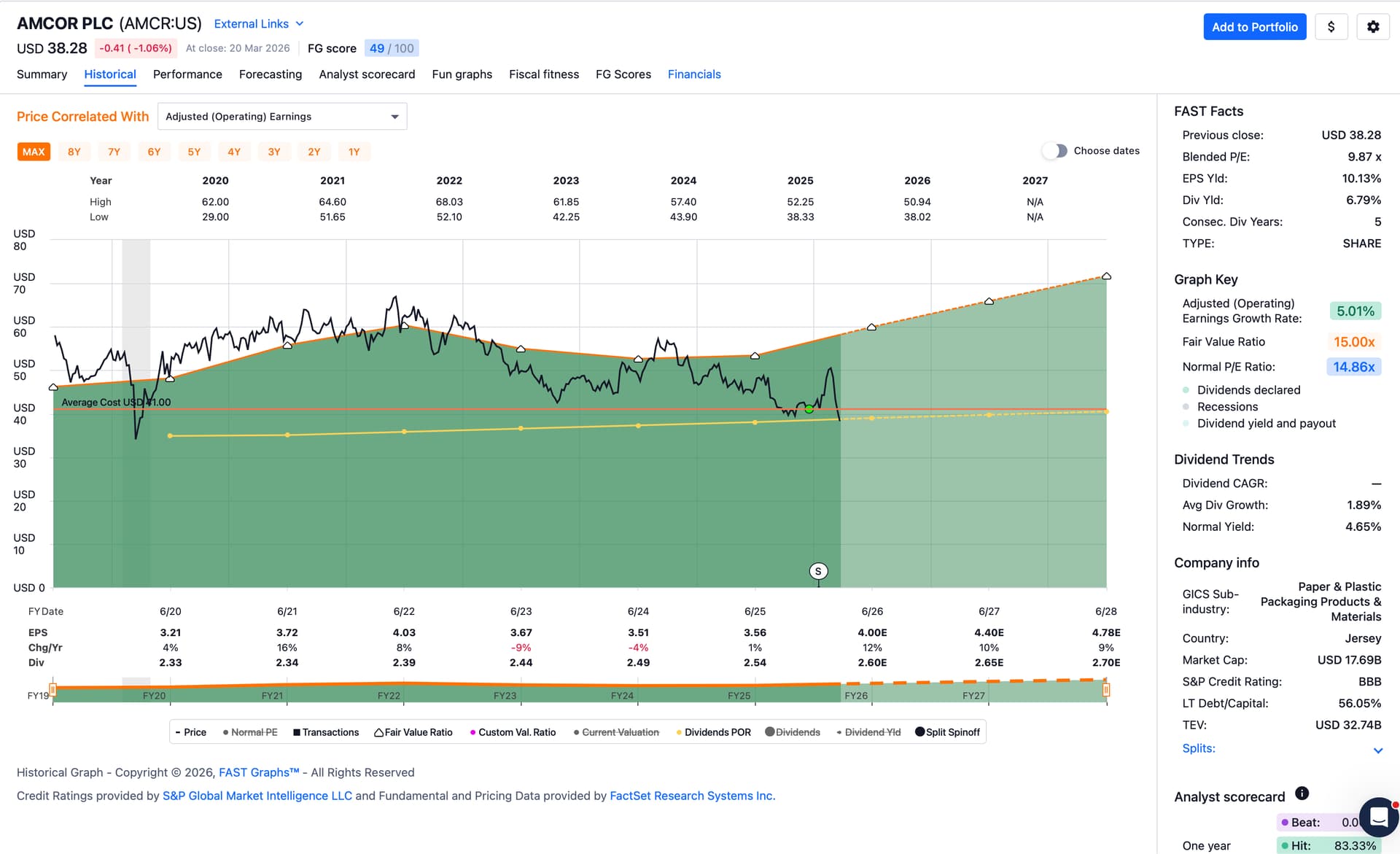

GIS is on my buy list, has been for weeks months.

Didn’t pull the trigger, yet, recently – their earnings outlook could look nicer, pointing more upwards at least two years out or so. Anyway, I’ve bought them at higher prices so should probably average down as long as my position is not full yet.

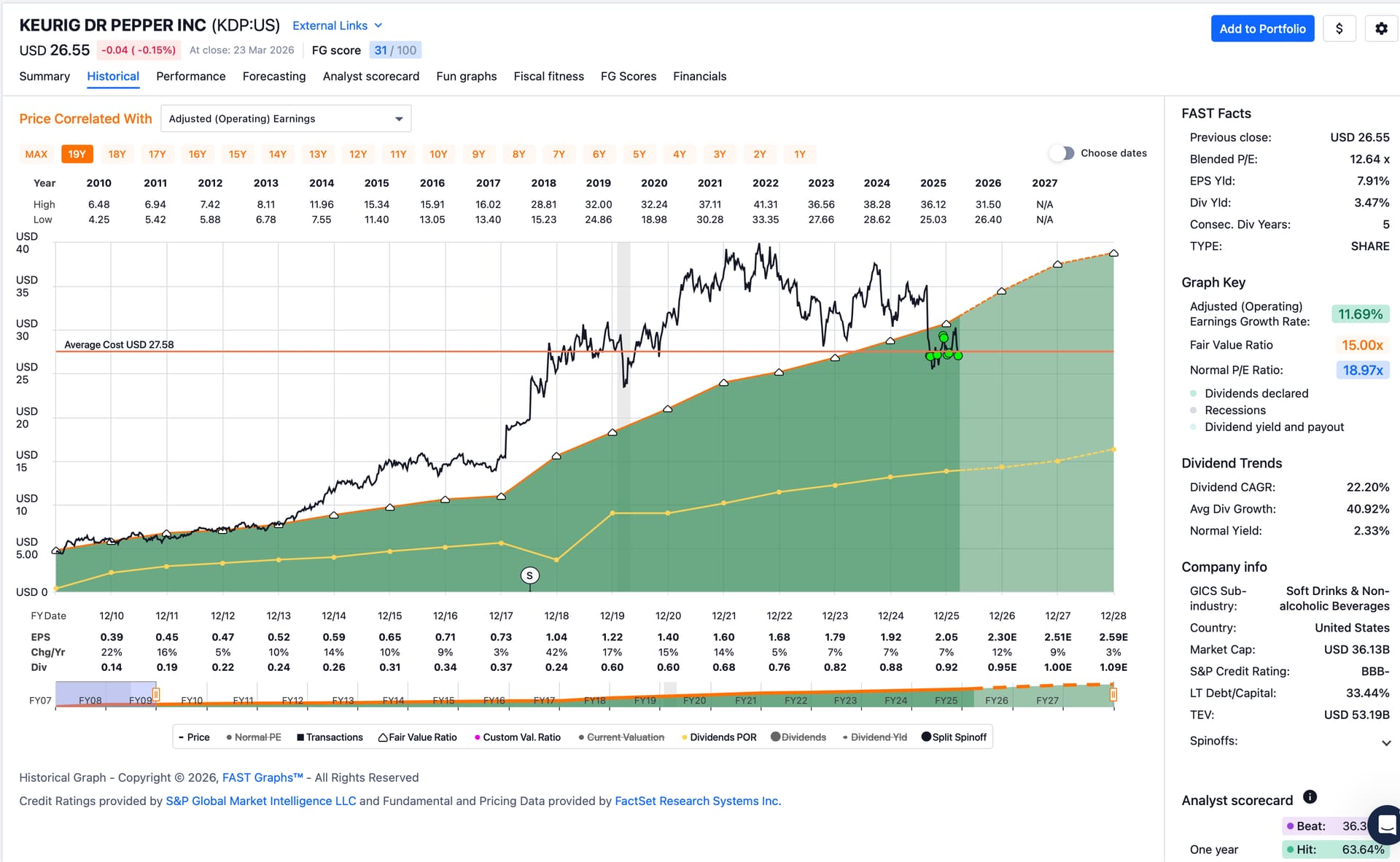

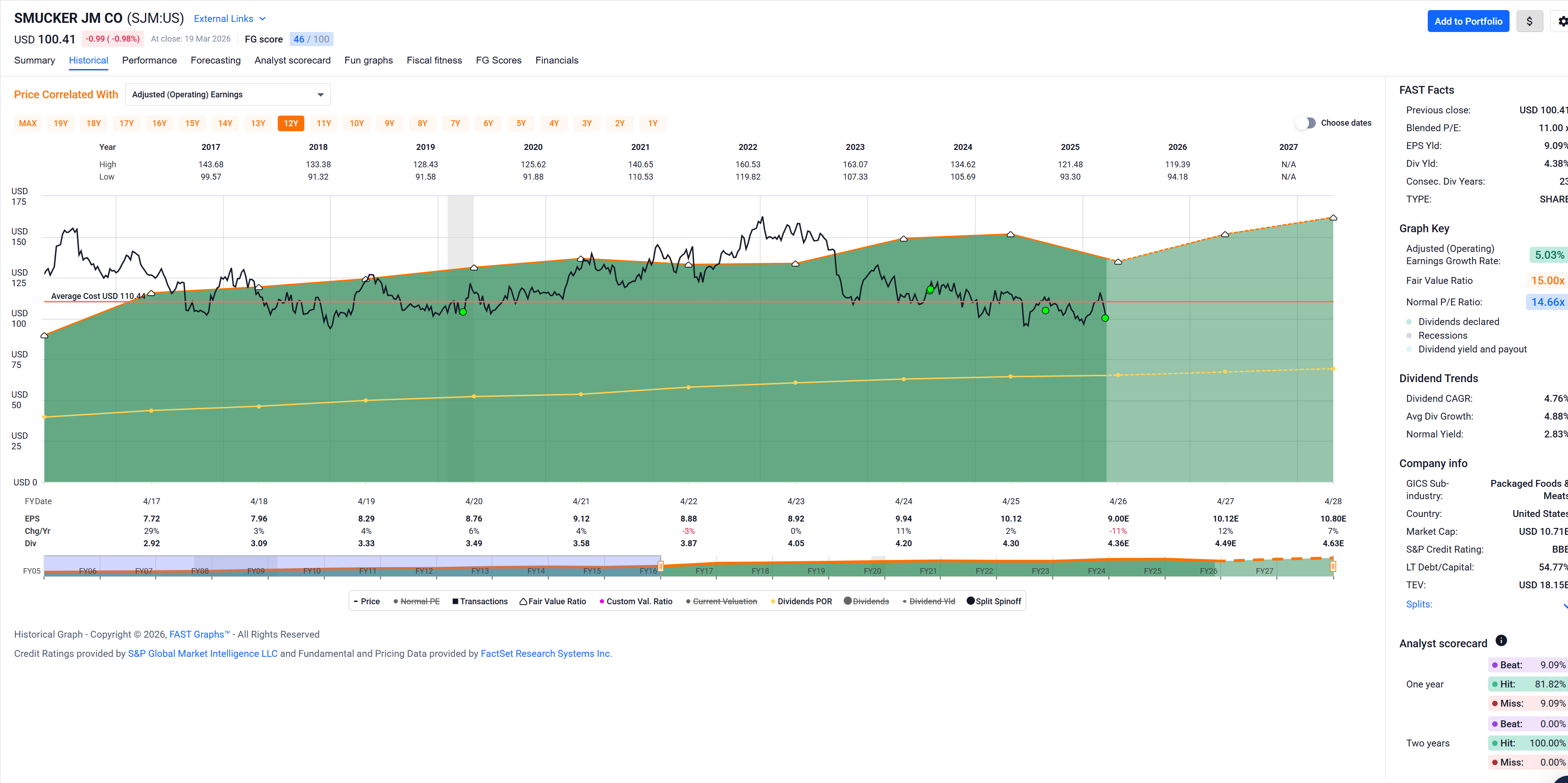

Other seemingly even prettier brides turned my head recently, though. Smucker, Keurig and Community Healthcare Trust were the promiscous cuties I bought into a bit more this week:

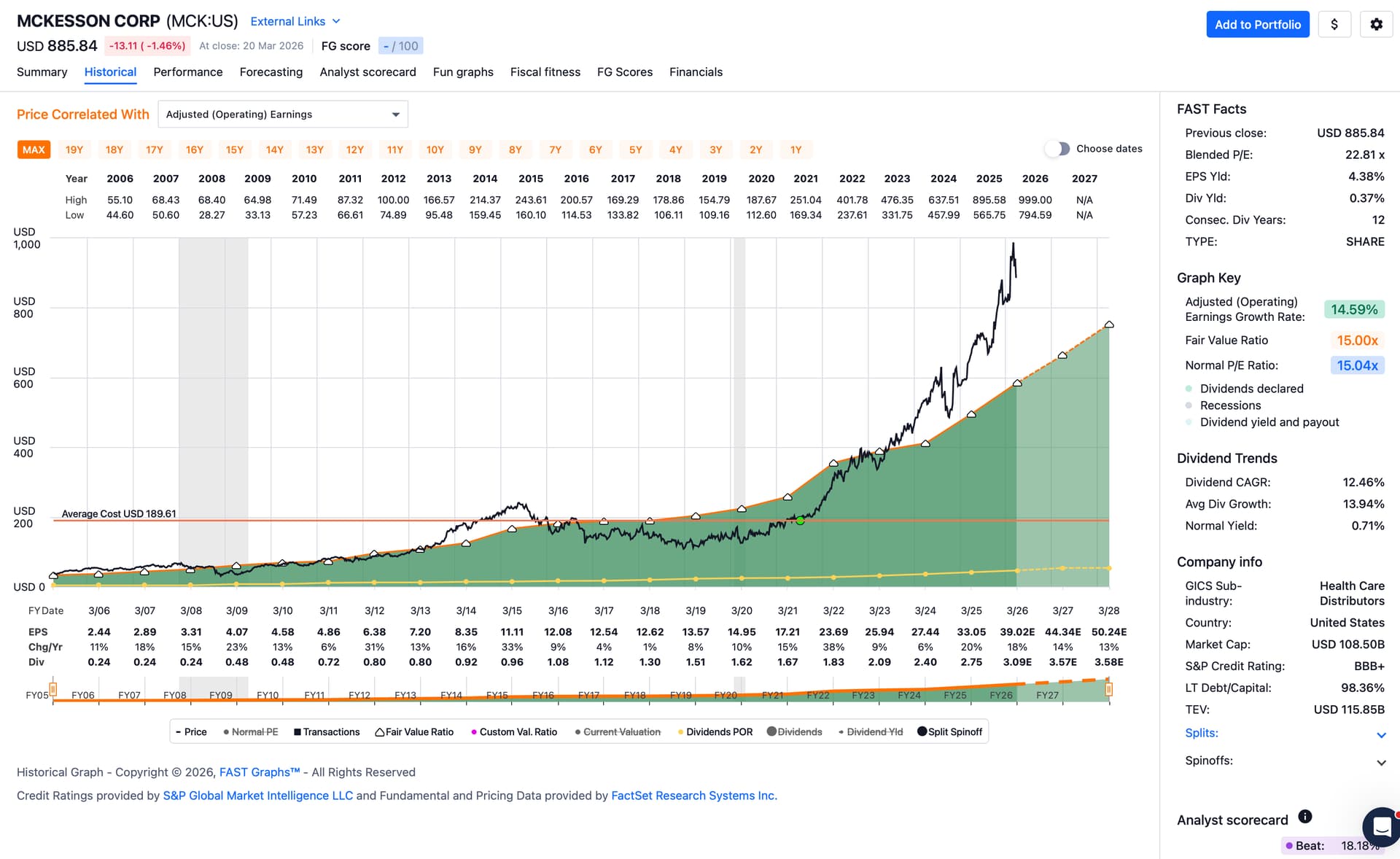

Look at those big … uh, dividends!

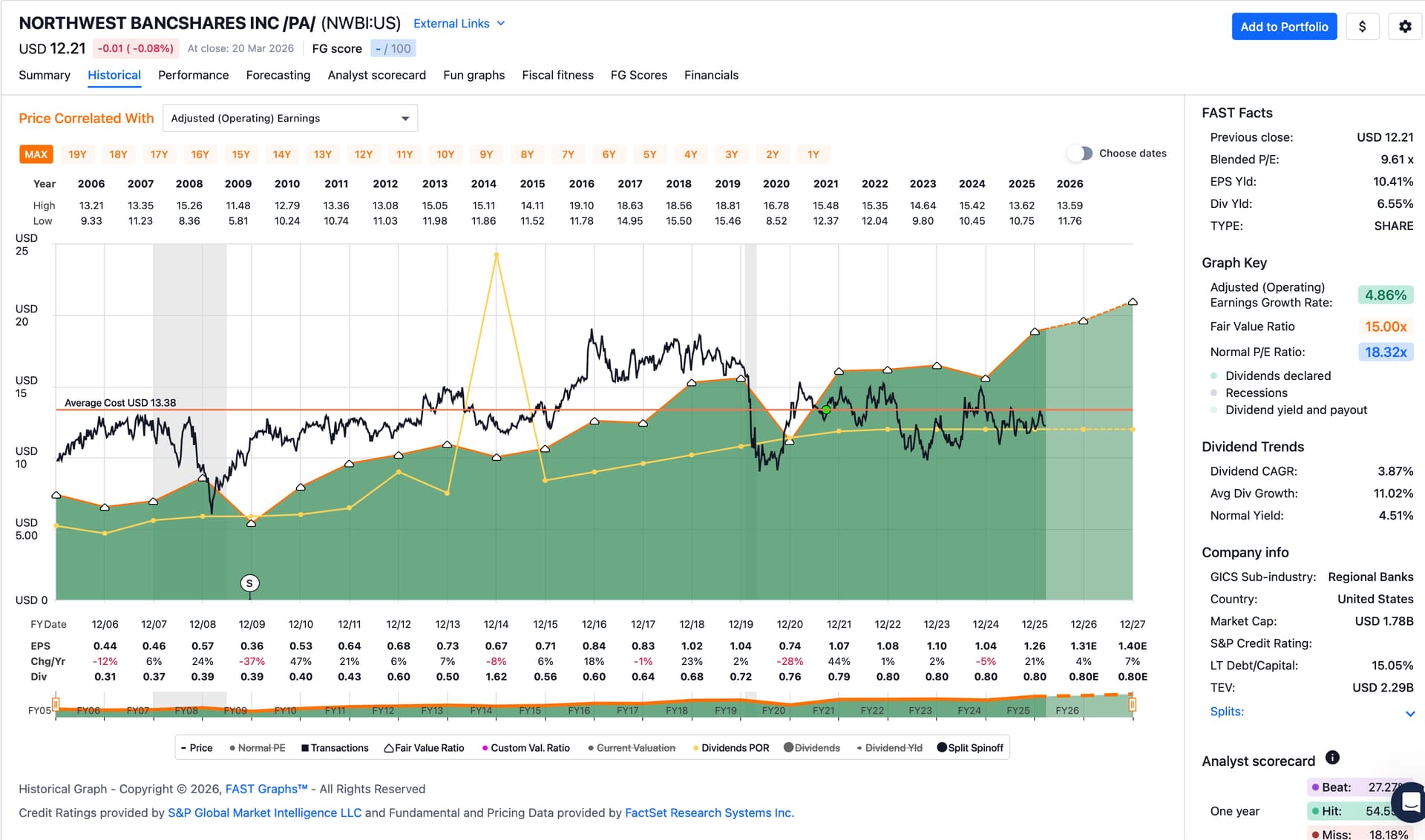

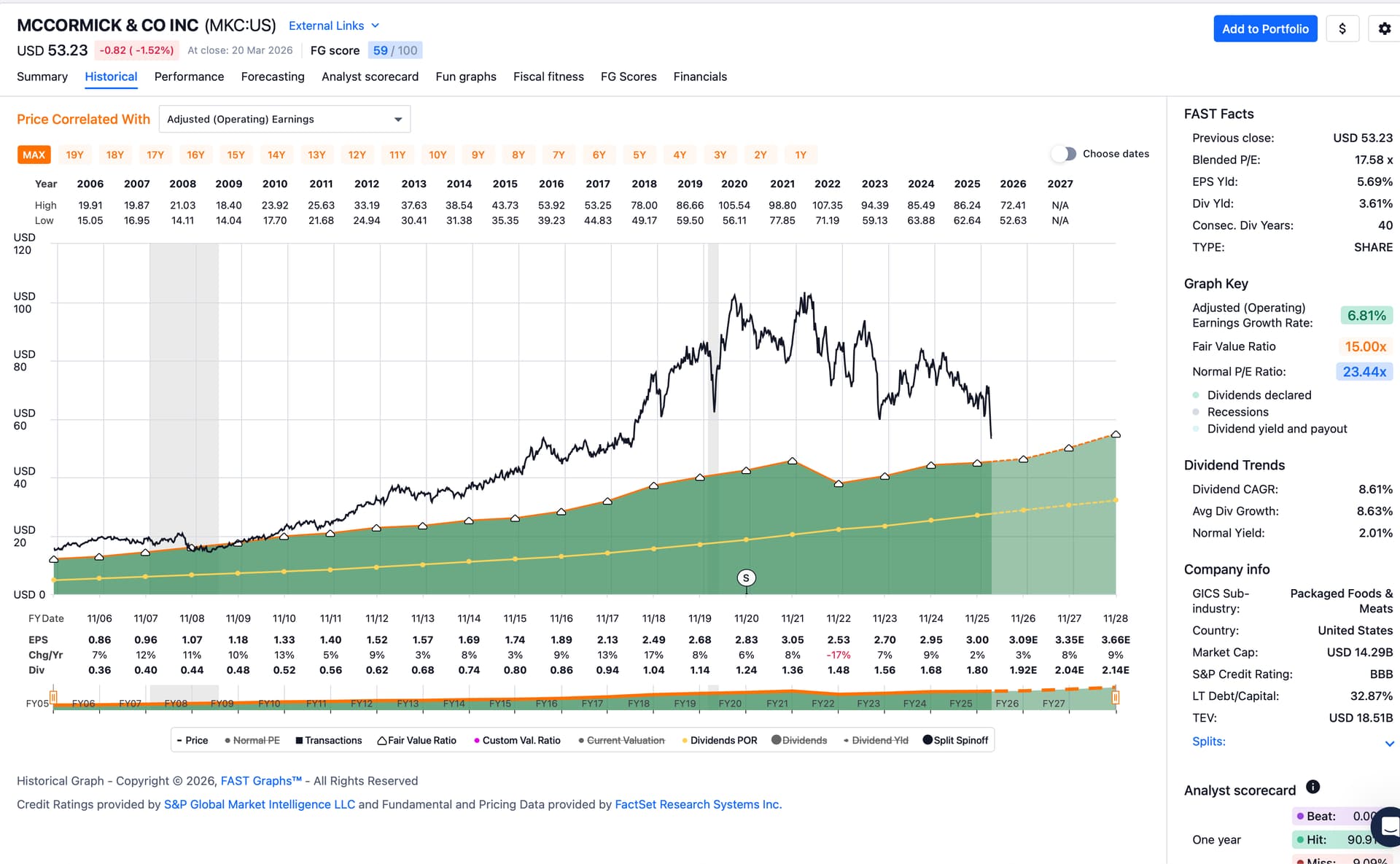

Dividend CAGR is on fire!

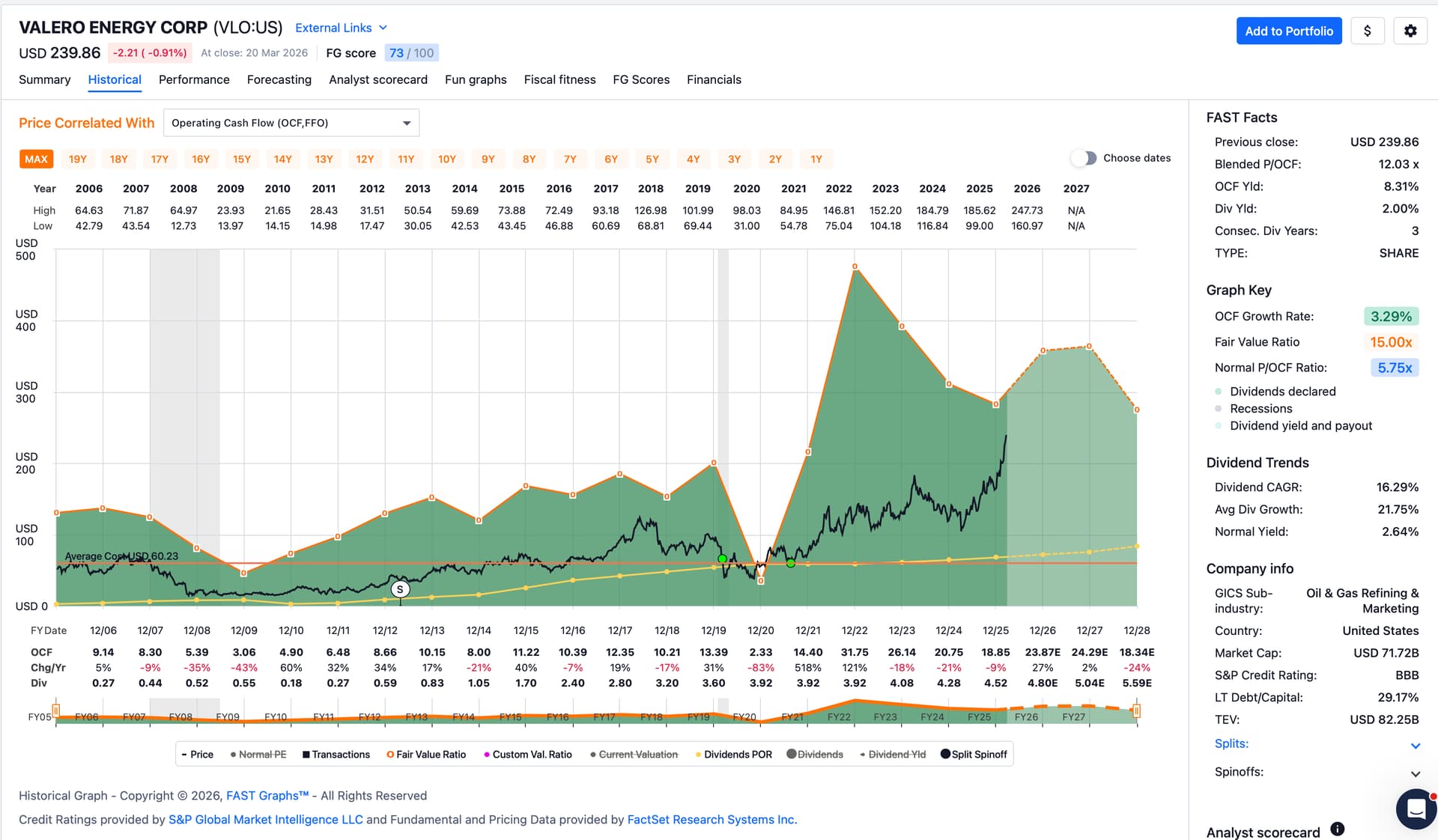

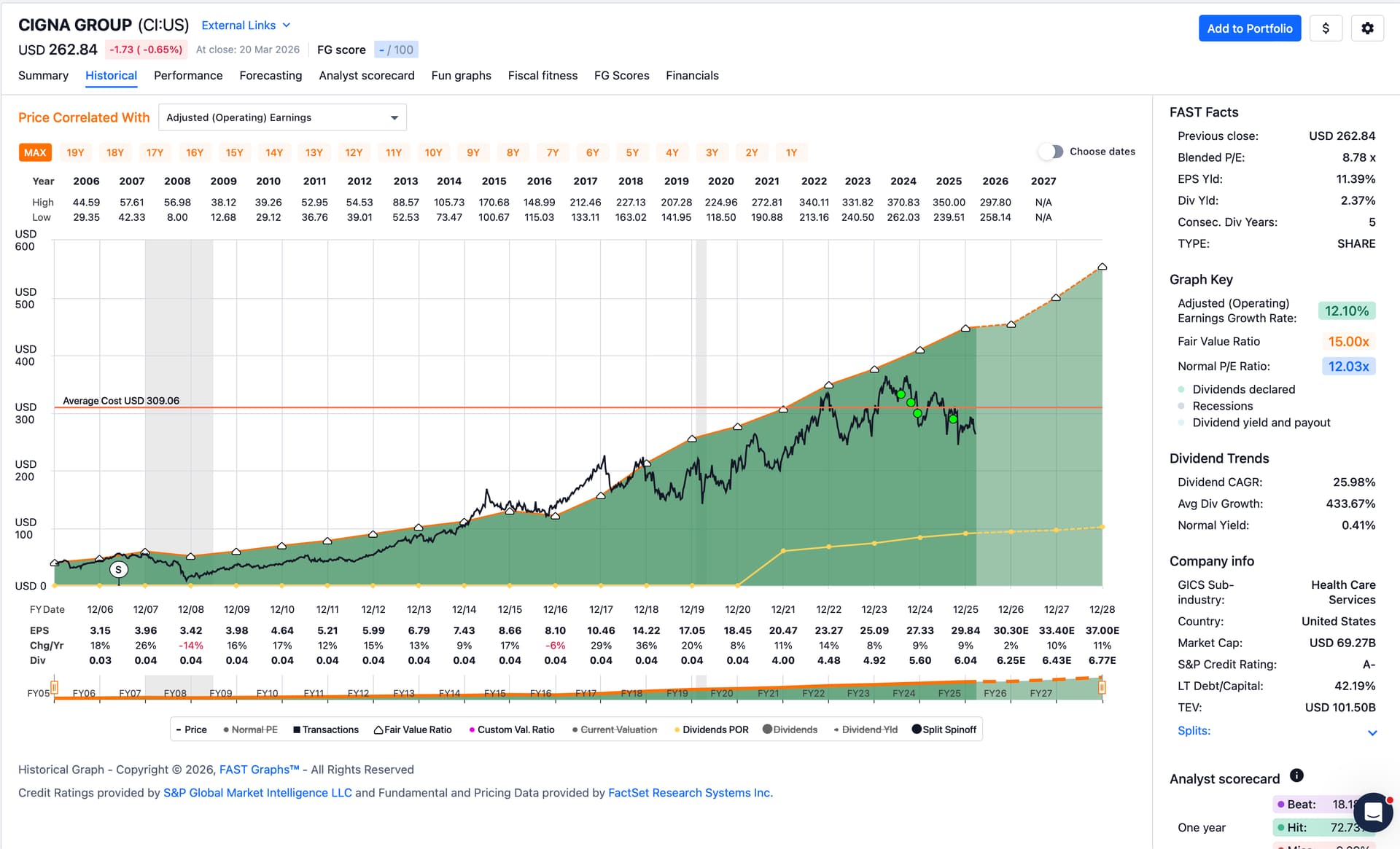

Sweet, sweet dividend – love it!

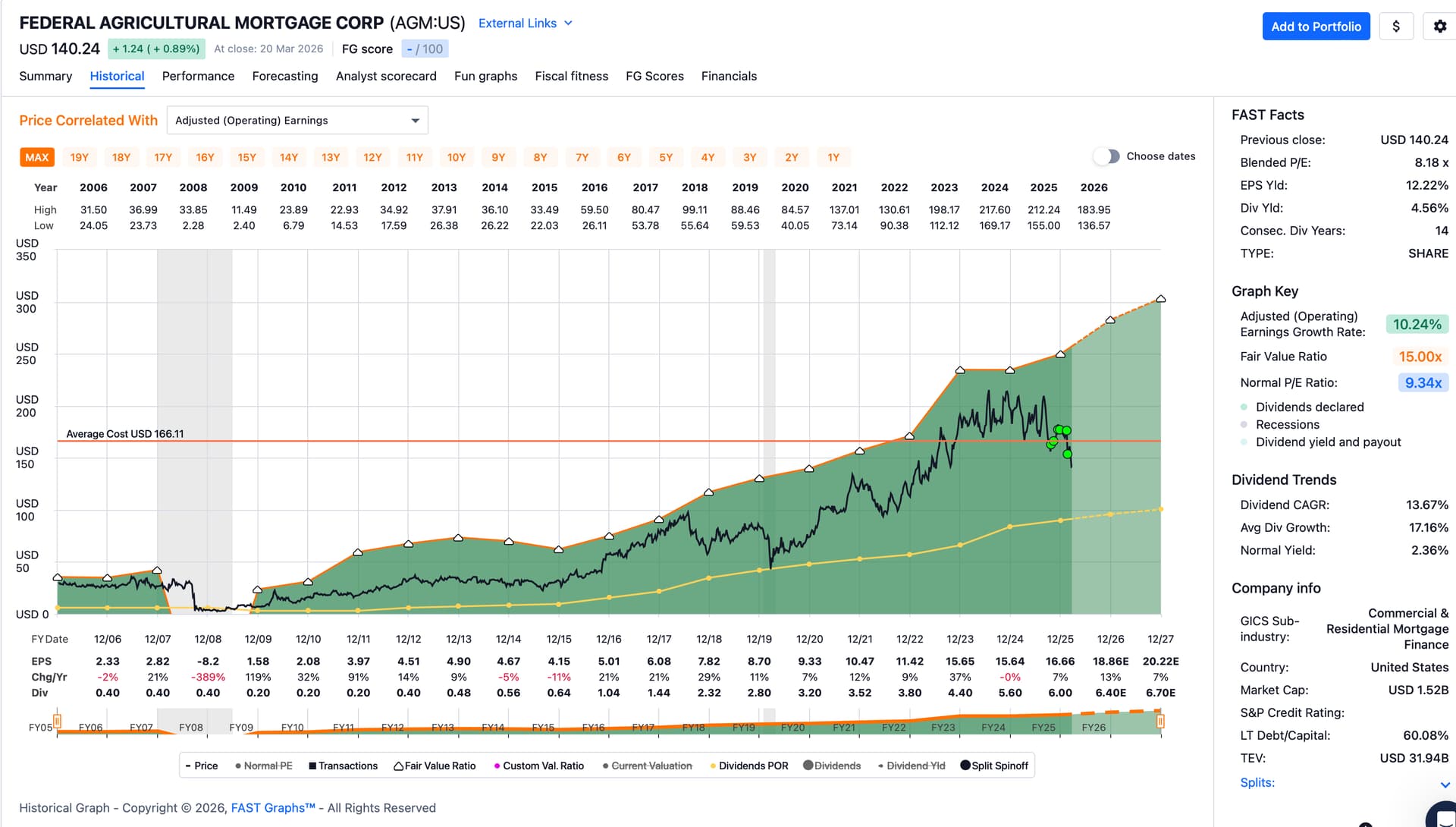

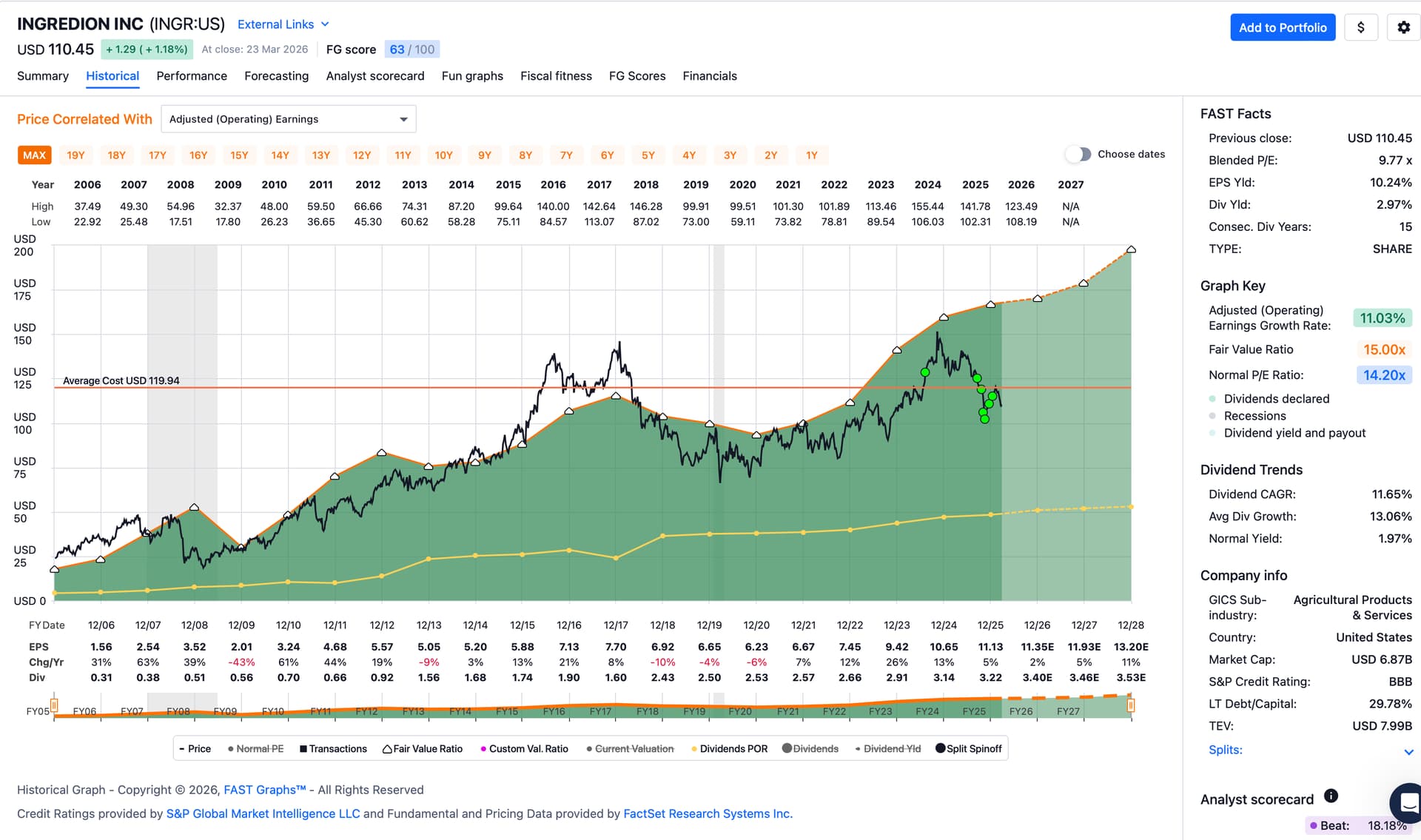

Amen!

I was already scared when their first cockroach showed up – Hindenburg research report released in August 2024 about balance sheet manipulation – and wasn’t very surprised when the second cockroach surfaced (EY withdrawing as their auditor). 3rd ‘roach was the DOJ looking at them in October 2024 and the last one just now … good ol’ smuggling! In the age of AI!!

Cockroach marriage in heaven, I guess … ![]()

To quote Warren:

“In the world of business, bad news oracles are rarely soliloquists. You will find that there is almost never just one cockroach in the kitchen.”

Anyway, might work fine for a speculative portfolio, but I’m afraid no ('Roach Motel) room in my dividend (growth) approach even though I am fascinated by those companies and their (expected) growth in earnings.