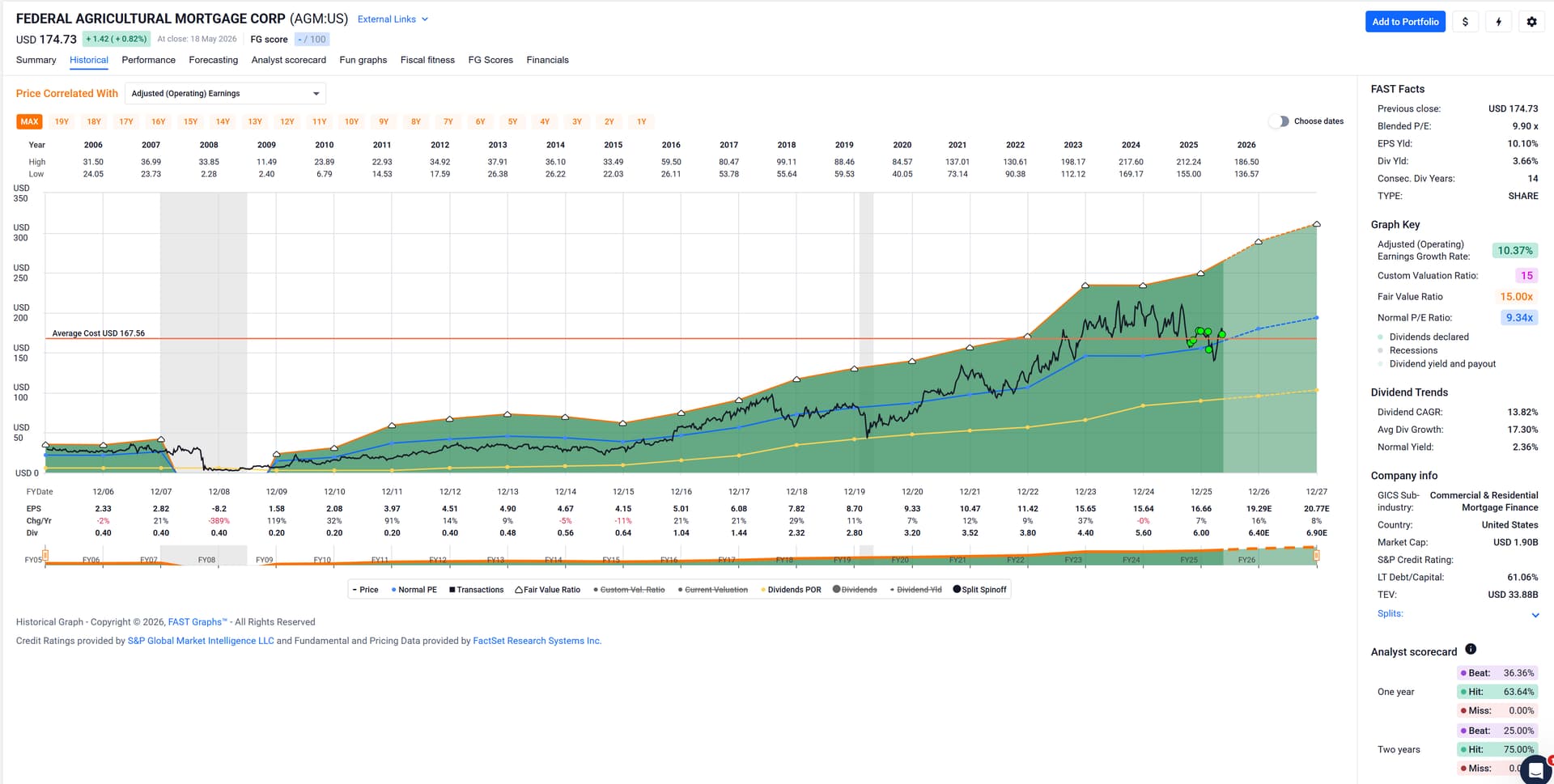

- added some additional AGM

- added some additional AMGN, violating[

] my own position sizing

] my own position sizing - added some additional PAX

- added some additional GPC

FASTgraphs below for those interested.[F]

Motivation as almost always was generating more income (i.e. not total return) while reducing some risk.

![]() My fast and not so hard rule says that income generated by a position should not exceed 2% of the total income generated by the (stock picked) portfolio.[E] Just so that I only suffer from a 2% income loss if the company somehow goes out of business tomorrow.

My fast and not so hard rule says that income generated by a position should not exceed 2% of the total income generated by the (stock picked) portfolio.[E] Just so that I only suffer from a 2% income loss if the company somehow goes out of business tomorrow.

Well, AMGN now generates a whopping 2.31% of my stock picked portfolio income.

Maybe someone from the Die Hard mechanical portfolio crowd shoud report me to the police … ![]()

E Except in … ahem … exceptional circumstances, e.g. when the income generated by the position organically grew above 2% of total income and seems sustainable and the company remains mostly fairly valued.

F The FASTgraphs:

2 Likes

Long dated treasury yields are rising. Is this a sign that a new tightening credit cycle is under way? Maybe a time to curtail long duration bets?

I’m just a macro tourist – I enjoy the sights, but can’t make much out of them (of what to do), so I wouldn’t know. But …

Or even intermediate term duration bets …?

Possibly not what you are alluding to with “long duration bets”, but I’m selling down some of my money like (fixed income) holdings (with an average duration of about 6 years) and am replacing them with equity … kind of as we speak.

It’s partly driven by interest rate expectations, but mostly driven by me finally realizing what I always kinda knew but wasn’t ready to admit: anything money like, even if it pays interest monthly, is doomed over time.[![]() ][𝓕]

][𝓕]

Given some more experience under my belt with my (stock) income strategy, I finally feel fine and safe enough to replace some of the (false) security of stable bond payments with the potentially larger volatility[σ] of dividend payments of dividend and dividend growth companies.

![]() I know exactly who is going to clap and tell me “told you so …”. Hi @cubanpete!

I know exactly who is going to clap and tell me “told you so …”. Hi @cubanpete!

𝓕 Chuck from FASTgraphs actually pushed me over the line with one of his recent presentations published last weekend.

σ Volatility is not a measure of risk. That’s just Modern Portfolio Theory ![]() .

.

1 Like

To be fair, bonds had a good run for a few decades from the inflationary times of the 70s until the first innings of covid. Once they reached zero or even negative, it was at the end.

They could still be useful to manage a bad downward shock in equity, but the cost of that over the last decades has been expensive and didn’t even work that well for the mild drops we had recently.

1 Like

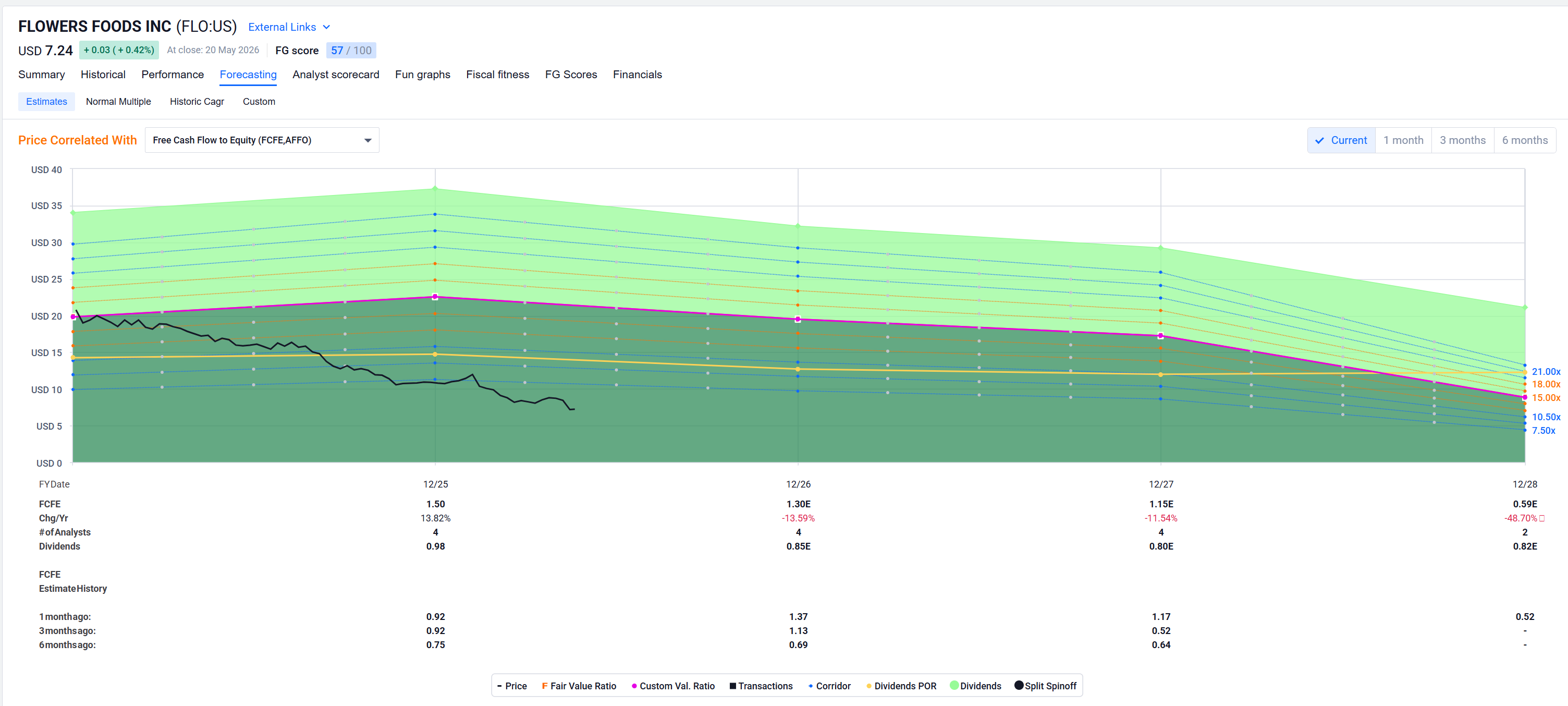

Just opened a position in Flowers Foods (FLO) - a falling knife… that I hope to catch just fine ![]()

Bad day to be an INTU shareholder: stock crashes 20% today.

Only four fingers and a thumb that you can lose (if using one hand only catching the knife) … ![]()

I like the rudimentary FASTgraph pic (looks undervalued, etc), but I hate buying into dividend cutters.

Free Cash Flow seems fine this year and next year but still a bit iffy afterwards.

I know @cubanpete just initiated a positiion a short while ago on FLO, and one of my mentors did as well, maybe about 9 months ago or so.

I personally can’t bring myself to buying into it:

- earnings trajectory too flat

- FCF … well, analyst expectations could be better

- I already own GIS, a similarly segmented

companyfalling knife

Good luck!

1 Like

I don’t know enough about their business.

Potentially another one of the “yeah, sure, I’m gonna replace it with the AI coding project my intern whipped up last month” stacked to compare to “well, we have decades of compliance we need to continue to stick to and Intuit basically guarantees that, let’s stick with it”.

The FASTgraph looks like it’s buyable, but what do I know.

I always feared for their business in case the government would create some kind of web portal that allows people to file their tax returns easily and cheaply and so not need private products. The UK has this where people can file online.

Though I guess with US capitalism, my fears are probably unfounded. And I’m sure Intuit are good at bribing lobbying the right people.

Also I don’t believe any company will use a vibe-coded product. But Joe Sixpack individual, I can see them using some vibe-coded open source tax filing product to save $50.

Also:

Intuit beats Q3 estimates, raises FY26 guidance and cuts 17% of workforce as Jefferies cuts PT to $550, keeps Buy

- Q3 revenue $8.6B, +10% YoY; non-GAAP EPS $12.80, +10% YoY, above guidance.

- Raised FY26 revenue growth outlook to 13–14% and non-GAAP EPS growth to ~18%

They beat, raise and even cut headcount and the market still punishes them. What do they need to do?!

1 Like

Waiting for the numbers, must come out any day now. I paid 7.99, actual price 7.05, there goes the dividend for almost a year. ![]()

Addition: just checked, numbers are due tonight after the closing bell. Almost everybody expects them to cut the dividend, what they never did.

And here they are (PDF):

Flowers foods (FLO): And the first peak at the cash flow looks nice. All my criteria are still fulfilled, it is therefore still on buy. I will probably buy more as soon as my current debt in the dividend strategy is paid back.

Not sure because the provided audio is too long (I hate that), but it does not look like they will cut the dividend.

Stock is rising after market.

2 Likes

Yep, looks like. They did buy back a lot of shares what seems to make more sense at this price. The dividend will go down to 7% (from around 14%). That will produce more selling pressure I suppose. It will get kicked out of the U.S. dividend 100 index.

1 Like

Would you still consider it a buy?

(FLO): Yes, it is on state buy. The debt is manageable and they would even have enough to support that old dividend.

However, as I start my selecting procedure with the U.S. Dividend 100 Index and FLO will be kicked out of it today I would not initiate a completely new position.

1 Like

I’d also say that technically it probably is a buy now.

Dividend payout ratio will fall below 50% of earnings and even if the company stays flat with earnings you’re still looking at a nice dividend.

I guess the dividend cut should also change the outlook for the FCF situation which is what made me avoid FLO in the first place.

I’d have to do some more research, though, to conclude whether I’d actually consider it a buy.

Gut still says no after the cut and I expect they’ll keep their dividend flat for a while given their language around “strategic transformation” on slide 4 in the presentation.

Great thing is that it’s a market of stocks, not a stock marketTM so I can look at other attractive brides out there when I have cash to deploy … ![]()