In other news NVDA raised their dividend by 2400% – from $0.01 to $0.25. ![]()

1 Like

There’s apparently also relentless bidding into active investing …

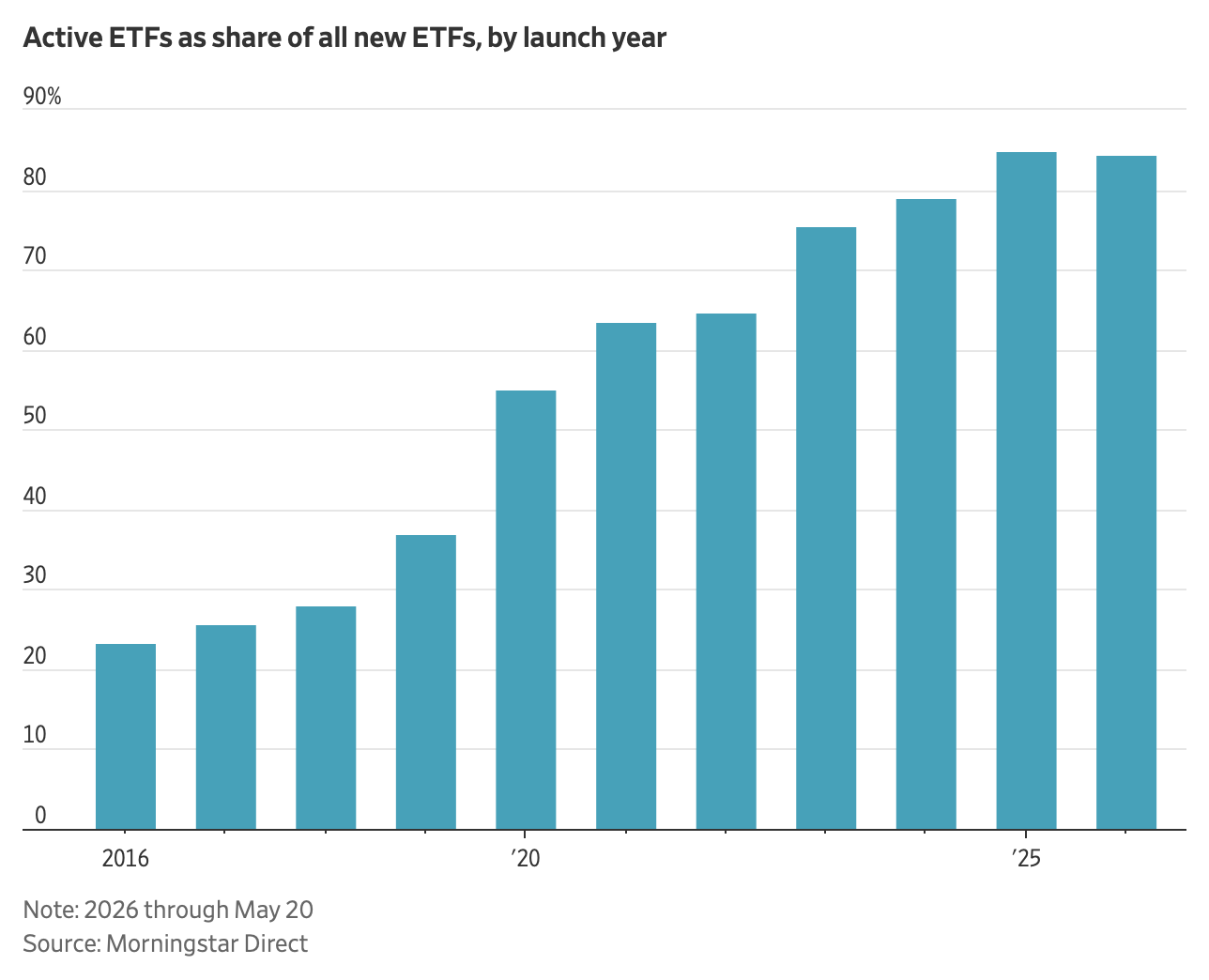

Jason Zweig writes in the WSJ:

How Weird Are ETFs Getting? Try UFO and Midnight-Bitcoin Funds[$]

Excerpts that made me chuckle:

To see just how far ETFs have drifted from the investment mainstream, look at the Tuttle Capital UFO Disclosure ETF. It was launched—and I do mean “launched”—in February.

The fund seeks to buy stocks that could benefit from “government disclosure, confirmation, or exploitation of advanced technologies” related to “non-human intelligence.”

Another unorthodox fund is the Nicholas Bitcoin and Treasuries AfterDark ETF, which began trading in April. With $30 million in assets, it charges 0.97% annually. For that, you get exposure to bitcoin’s returns—but only when the stock market is closed.

Each day from Monday through Friday, the fund starts out exposed to bitcoin, flips to Treasury bills or cash at 9:30 a.m. Eastern time, then darts back into bitcoin at 4 p.m. (It stays in bitcoin over the weekends and on holidays.)

The ETF’s strategy, says David Nicholas, one of the portfolio managers, is based on data indicating that bitcoin earns higher returns outside the U.S. stock market’s trading hours.

$ Gift unlocked for a limited time.

2 Likes

I guess I got lucky with timing (FLO).. Let’s see how it fares longer term

1 Like

At least it was 11h ago. Wow, one Cent over my entry price.

I don’t know if it takes artificial intelligence to tell us that dividends are bullshit. But I like to use them as a measurement of risk. Maybe I am completely wrong and should just take out a few bucks to be able to live and invest the rest in my gambling portfolio. That is, with >30% per year instead of 14%.

![]()

Yeah, half of that “buy” opportunity I alluded to earlier just evaporated in a couple of trading hours … IMO still not unbuyable, but surely a bit more sellable now … ![]()

BTW, not the first time I’ve observed a dividend cut sending the price up … market believing the company’s business model now being more sustainable, etc. Probably true in this case. I’m still not a buyer, I’m afraid, especially not after the price hike in the past few hours.

Anyway, still good luck to the current holders!

May I suggest launching your gambling portfolio as an ETF, naming it “>30% p.a” … ![]() … you know, in the spirit of the ETFs mentioned above by Jason Zweig in the WSJ.

… you know, in the spirit of the ETFs mentioned above by Jason Zweig in the WSJ.

Also don’t forget to charge 0.97% in fees, and live happily ever after. You’ll profit from the gains and from the fees!

More seriously:

Stay the course, Pete, …, especially if your gambling portfolio keeps delivering over time. Just shift allocations … perhaps gradually? … until you’re confident the gambling portfolio can sustain you.

Of course, you knew that already.

1 Like

My whole life I was looking for a way to make money without having to deal with idiot bosses, idiot clients and idiot employees. Finally I found it and I will not destroy it for a few (billion) bucks!

Somewhere I did read that once you have provided for basic needs for you and your family, money does not bring more happiness. It is just worries, how will I (… my wife) spend that?

When asked how that made him feel, Heller replied: “I’ve got something he can never have.” When Vonnegut asked what that could possibly be, Heller said, “The knowledge that I’ve got enough.”

2 Likes

No need to fear. The US tax return is one of the most complicated in the world. However one can argue if it is the most complicated. 15 Countries With The Most Complicated Taxes | Millionaire Migrant

So you will still put money into their buns?

In the end, the economy does depend upon consumption.

Never tried one.

My captain says yes, it is on buy and it is worth less than 4% of my portfolio, so if there is money laying around I’ll buy more FLO.

The U.S. Dividend 100 Index is just a help to limit new buys to a 100 candidates. Being kicked off it is not a problem for the captain. My only restriction dividend wise is that it is over 2%. After the cut it is still >6%.

Only that the fund has to sell the company at a loss. Only to buy it back at a higher price if it should ever reenter.

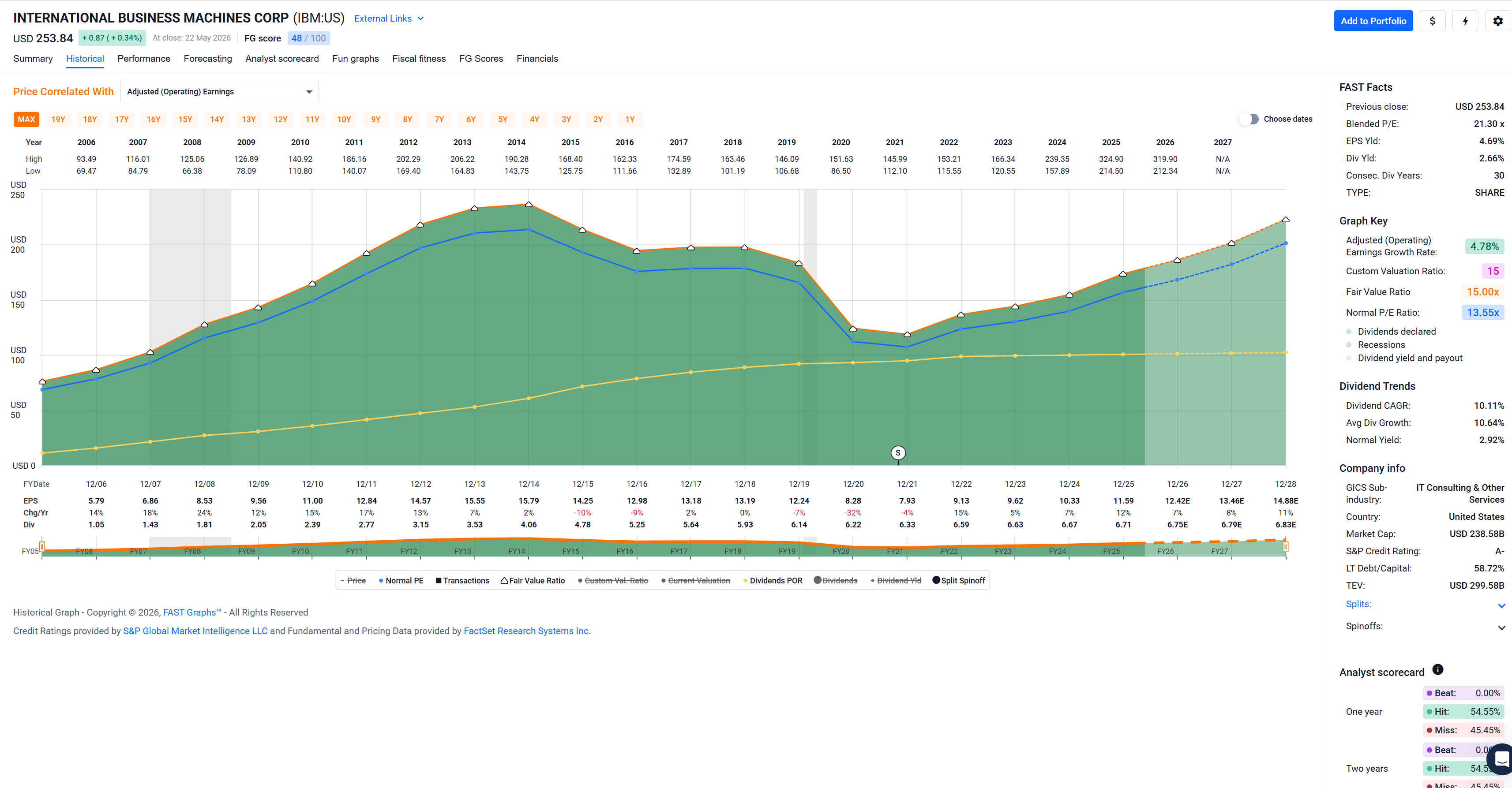

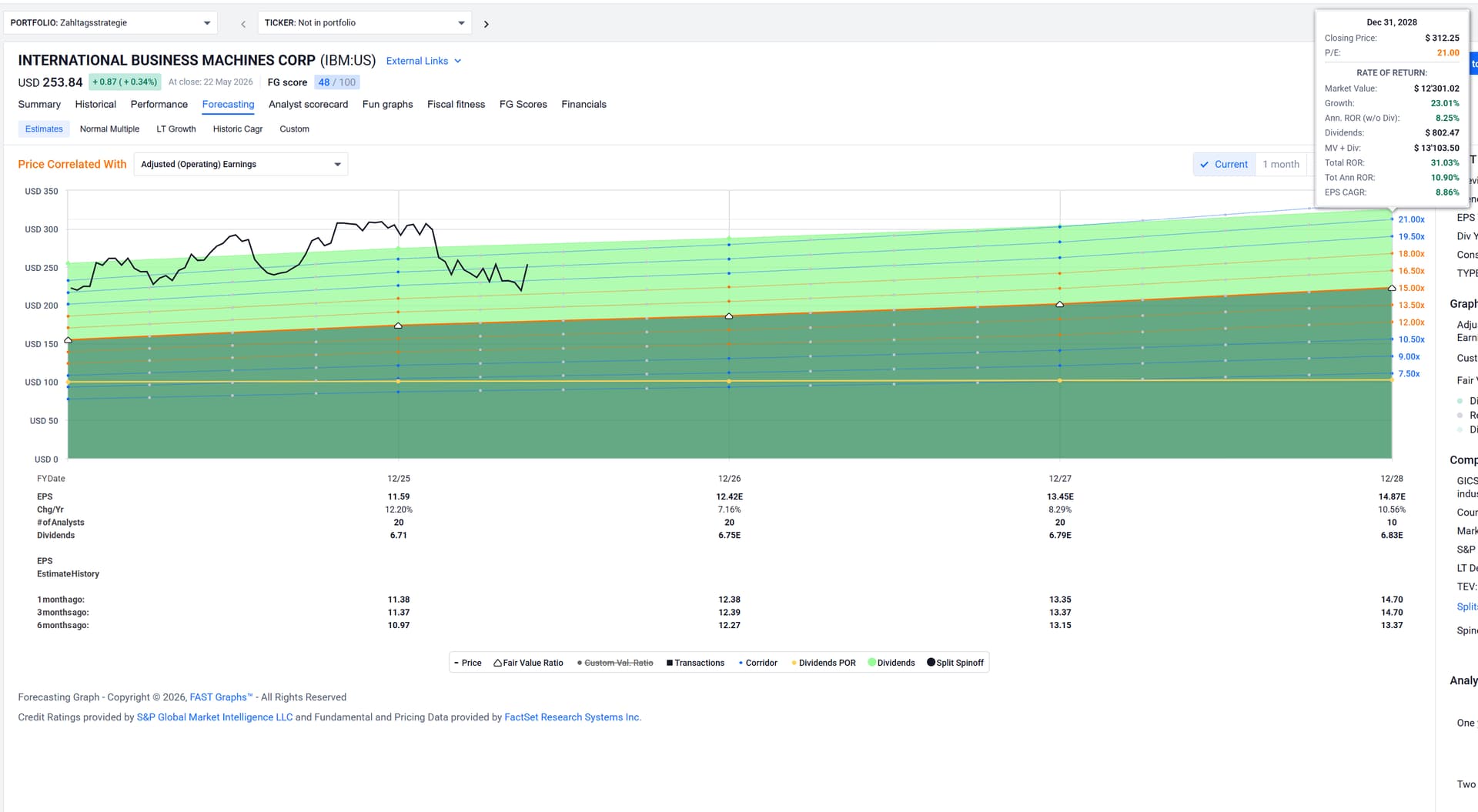

So! Would you consider also IBM?

I’ll bite …

IBM’s earnings history looks like continuous piles of turds to me, some bigger, some smaller.

Also, please use a good magnifying glass for spotting the company’s dividend increases in the past decade or so … it’s not even keeping up with inflation. ![]()

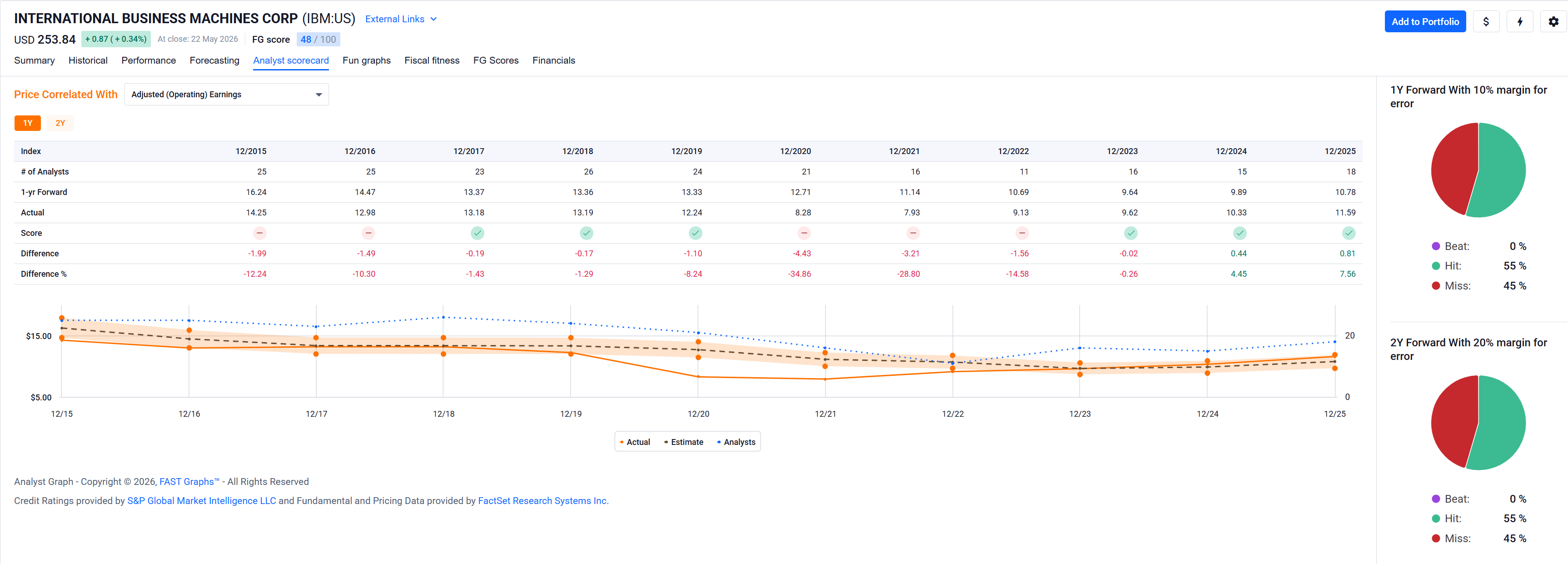

The company misses analysts’ earnings forecasts about half the time – probably over optimistic company guidance and analysts having a hard time estimating earnings.[![]() ]

]

(this should lead us to applying some caution when looking at future earnings estimates …)

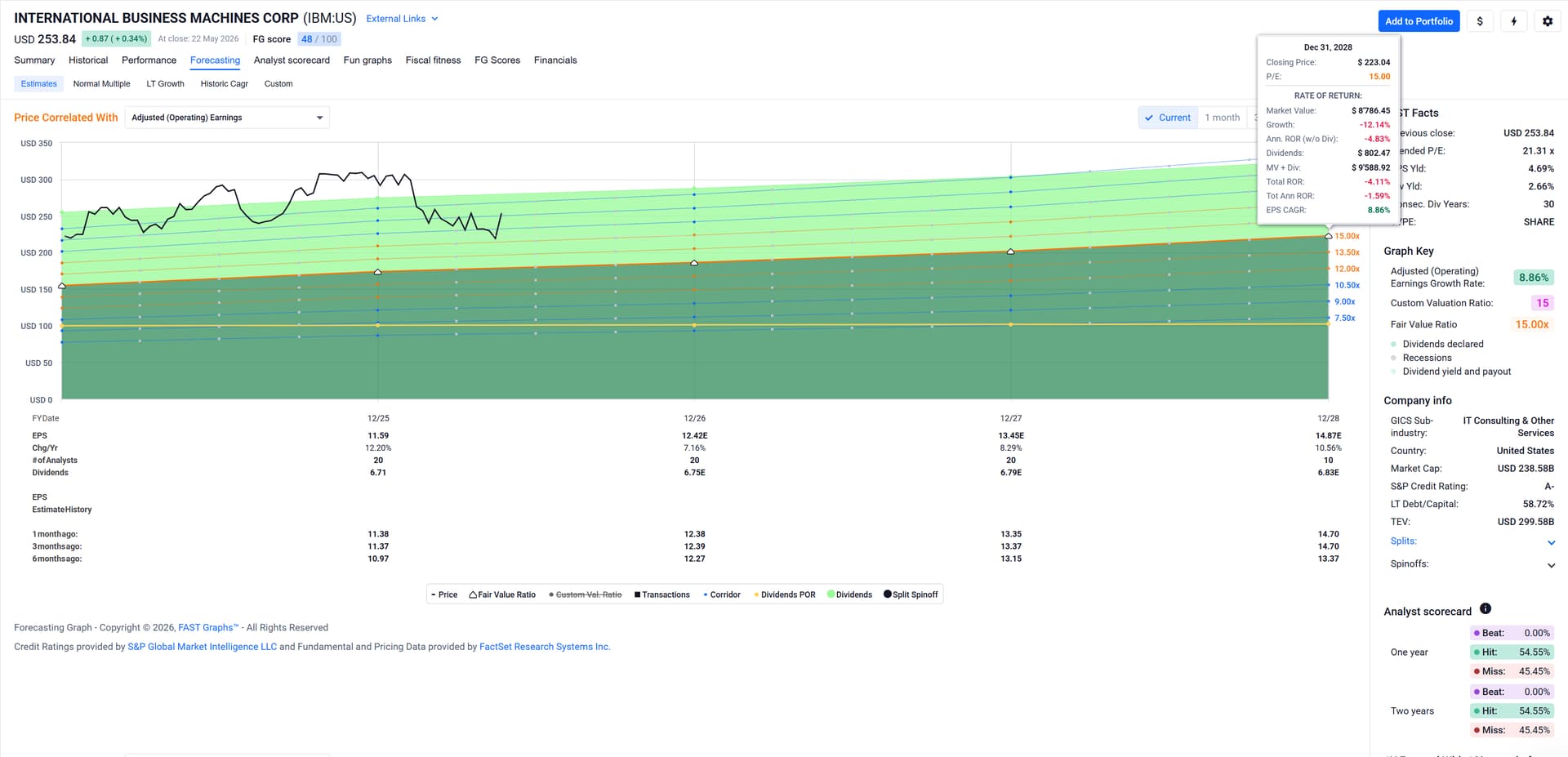

Since we’re not buying the company’s past, let’s look at the future. Given its (earnings) growth, the fair value is 15 x P/E. If the company returns to that (valuation), you’d be sitting on dead money for the next couple of years, even if you include dividends.

If the company stays at its current (over-) valuation, you’re looking at about 11% annual total rate of return. Not bad. Not great, either.

I would pass on this company.

YMMV, of course.

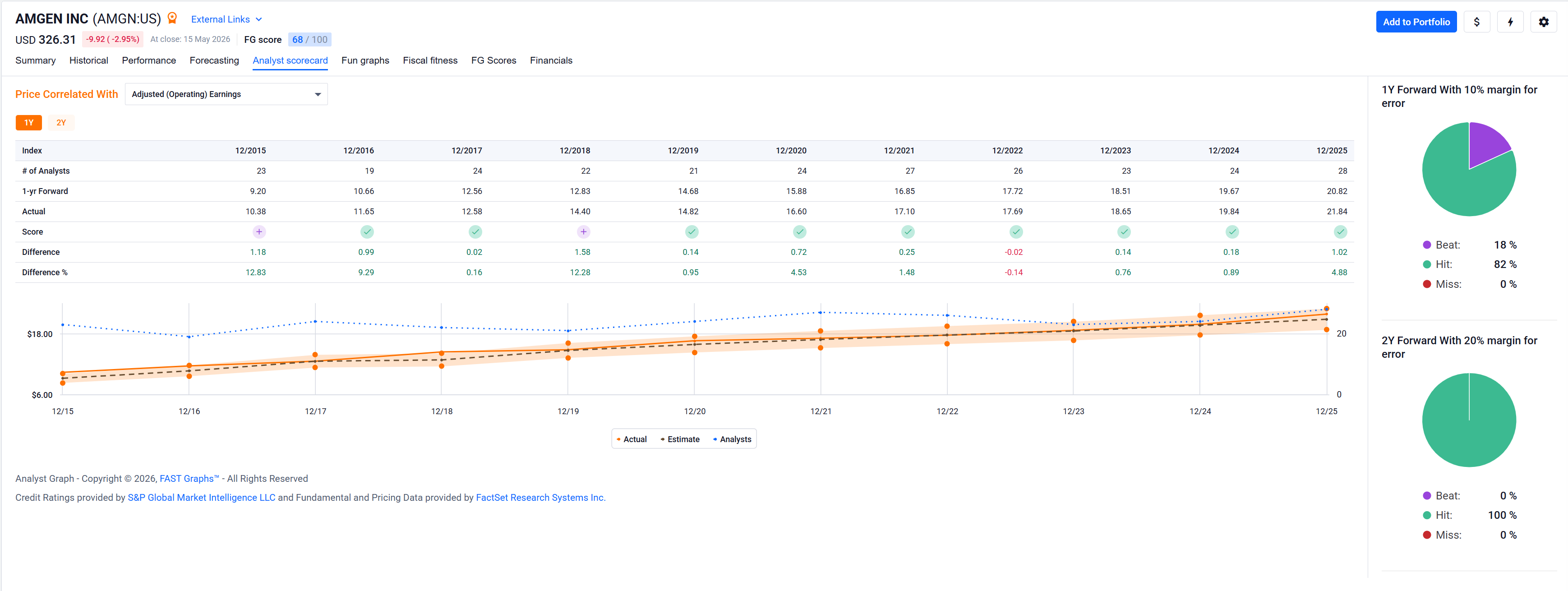

![]() Please note that analyst estimates for earnings are not the same as price targets by analysts. The latter are essentially crystal ball readings while the former are often close for “good” companies (e.g. AMGN, one of my currently favorite ones:

Please note that analyst estimates for earnings are not the same as price targets by analysts. The latter are essentially crystal ball readings while the former are often close for “good” companies (e.g. AMGN, one of my currently favorite ones:

1 Like

Actually not only consider, it is with me since a decade or so. Dividend yield is currently at 2.66% and the captain says it is still a buy. But I cannot buy because it is already more than 4% of my portfolio. You find all my rules in one of the first posts here.

Just checked, a decade of dividends, 73% capital gain and about a year ago there was a juicy “market dividend” which puts my entry price almost to zero.

2 Likes

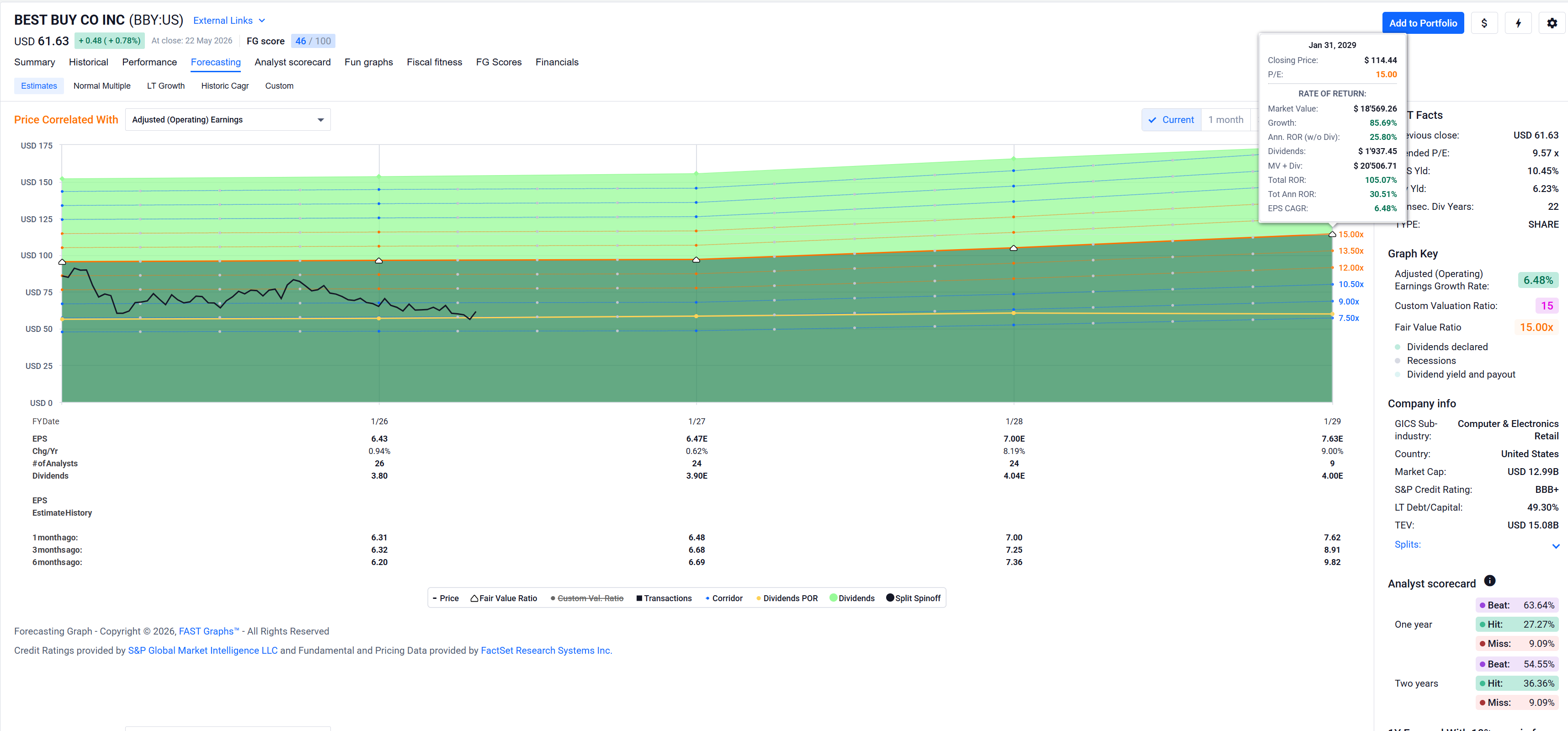

Next up (in the series of going through my stock picks):

BBY

Best Buy Co., Inc. engages in the provision of consumer technology products and services. For company profile details see footnote.[1]

FASTgraphs score:

Historical earnings graph, price chart, etc:

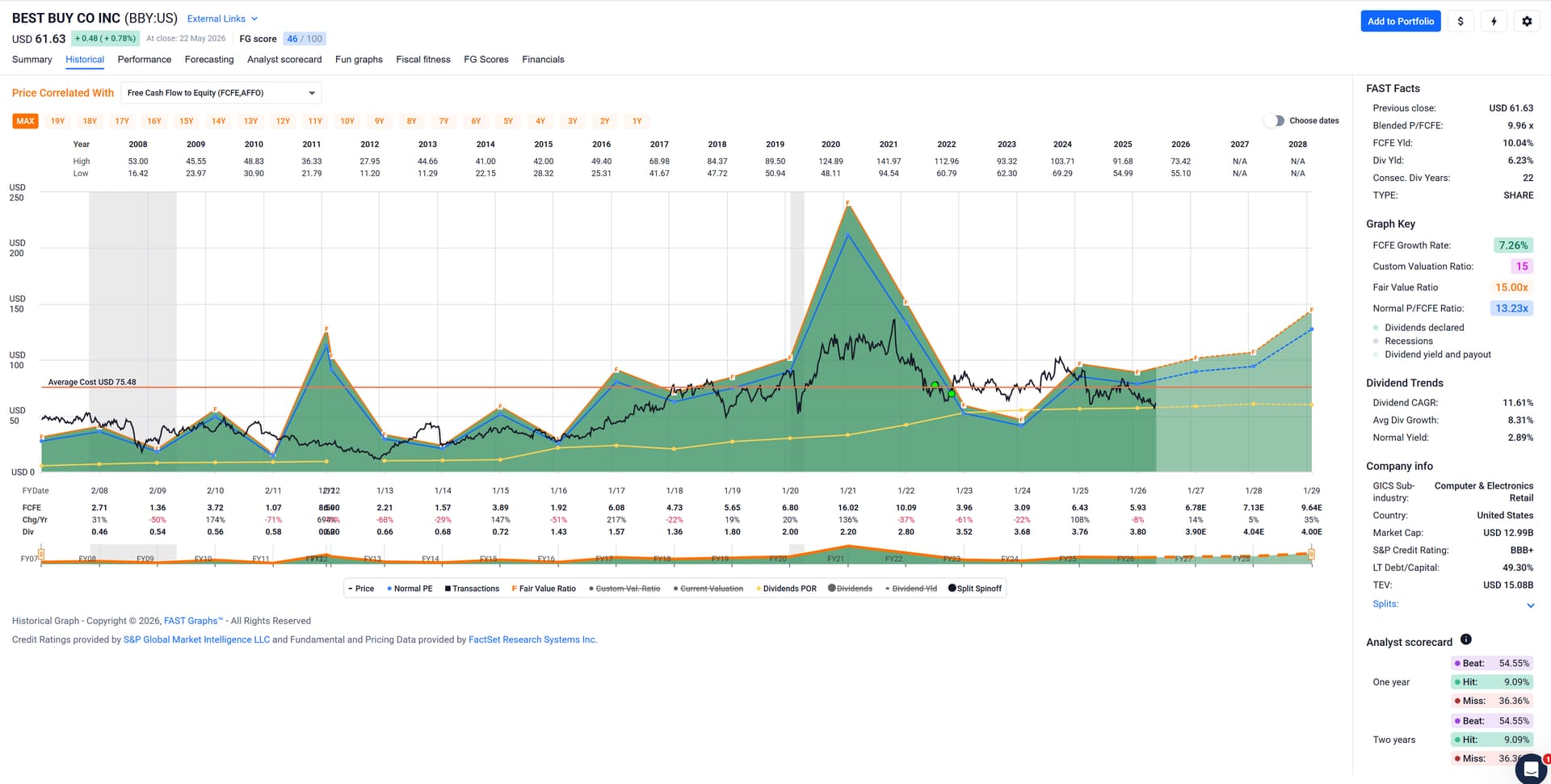

Since I poo-poo’d on IBM yesterday I first have to admit that

- BBY’s earnings history looks like continuous piles of turds to me, some bigger, some smaller.

- please use a good magnifying glass for spotting the company’s dividend increases in the past

decade3-4 years or so

Earnings growing at less than 5% p.a., at least the dividend CAGR was double digit over the past 20 years (but not since I own it).

Analysts are pretty good at earnings estimates according to the scorecard.

Free Cash Flow looks almost as unimpressive as earnings (but at least covers the dividend well in most years):

Forecasting earnings:

Analysts expect earnings to grow at about 6.5%, not bad, not great. If the company valuation went to a (fair) 15 x P/E, I’d see a nice a nice total annual rate of return (ROR) of 30% (from here). If the company stayed at its current multiple of ~9.5 x P/E, I’d still see a nice total annual ROR in in the double digits. If the price went to the company’s normal multiple of about 12, I’d see a total annual ROR of 20%.

They’re undervalued and they pay a nice dividend. When I bought them I fell into the trap of believing their earnings would continue to grow as during COVID-19, but the market saw through that which is why the price fell.

Average company, but reliable dividend payer.

BBY is a hold in my portfolio. I’d upgrade to a buy if growing earnings expectations actually became true in the next year or two.

1 Detailed company profile:

Company description:

Best Buy Co., Inc. engages in the provision of consumer technology products and services. It operates through two business segments: Domestic and International. The Domestic segment includes operations in all states and territories of the U.S., operating under various brand names, including Best Buy, Best Buy Mobile, Geek Squad, Magnolia Audio Video, and Pacific Sales. The International segment consists of operations in Canada. It also markets its products under the brand names: Best Buy, bestbuy.com, Best Buy Express, Lively, Geek Squad, Magnolia and Pacific Kitchen and Home. The company was founded by Richard M. Schulze in 1966 and is headquartered in Richfield, MN.

GICS Information:

Consumer Discretionary>Consumer Discretionary Distribution & Retail>Specialty Retail>Computer & Electronics Retail

Company website:

1 Like

Thanks for your quality posts!

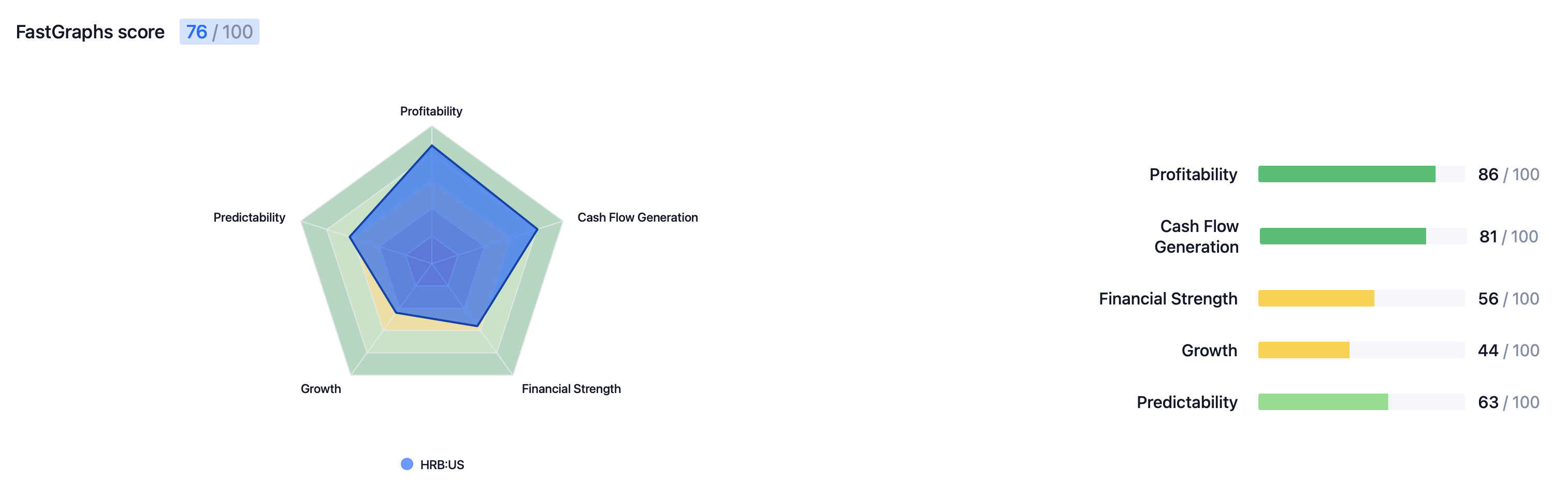

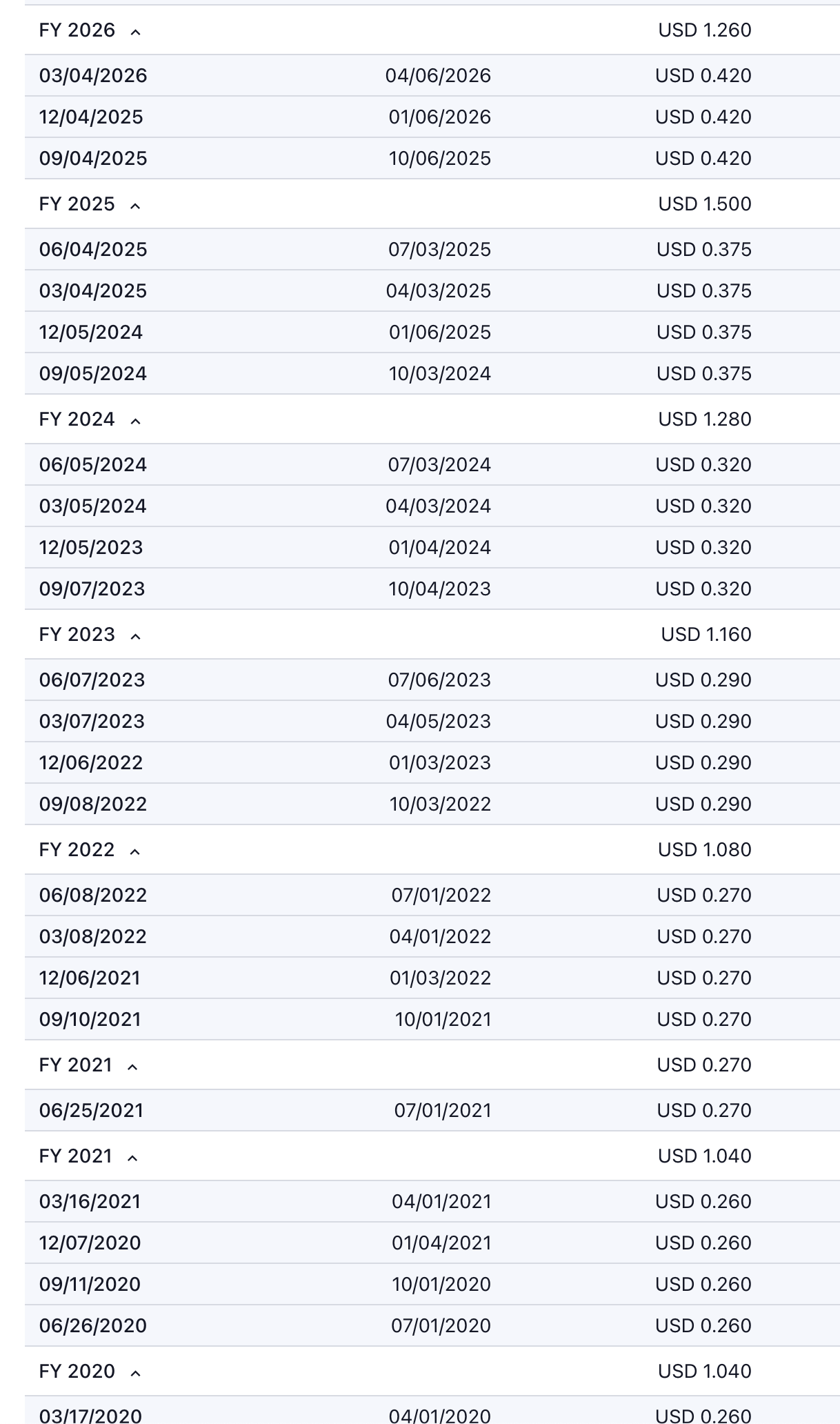

I am considering opening a position in HRB as I believe they are undervalued, dividend at around 4%. Debt is a bit high though, AI disruption might bite…

H&R Block[HRB] looks interesting from a fundamental and FASTgraphs perspective.

Earnings:

Looks like they changed their financial year ending in April to June about five years ago which probably explains why there’s a missing dividend on the graph.[$]

FCF:

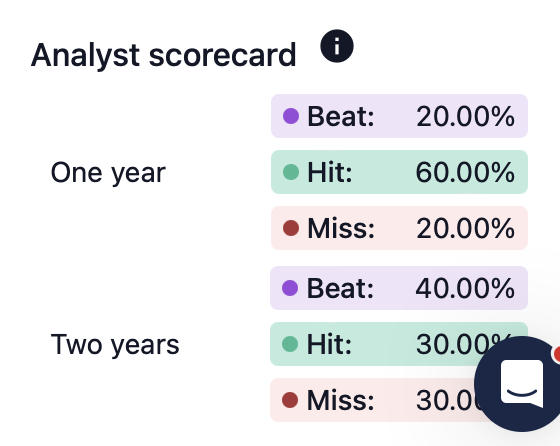

The analyst scorecard looks a bit iffy[$$] and they’re indeed high on debt so I’d probably dig into their long-term debt maturity schedule on their latest 10-K or so.

AI disruption would surprise me (along the lines of the discussion around Inuit we had earlier).

HRB Company profile:

Company description:

H&R Block, Inc. engages in the provision of tax return preparation solutions, financial products and small business solutions. The company was founded by Henry W. Bloch and Richard A. Bloch on January 25, 1955, and is headquartered in Kansas City, MO.

GICS Information:

Consumer Discretionary >Consumer Services >Diversified Consumer Services >Specialized Consumer Services

Company website:

$ In fact, looking at the Performance tab on FASTgraphs, they didn’t miss a beat:

$$ Analyst scorecard:

2 Likes

Truly beautiful story and eternal wisdom that I will use to remind myself when greed creeps up on me.

I asked Gemini to create a PDF on Vonnegut’s subsequent poem on this conversation in the colors of the original CATCH-22 book cover, printed this out, will frame it and hang it on the wall behind the screens where I do most of my trades.

It’ll hang it right between an A2 facsimile of Hergé’s L’Île Noire [![]() ]

]

and an original painting I picked up some more than 20 years ago at the flea market in Atlanta (the “Cafe Girl” by Erin Fitzhugh[![]() ]).

]).

Apologies, this was perhaps slightly beyond “simply stock trading”, but I love adding a bit of … color. ![]()

And I truly appreciate the Heller-Vonnegut insight referenced by @cubanpete!

![]() Which is in itself a nice allegory of the forbidden attractions of gothic things that usually only bring demise and are inhabited by monkeys …

Which is in itself a nice allegory of the forbidden attractions of gothic things that usually only bring demise and are inhabited by monkeys …

![]() I know that all of you know this painting already, but for those who somehow forgot, here’s your quick reminder:

I know that all of you know this painting already, but for those who somehow forgot, here’s your quick reminder:

1 Like

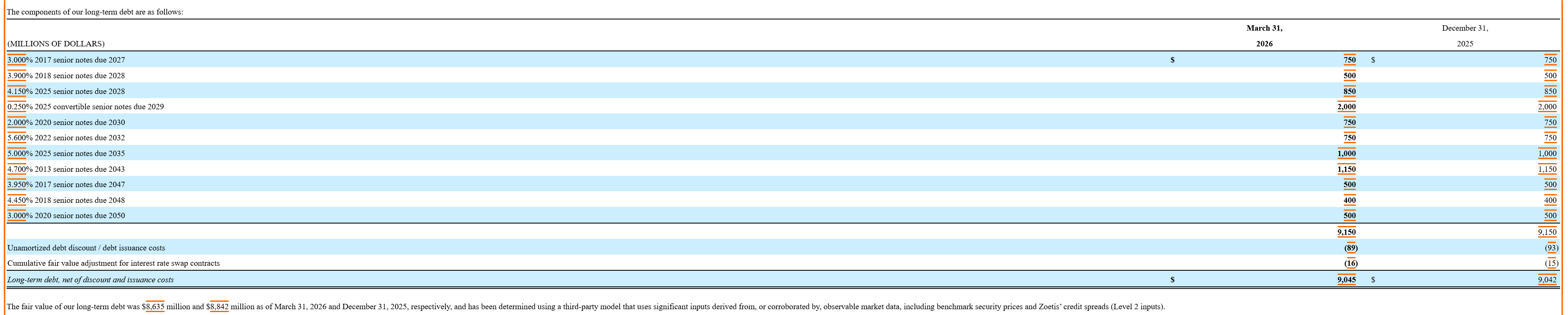

Any owners of or thoughts on Zoetis? Came across it recently as it was featured in the FASTgraphs newsletter.

Earnings:

Free Cash Flow:

Price:

Only thing I don’t like about them is their debt load (and the still relatively low’ish yield).

Long-term debt maturity schedule according to their lastest 10-Q filed on May 7 2026:

Looks manageable given their credit rating and steady cash flow?

Looks intriguing, but also the kind of stock I buy only for it to fall a lot more ![]()