Valuation is difficult on a stock that did fall down like a stone for that much time. Did they really do the turnaround? I tend to wait until such a stock starts to rise. We have tons of stocks that are not cheap at the moment and if one is that cheap it usually is for a reason.

Try to find that reason and then find out if the environment really did change. And personally I would just wait until the chart shows that it did really turn around. It does not matter what happened before you buy, I don’t care for leaving a few bucks on the table when buying. Most of the times trying to catch a low is a losers game.

I had to look it up – in case others don’t know: it’s apparently a technical chart pattern for trend following / momentum upwards if I’m not mistaken (I’m such an ignorant for charts and chart patterns – please accept my apologies if that’s incorrect).

Reverse Darvas stairs / box would thus be the stairs downwards, I guess … …?

Admittedly, I didn’t do much research on this company beyond reading the FASTgraphs newsletter and looking at the company through said tool in my post above.

According to that newsletter (highlighting mine):

What Happened: A 25% Single-Day Collapse

On May 7, Zoetis reported Q1 2026 earnings that missed on both the top and bottom line for the first time in years. Revenue of $2.3 billion grew just 3%. Adjusted EPS of $1.53 missed the $1.62 consensus by 5.6%. U.S. companion animal revenue declined 8% as pet owners pulled back on veterinary visits and premium products. Gross margins compressed. And management cut full-year 2026 revenue guidance to $9.68 to $9.96 billion, below the $10.2 billion analysts expected.

The stock dropped 25% in a single day, from $111 to $83. It has continued sliding to $81.32 as of last week. Over the past year, Zoetis is down 49%. Over three years, it’s down 21% annualized. Over five years, it’s down 13% annualized. The S&P 500 is up 29%, 22%, and 13% over those same periods. Zoetis has been one of the worst-performing large-cap healthcare stocks of the past five years.

I’m personally not really worried about the recent 25% single day collapse – on the contrary, that looks like an opportunity to me![] --, but more about the market apparently continuously rating the company lower for more than 2 years now … of course it was overvalued, but such a continuous price downtrend seems to suggest the market’s been smelling something else, perhaps.

I believe the “story” / narrative explanation for the extended P/E compression is that their business is what I would describe as “animal healthcare”, and while livestock (aka professional) healthcare (part of their business IIUC) is probably somewhat stable, their “companian animal” (aka pet) healthcare business might be facing trouble (or at least margin compression) for the gazillion of pet owners who might be facing hardship in the K shaped economy that we’re supposedly in (at least in the US), and who might bring their pet to the doctor less often.

Anyway, I’ve stated it before, I’m only a macro tourist, and the earnings (and FCF) estimates keep looking good, so for me the question would be whether the market’s been overreacting with the recent price chill. Looks like it (to me), but as @Phil_MCR points out, this might go on a little further.

My plan is to buy after @Phil_MCR has bought and after it’s then dipped a little more …

Had the company been on my radar and on a – in principle – buy rating after doing some deeper digging from here (I haven’t arrived at a buy conclusion with the little scratchin on the surface I’ve done so far), I’d probably have sold a “fear” put with a ridiculous premium.

A funny book from a dancer 1952 who traded stocks while on world tour. I think some of the telegrams of his brokers gave him problems for suspicions of some kind of code for spying. And he speaks of 2 million dollars of 1950 which by today would be like 27 millions.

It is an entertaining book that I did read a long long time ago:

I regularly catch myself looking up what a million dollars at time X would be equivalent to today.

Like, one hundred years ago, my total net worth would be a few hundred K in USD (about double in nominal CHF).[$]

Peanuts. Not even close to a real millionaire. Mostly the air in millionaire.

Oh, and only after drafting this reply and about to hit the “reply” button did I learn that the book you’re referencing is by Darvas who apparently coined the term for that chart pattern …

[$] This is dedicated to you, the dollar naysayers on this forum.

Maybe a dim outlook for the consumers will dent the earnings expectations a bit, but overall up and to the right?

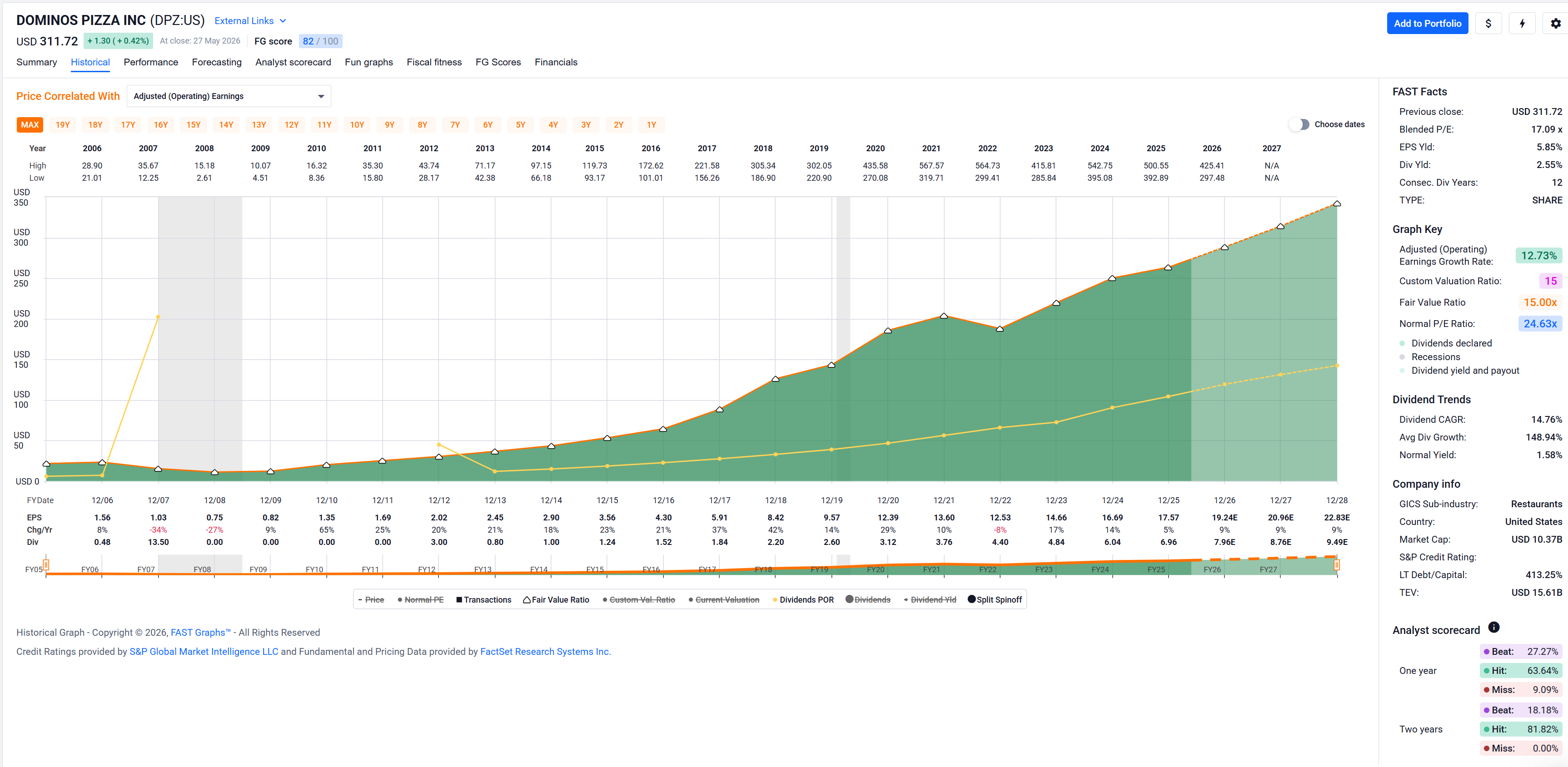

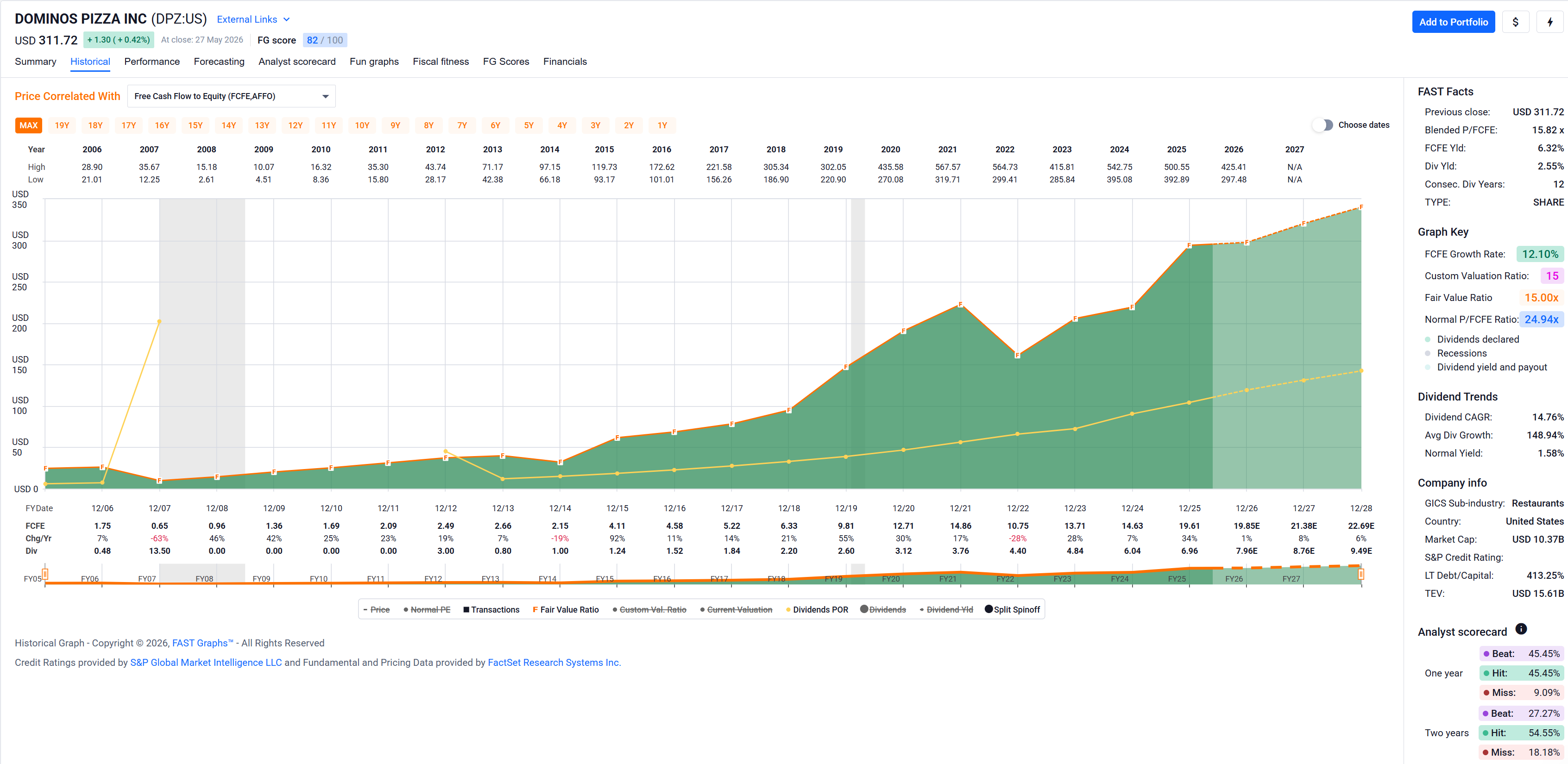

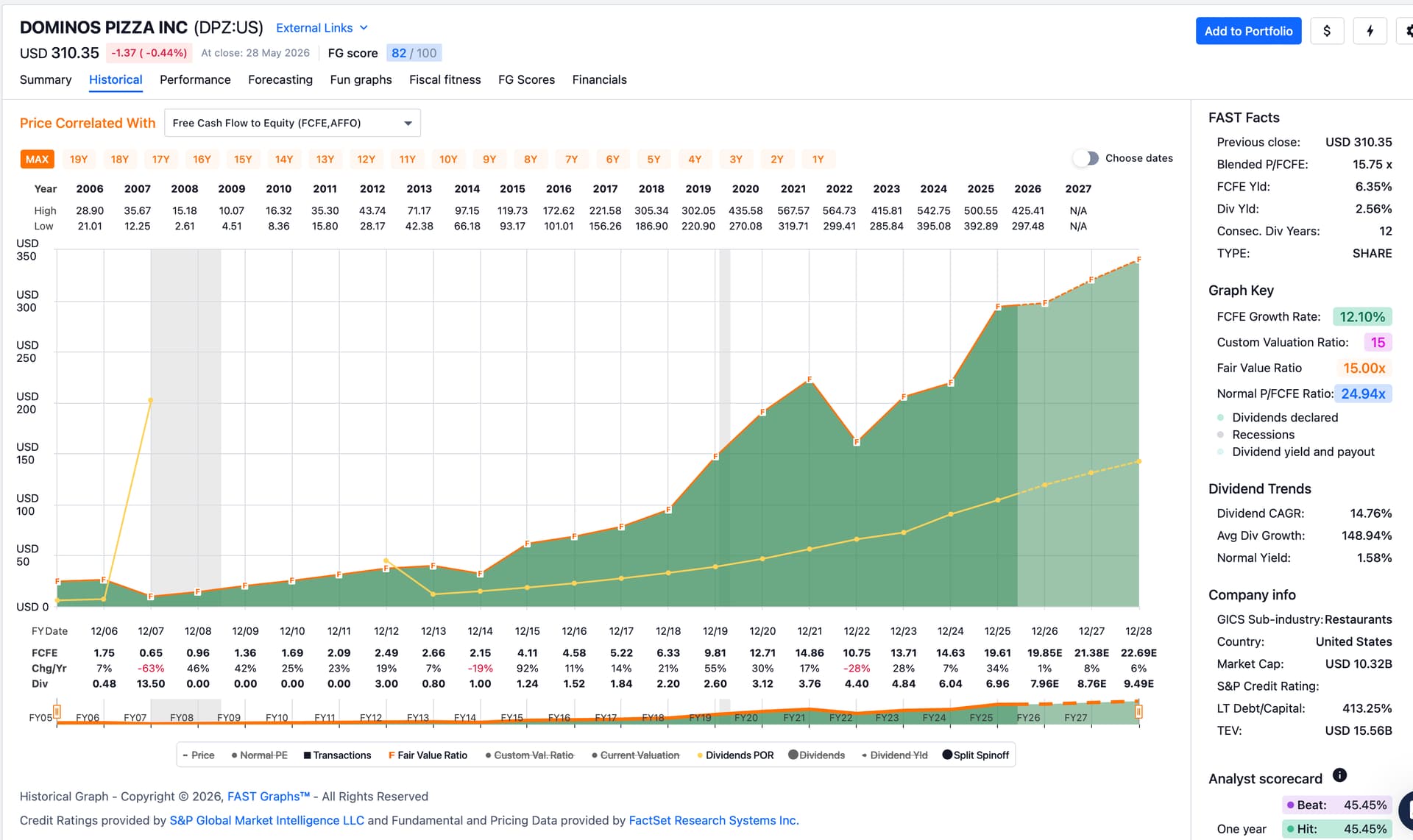

I picked this up from Nils Gajowiy, one of my mentors, and didn’t quite grok the long-term debt to equity situation, but apparently it’s not really an issue?

I love pizza. Sometimes I don’t know if I like the stock, or just like the product. I once had a junk food portfolio: DPZ, MCD, YUM, etc. I should have kept it, I’m sure it would have done well.

Dominos: I don’t invest normally in companies with a negative book value. Of course there is McDonalds which is actually a real estate company and had a negative book value like forever. It is just saved tax…

But then I made one of my best deals of my “youth” with pizza: owned Spanish Telepizza after the first going public in the 90’s until it went private again. Free pizza for life…

the problem is that under accounting rules, book value keeps real estate at original cost and doesn’t value them at market value, so you can’t sensibly use unadjusted book values for investment decisions.

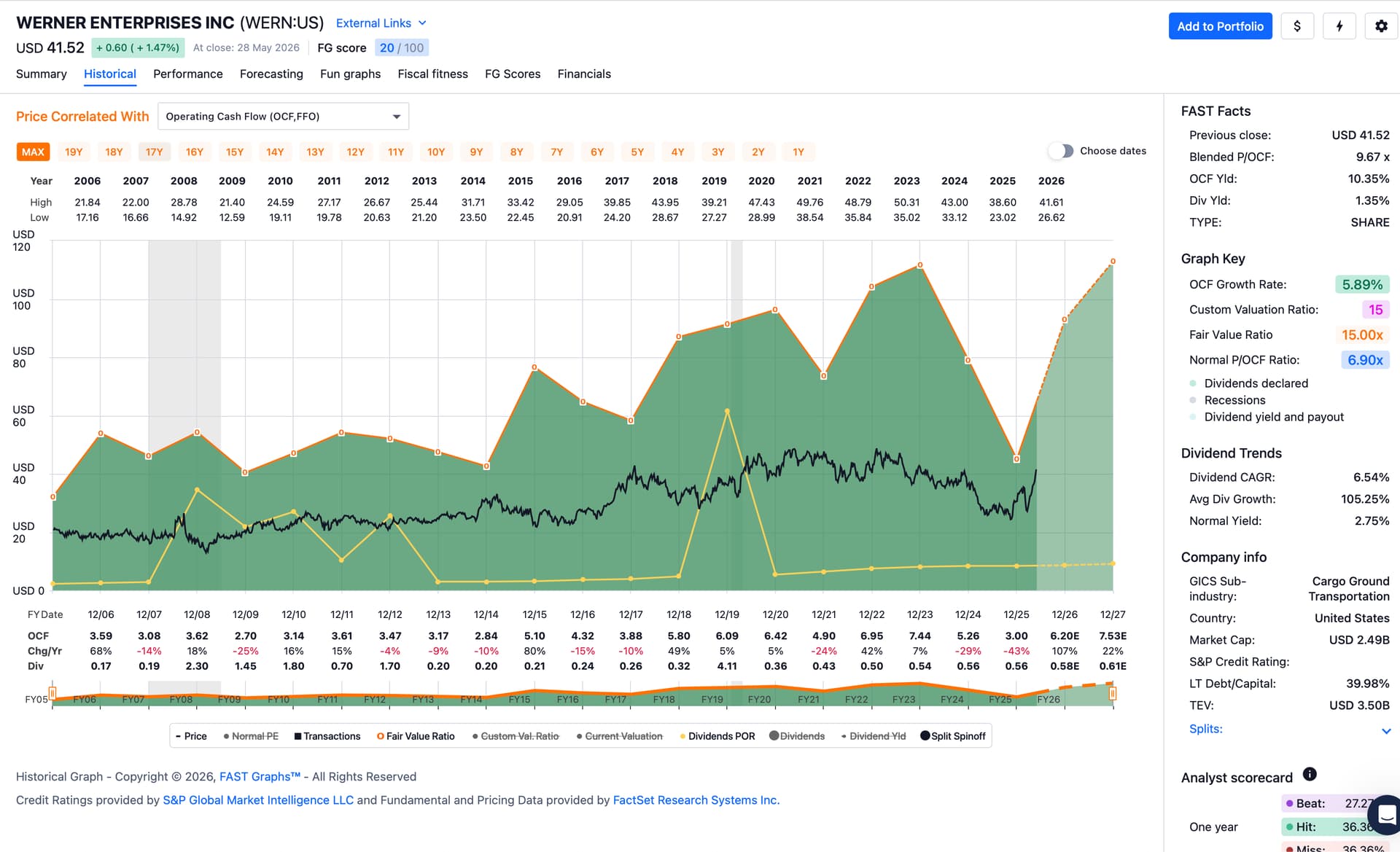

Gambling strategy: sold my Pagseguro today. Columbian finance shops seem to run better than the Brasilian ones. A little gain of around 5% after a year.

With the money I bought a few trucks: Werner Enterprises.

You can use anything for investment decisions. To analyze a company you have to find the “silent reserves” and add it to book value. However, negative book value is a warning sign. Remember the good old Dr. Doom Marc Faber when he commented on the negative value of Swissair. He said he would buy Swissair stock, but they would have to pay him to take the shares because there worth is negative. Sometimes he was right…

Thanks for pointing that out. I’ve asked Gemini to explain it to me and I’m coming away thinking that this number – long term debt to equity – is completely useless for a franchise business like this one.

Of course I’ll still pay attention if Mr. Doom issues a warning on DPZ … … for the moment, though, their FCF seems healthy enough that they won’t end up in a Swissair like situation – “all pizzas are grounded!”

using any equity ratio i suspect as the equity number needs adjustment (actually throw it away and calculate your own number from scratch) to be useful.

it might be better to look at interest cover ratios instead.

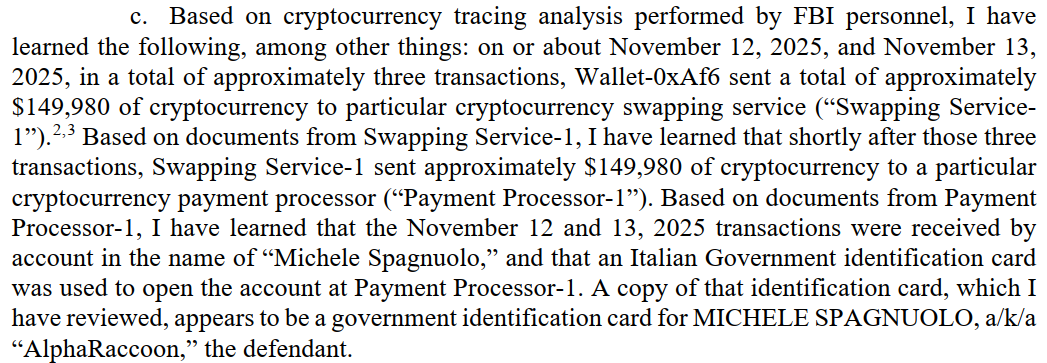

Today I came across a former colleague of mine featured in the WSJ, unfortunately in a sad way, but perhaps a good example of someone who also didn’t have the knowledge that he has enough: How Online Sleuthing Helped Catch the ‘Google Insider’ on Polymarket (gift unlocked article).

I’ve had many expressi with him in Google Zurich’s microkitchens, I know he has (had) a great paying job, making a ton from stock grants, on his way to FIRE … an yet he had to exploit Google insider information and place bets on Polymarket to add another million dollars or so … only to get caught, charged with money laundering and fraud with the end result of a probably ruined career.

This is United States of America versus the Defendant.

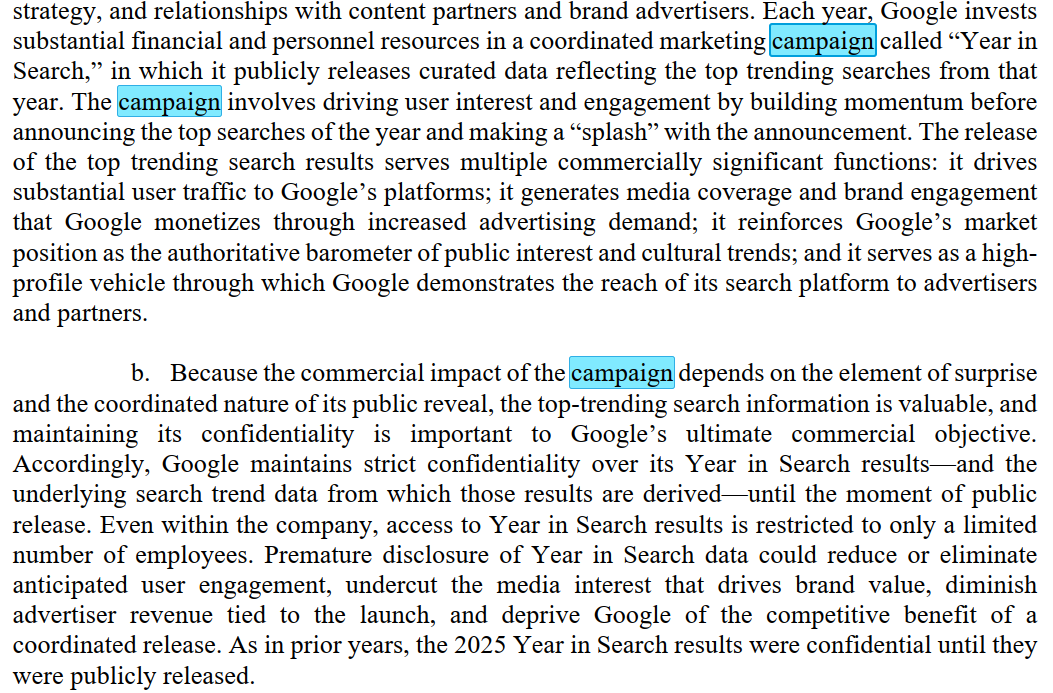

I wonder if Google could also file a complaint in Switzerland about using company data for personal purposes. The request for a warrant in the US list charges and implies that there may be monetary loses for google (Premature disclosure of Year in Search data could reduce or eliminate anticipated user engagement) if the confidential info is misused.

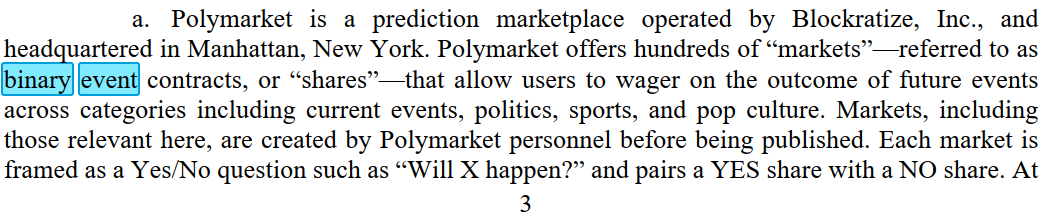

Yes, rules are clear since 4 years ago. The Commodity Futures Trading Commission said these “Polymarket bets” fall in the box of “off-exchange event-based binary options contracts”

The request for a warrant doc also mentions these “binary event contracts”

The tragedy here is that fraud in binary event contracts may be a slap in the hand and a fine. Concealing the earned money (money laundering) is the scary one.

Circle, the company that developed and operates USD Coin (USDC) is regulated by US law. Polymarket uses USA-issued USDC.

So, it’s the old story of “using the US financial system to do bad things even if you’re not physically there”. LIke the FIFA guys taking bribes in the Caribbean and South America. They did not take the bribes in the US, but the money passed through US banks.

PS: I’m learning about USDC. It’s a centralized crypto, fully traceable, must comply with AML and accounts can be frozen…so, it’s not crypto I retract my statement of whatever happens in crypto world stays in crypto world.

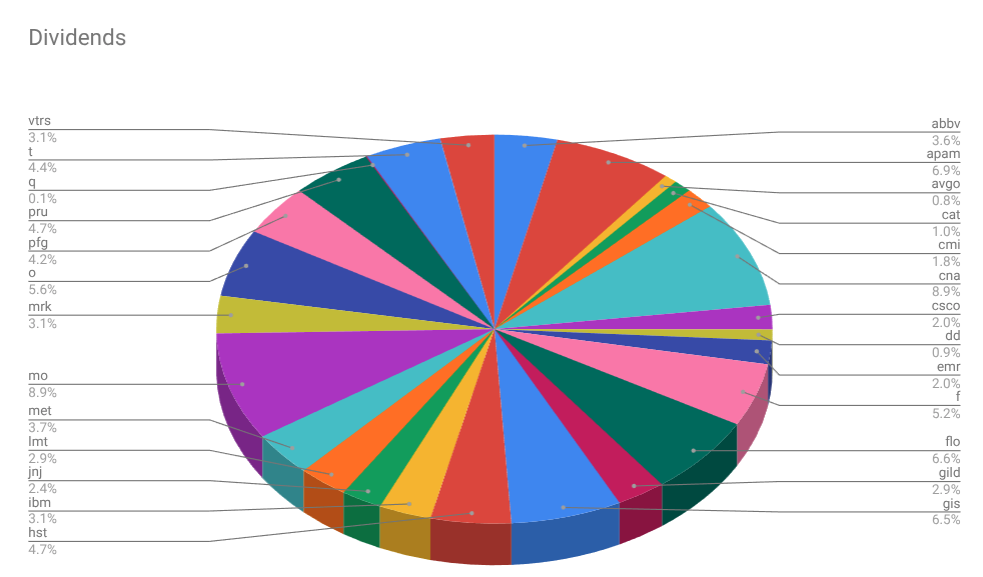

Dividends in May: ~$8.5k (+13.3̅% vs May last year)

May trades:

Ticker

Date

Buy

Sell

CHCT

05/04/2026

100

TSE:BNS

05/06/2026

9

CMI

05/07/2026

10

KDP

05/07/2026

50

MET

05/07/2026

15

CHCT

05/07/2026

100

TSCO

05/14/2026

100

TSN

05/14/2026

300

INGR

05/14/2026

70

OMC

05/14/2026

100

VICI

05/14/2026

100

CSCO

05/15/2026

52

AGM

05/15/2026

40

AMGN

05/18/2026

70

PAX

05/18/2026

1200

GPC

05/19/2026

25

SJM

05/20/2026

20

TSCO

05/21/2026

100

AMCR

05/21/2026

100

MAIN

05/22/2026

4

DPZ

05/23/2026

20

Also bought back on May 27 an AGM 125P NOV26 that I had sold on Feb 20 with a realized annualized return of 10.42% on the capital at risk (this trade is outside my dividend strategy).

Expected[𝔈] dividends in June: ~$17k (+37% versus June 2025)

Actually, it’s a joy.

$ The Returns tab usually has a lag time of a couple of days after month’s end.

[𝔈] $16.1k have already been declared. AVGO and GWO haven’t declared their dividend yet but should bring in another $800 or so.

You do trade a lot, but I suppose it is systematic.

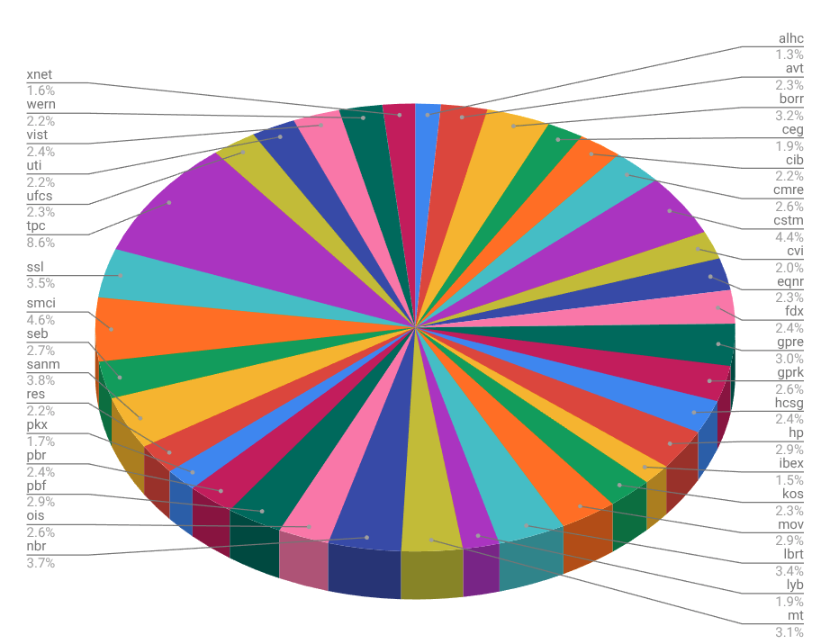

I did publish the trades near term, this month I think there was only the “market dividend” trade on Cisco for the dividend portfolio and in the gambling strategy a partial sell of CVI (“the rent”) after one year and new positions in AVT, PKX and WERN and complete sells of GIC, AVNW, DLTR, STRT and PAGS.

I do not count the dividends but the total carry premium which is dividends + market dividends - tax - debt interest. This is more or less the free cash flow. Last year the dividend strategy gave me $13’059 net carry premium per month. This year that number is only at $7’647 because there has been only 3 market dividends until now. But it is only May/June…