Low valuation, strong cashflow and profitability, low growth is supplemented with stock buybacks.

You wanted arguments against a buy of CARG:

P/E is lower every year, that is true and may be for a reason because business seems to go down. P/S is at 3.11, same as when P/E was at 145, that means they make less out of the sales. And then the bookkeeping tricks, like 11 times book value compared to 5 times a year ago.

It is not cheap, loses business and is in a business without having an edge, where almost everybody can enter.

You mean negative growth of earnings…

It is OK for a lottery ticket, but I don’t see a real edge anywhere.

More than the complete FCF is used to buy own shares, probably to avoid them sinking more. Profitability seems to be on the way down.

1 Like

US interest rates were put on hold, as anticipated.

There is a ‘deal’ between US & Iran.

Oil tankers appear to be ‘moving’ again through SoH.

Why are oil prices are barely dropping … The US market going down …?

That’s a clear statement. Still, I’m wondering if you have any pointer to success or good vs. bad performance.

Do any of you own or like Sonoco? They pay a nice dividend and for over 40 years already.

They make packaging products. Looks a bit boring, but I like boring as long as they make good profits and pay dividends.

Any reason to stay away from it?

Sonoco has been on my watchlist since ~forever.

I like their yield, I really like their (severe?) undervaluation, I like that they’re mostly under the radar (not in any major index).

I dislike their recent tiny tiny dividend hikes (please use a magnifying glass ![]() to spot them), barely keeping up with inflation.

to spot them), barely keeping up with inflation.

Not sure why the market’s been discounting them for the past several years now. Anyway, I am not a chart guy, so …

In summary, looks buyable to me.

SON:

I would want to buy it much more expensive. But then a look at the balance sheet makes me shake my head. Seems like all the stockholders money is already in the pockets of other companies Sonoco did buy.

There are more than enough cheap companies around. But they probably are cheap for a reason, especially after such a long bull market with new highs everywhere.

1 Like

On mine too, but I always avoided it, some spidy-sense telling me there’s something not right there.

1 Like

It’s apparently Michael Burry’s birthday and he’s sharing an article that is usally behind a substack paywall.

I enjoyed it. It’s long. It repeats some of the already known skepticism one can have around the AI business cycle, but what really surprised me most is that even some of the Life Insurance businesses in my own portfolio (like MET or PRU) might be affected if this all goes belly-up.

Excerpt:

So, as it is, the next buyer of AI risk, the next funding source, does not look like an AI company at all. It may come from the most staid and boring insurance companies on earth, the life insurers.

Life insurance is already helping to finance the AI data center buildout. MetLife has been issuing data-center-backed asset-backed securities (ABS) collateralized (backed) by lease income over a 15-19 year term.

MetLife does this because it sells long-duration retirement annuities to American workers, and that requires long-duration assets to offset the annuity liability and ultimately fund the payments for the annuity. In the past, this meant corporate bonds, mortgages, as in the above charts. Increasingly now it means data center ABS, which fund AI data center builds.

These funds take an offshore detour, however. Over the last few years, since about 2023, the start of the AI boom, more than 200 captive insurance companies have sprung up in Bermuda.

So, when MetLife issues those annuities, it sets up an entity in Bermuda that it controls. The U.S. insurer MetLife then cedes risk to the Bermuda reinsurance entity, which is a captive reinsurer because it exists to reinsure insurance policy liabilities of the parent (MetLife).

This gives me food for thought whether I should dial back on some of the Life Insurance businesses in my portfolio … I’m not in a hurry as I believe this bubble won’t pop anytime soon, but still, maybe just shift some of that stuff to even more boring businesses.

2 Likes

I heard that private equity have been buying up insurance companies and then pushing risk offshore to Caymans where there are more lax rules.

2 Likes

Still in the middle of reading it, but funny that he mentions bull-whip effect. That was exactly was I was thinking earlier this week: similar to covid, are we seeing an AI supply chain bull-whip effect which is spreading out and hitting component suppliers like Micron and Sandisk, and whether a massive crash is therefore coming.

ACN down nearly 20% today. Down over 50% YTD. ![]()

I feel they’ve already nicely dropped. Not yet February 2026 levels, but on its way?

Probably depends how the next couple of months play out, with both sides’ erratic leaders at the helm … though I suspect the closer the mid-terms, the less erratic the orange one will behave.

I usually don’t watch this space much, as it’s a macro thing that I don’t really know how to trade … plus I’m anyways an investor, not a trader.

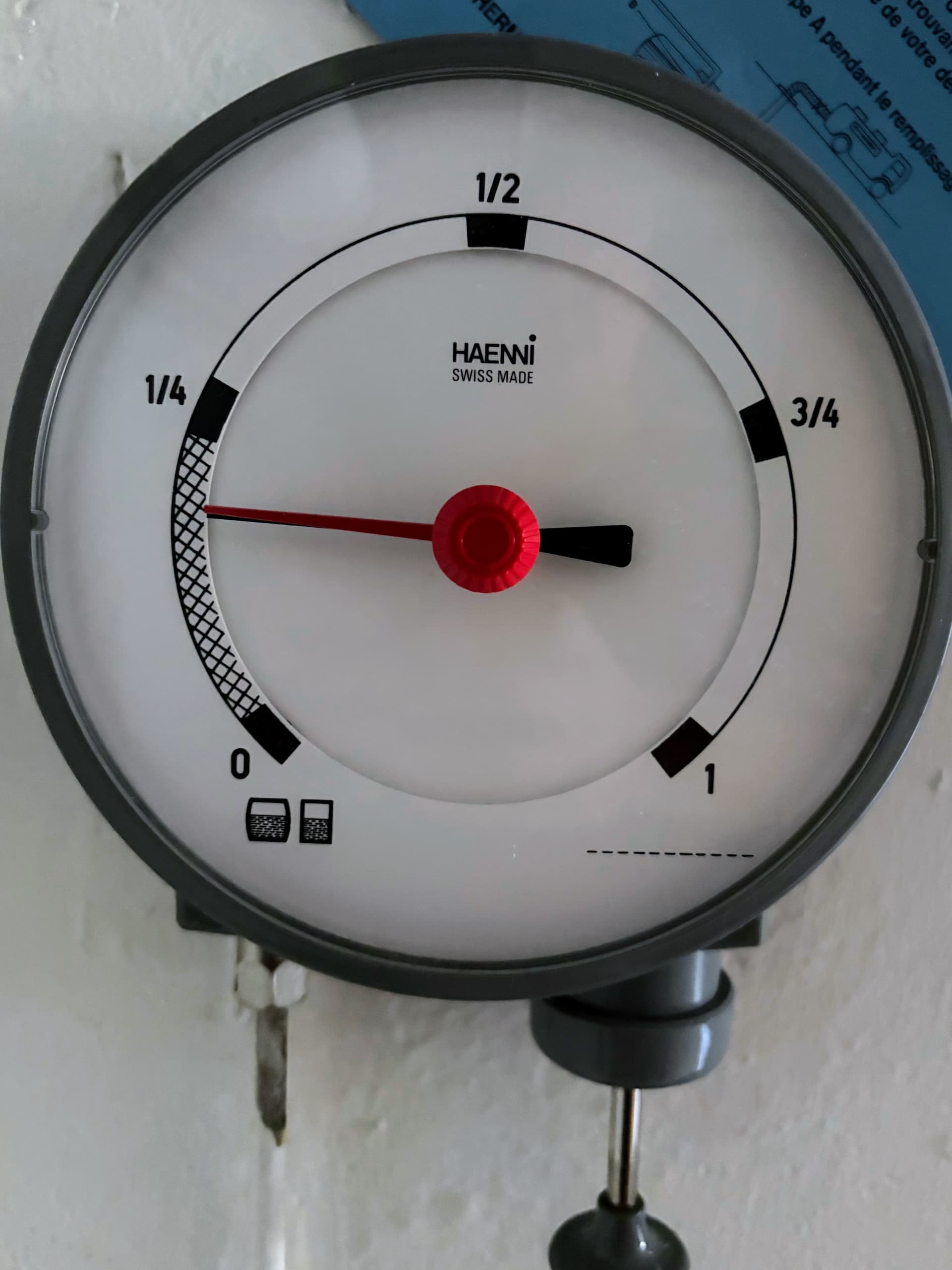

In this case, though, I’ve paid more attention to the (heating) oil price as our heating oil tank was maybe just a quarter full when I checked in February. Price per 100l was at the usual somewhere below 100 CHF.

Decided I’d wait with ordering until after our then already planned vacation to avoid the hassle with finding a delivery date after we would be back from vacation.

Then bombs fell. Goofy regretted not locking in the low price in February … and kept checking the fuel tank gauge regularly … especially when it was cold outside.

Now it’s definitely warm, no heating required as far as the eye can see, and the fuel tank gauge still looks fine.

Turns out Goofy is a little bit of a trader after all … ![]()

P.S.: Hope I’m not jinxing it …

Overheard this on Twitter earlier today:

“Accenture now needs McKinsey consultants …”

A little Schadenfreude chuckle emerged from Goofy’s belly.

Edit: Didn’t mean to ding any shareholders. Just have some chilling thoughts on the consulting business with the structure of McKinsey et al.

Skip to my Stock picks for the week section below if you are not interested in my caffeine scented noise.

I jinxed it, obviously.

More seriously, I expect this – and perhaps other new distractions – to continue until somewhat close to the mid term elections. It’s a suitable deflection from e.g. the Epstein files and perhaps other more recent policy mistakes.

</conspiracy theory>

Still a fine time window to seeking a local bottom in heating oil for filling up our tank. ![]()

Anyways, back to the topic title.

It’s a slow and hot Sunday, but after chilling in the Limmat this (early) morning at a still acceptable 23°C and downing a Cappuccino[![]() ] and a Gipfeli for CHF 8.50

] and a Gipfeli for CHF 8.50 ![]() in a self-service restaurant/bar aptly named the Panama Bar …

in a self-service restaurant/bar aptly named the Panama Bar …

… I retreated to a large screen and my dearest hobby: stock picking.

Stock picks for the week

My updated potential buy list (from the universe I already own) for next week (mostly to shift some BND dead money to real assets):

| Ticker |

|---|

| CHCT |

| CI |

| CME |

| CSWC |

| DPZ |

| EIX |

| FLNG |

| GIS |

| IIPR |

| LON:IMB |

| INGR |

| LON:LGEN |

| MAIN |

| MO |

| MPT |

| NNN |

| O |

| OMC |

| OZK |

| PAX |

| PEP |

| TSE:POW |

| SJM |

| SGX:U11 |

| TSCO |

| VICI |

| VZ |

Just because something is on this list does not mean I will buy it.

Oh, and I hesitate to mention my new adventure: as some of you know (and frown upon), I also have significant holdings in VXUS. This has recently ballooned, the yield has cratered, and I feel some of this holding might be reduced in favor of some more yielding – still “international” – companies.

I’m only in my exploratory phase so far, a couple of Japanese companies have showed up on the radar (purely to them being numeric stock tickers showing up alphabetically before any others), but if you have thoughts on this potential portfolio shift, fire away.

[![]() ] The cappuccio was served without cacao powder. While my wife’s cappuccio was prepared and served (without cacao powder), I intensely scanned scanned their entire coffee station (a push button coffee machine …

] The cappuccio was served without cacao powder. While my wife’s cappuccio was prepared and served (without cacao powder), I intensely scanned scanned their entire coffee station (a push button coffee machine … ![]() ) for the cocoa dispenser. Finally spotted it by the time my cappuccio was served and asked for it.

) for the cocoa dispenser. Finally spotted it by the time my cappuccio was served and asked for it.

The guy at the bar was seriously challenged by my question but was able to hand it to me after I pointed to it with my arms and fingers.

1 Like

I’m sorry for the split of Bob Marley’s chemical plant. Wednesday they do that and I hate it as always: one to three, why??? OK, I get some shares that I probably don’t want, I did not want Dupont shares at all, but it is just money so I did just take it.

Chicos, try to make real money for me and I keep being your owner,

Sorry, that was DuPont (DD)

1 Like

Is it tax free?

Sorry, I know where the door is. I’m on my way…

1 Like

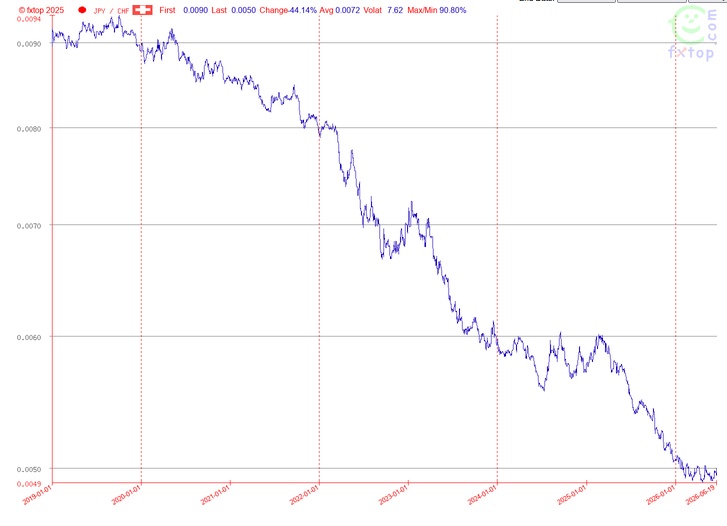

JPY/CHF exchange rate (log scale). The picture is very similar against the USD though a tad less linear.

The weak yen would have caused a 10% headwind since 2020. According to my AI, Japan’s central bank doesn’t plan to change its monetary policy.

Don’t believe a statistic that you did not falsify yourself.

I lost a lot of money changing my debt from USD to CHF. But then I pay a lot less for the interest. But fuck, it hurts, why do we have to live in a country that really cares about it’s money?

All money went down compared to the USD really all… except the CHF. Since world war one.

Well, exchange rates were fixed (and AFAIA hardly ever adjusted) until 1971 when the Bretton Woods agreement fell apart. They didn’t float (more or less) freely until 1973.