I really thought a lot about my harsh words on the holy grail investors. As I said, I am a contrarian. But then the phrase “We don’t like things because they are true; we think they are true because we like them!” describes pretty much what happened to me and my comments about the holy grail the last decade.

At the beginning I was maybe alone with my warnings, probably ten to a million. Then it went further down because of the big propaganda of the industry, to maybe one to a million. And what I had to hear. All kind of insults just because nobody wants to hear the facts even if they can be proven easily. People spend 40 years to make a bit of money and then fall for propaganda and do not even spend a few hours thinking of their investments. If I can change that for anybody, even with harsh words, I am OK.

Without a plan you will lose money investing, in ETF or single stocks, does not matter. I described earlier the Peter Lynch situation: 29% per year over 20 years and the holders lost money because of fear and greed, they sold low and bought high.

The average holy grail investor is satisfied with a positive return, even if compared to other strategies the return is very low. But that does not protect from behavior errors and those are the most expensive errors. We will see what happens when markets tank more than 40%, which is a realistic scenario. You need to have a plan or you are lost!

I was updating my dividend payout numbers earlier today and was just marveling at the steady flow of increasing dividends, come Venezuela, Greenland, Iran or whatever will be next.[]

This month will be a record dividend payout month for me. Even though I care more about the trailing twelve months average steadily rising, it’s still a beautiful number for me to look at.

While my dividend growth portfolio is up YTD, I would have hated to have to sell to live off the cash flow … which reminded me of your post earlier this week on how you manage cash flow if cash is needed: just raise margin debt! Indeed the smart approach to avoid selling when the market has its hiccups, especially if pursuing your approach of actually not living directly off dividends.[$]

Anyway, since I expressed my negative views on your communication style sometimes, I thought I should also give credit where credit is due: even though I can’t do it myself, see above (or maybe more below[$]), I admire your cash flow management.

Hope I’m not jinxing it … if I did, apologies, so long and thanks for all the fish. Let’s then all admire the next (and final) geopolitical event: the beautiful view of nuclear shrooms for the first and the last time. And good luck to everyone holding gold and Bitcoin – I’m sure their “hard” holdings will allow them to survive nuclear armageddon and live happily ever after …

$ I still couldn’t bring myself to taking on margin debt to live off, but I’m just wired differently. I believe the only times I took advantage of my margin account was when I knew that some big payment would come in on day T and I saw the opportunity to buy some dip on day T-2 (now T-1 for most US securities). Since the settling takes that day or two, I didn’t even have any margin debt, technically speaking.

The other reason, maybe the main reason as I think about it: if a tram hits me today, the dividends in our portfolio will still flow, all by themselves, and my family will be able to live off the cash flows produced by them.

I even instructed them on how to convert to CHF and transfer the cash to the Swiss bill paying accounts.

I wouldn’t know where to start to instruct them how to take on margin loans …

The final reason is probably the one that’s least important but that I’m most proud off: I learnt a lesson from a mistake someone else made! My main mentor in my dividend growth portfolio approach – right when I was getting started on shifting towards this strategy in February 2020 – got a margin call in March 2020 and was forced to inject “outside” cash into his IBKR account to avoid liquidation of some positions that he would have regretted liquidating. I learnt for myself that I never want that, that I – based on this lesson – could probably avoid ever getting burnt, but that this just was not the game that I wanted to play.

You will like this: said person did not technically get burnt/margin called on margin debt, but options sold that … well, went from OTM to deep ITM within a couple of weeks and for some of those options, expiry was creeping up …

You may anytime call me out for not having learnt the lesson that one should not sell Put options, but I still do, successfully. I’ll delete this post once I’m wiped out.

@Your_Full_Name I like your communication style, robs me a smile every time, that is almost art!

Now the margin part deserves some more digging. Almost everybody will tell you that it is a very bad idea. You can go bankrupt if you are not doing a strict money management (you remember, the most important part of every plan).

Debt is not per se a bad thing. All money is debt. Companies we own stock of have debt, at least most of them. Fortunately our liability is limited to the amount we did invest; in theory with broker margin debt you may lose more.

I manage debt different in my two strategies. The management of the dividend strategy I did describe before: I take on only debt in bear markets or when I need spending money. But since some time I take out the spending money from the gambling strategy as it is worth more than the dividend strategy now.

In the gambling strategy I have always debt, even started with debt. I calculate a margin multiplier of 150-300% depending on the difference of the actual portfolio value to the last high, I use the SP500 if the difference there is bigger. This difference I multiply with 3 and add it to the 150% up to a maximum of 300%. Then I multiply this number with the actual worth of my holdings and with the minimum of actual worth and entry price. That gives me two numbers. I try to keep the actual margin in between this two numbers. If it gets bigger than both I sell, if it gets lower than both I try to buy (I lower the requirements to buy a position). Sounds strange but works for me and my personal situation.

But of course this type of money management requires at least daily control. Lucky with some spreadsheet functions this is easy and you can even define alarms being sent to you. With 300% margin I would not even use half of my portfolio margin at IB which is 800%, so I am (almost) sure to not get a margin call. IB does no more margin calls, but you can define the sequence in which positions are closed.

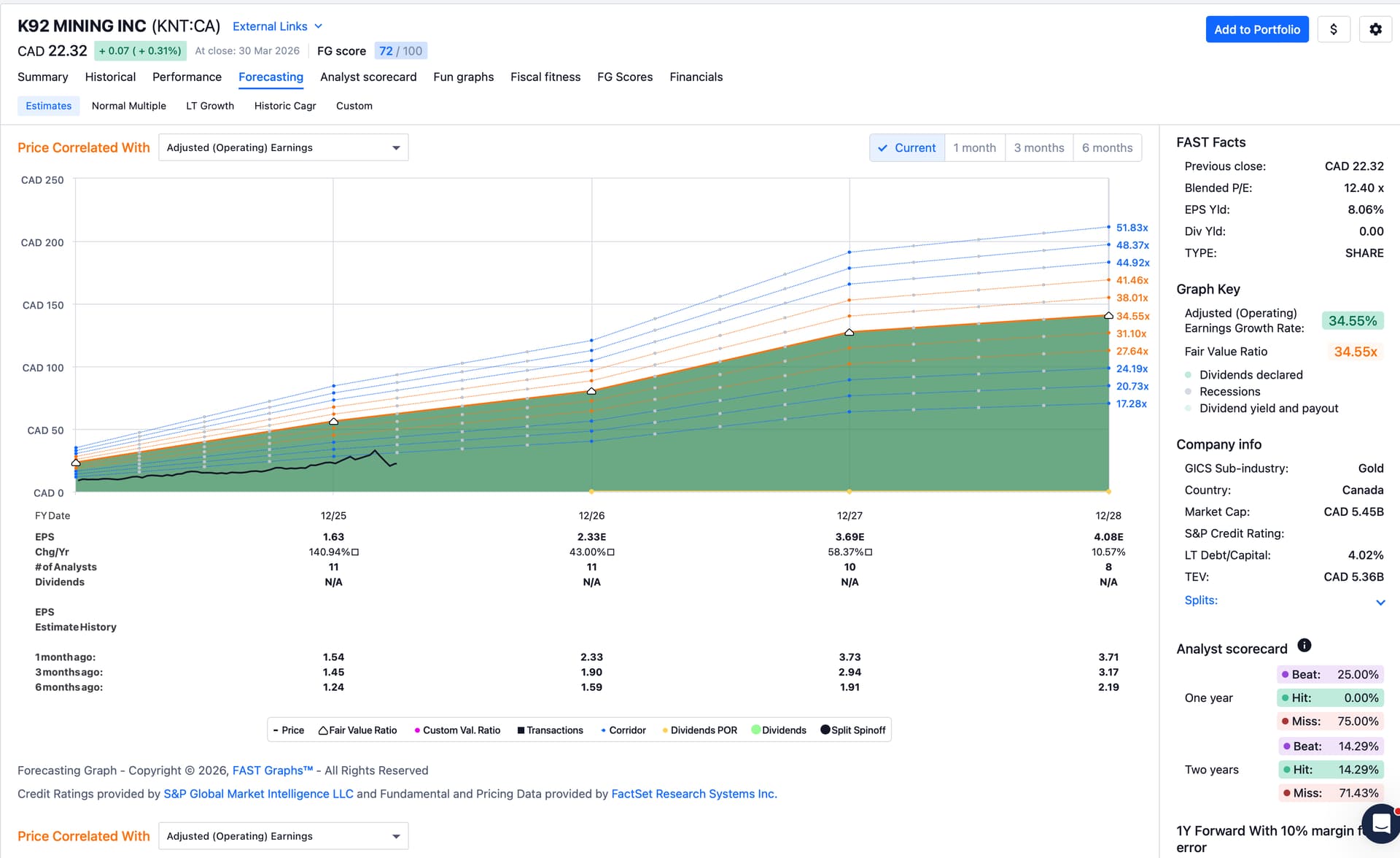

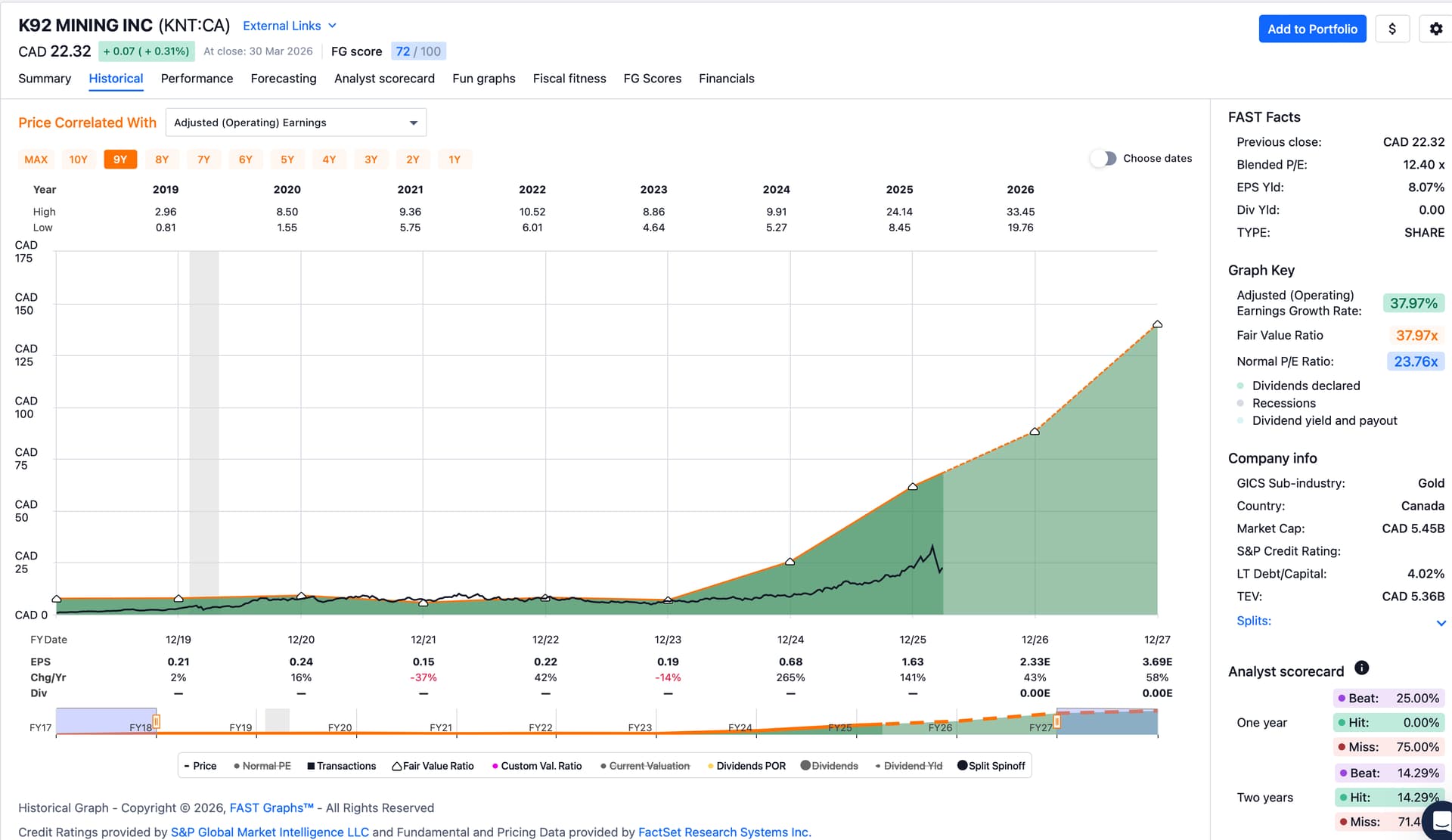

Came across K92 Mining today. Gold mine in Papua New Guinea. Before you all burst out in laughter:

Doesn’t fit my stock picks portfolio as it pays no divvies and operates not in my preferred countries. But the company seems high growth and easy to understand. I’ll research it bit more as a potential addition for my son’s growth portfolio.

They might suffer a bit more short term especially with energy prices elevated, but with the time horizon of my son’s portfolio this probably does not matter.

Sir, you are one day too early, 1. of April is tomorrow.

Canada is known to not control too much, no SEC, no Edgar, no trustworthy numbers. There are tons of such companies in Canada. If you do further research, you should have in mind that the numbers could be completely made up. Have seen it dozens of time, Canada is the Eldorado of stock scams. I think in the eighties I heard stuff like “hey, that looks like a Canadian gold mine” when talking about a cheater.

There are some methods to identify cheaters and for this type of investments I would use at least one of them. If the numbers are too good to be true they mostly are not true. Maybe this company is the great exception, but then why don’t they list in the USA like most Canadian companies?

I suppose you know a place to find the numbers. On first sight when I klick on financials on your link I only get a bunch of youtube videos, like they want to show that the mine really exists. But I’m sure you will find numbers somewhere, Fast Graphs apparently did.

But then thinking about your investment style probably you were really just one day too early…

I’ll dig a litte more and will also compare them against the miners Phil mentioned. I by the way picked them up from a Twitter post by a Swiss commodities investor:

You have to admit, though: at least they have a cool company name!

Edit:

FASTgraphs gets its data from FactSet. I have access to it at work and will also check Bloomberg, which is the … ahem, gold standard for financial data.

I remember the M-score, F-score and C-score to identify cheaters. Today I use my own methods which are mainly to identify “bought growth”. But that would not work if a company just makes up all its numbers in a country where you can do that without big consequences. Actually two such countries…

ICD-10 code K92 for Other diseases of digestive system is a medical classification as listed by WHO under the range - Diseases of the digestive system.

Add on: I usually check the holders. Many funds and I hope they are not all passive and have some analysts who like to travel. Still I see no reason why it is not listed in the U.S.

B (assuming you mean BCM Resources) doesn’t have any earnings data. It once cranked out a positive Operating Cash Flow (OCF) in 2009. Microcap of 48M CAD – if you trade a share you’ll move the price …

No forecasts available through FASTgraphs/FactSet.

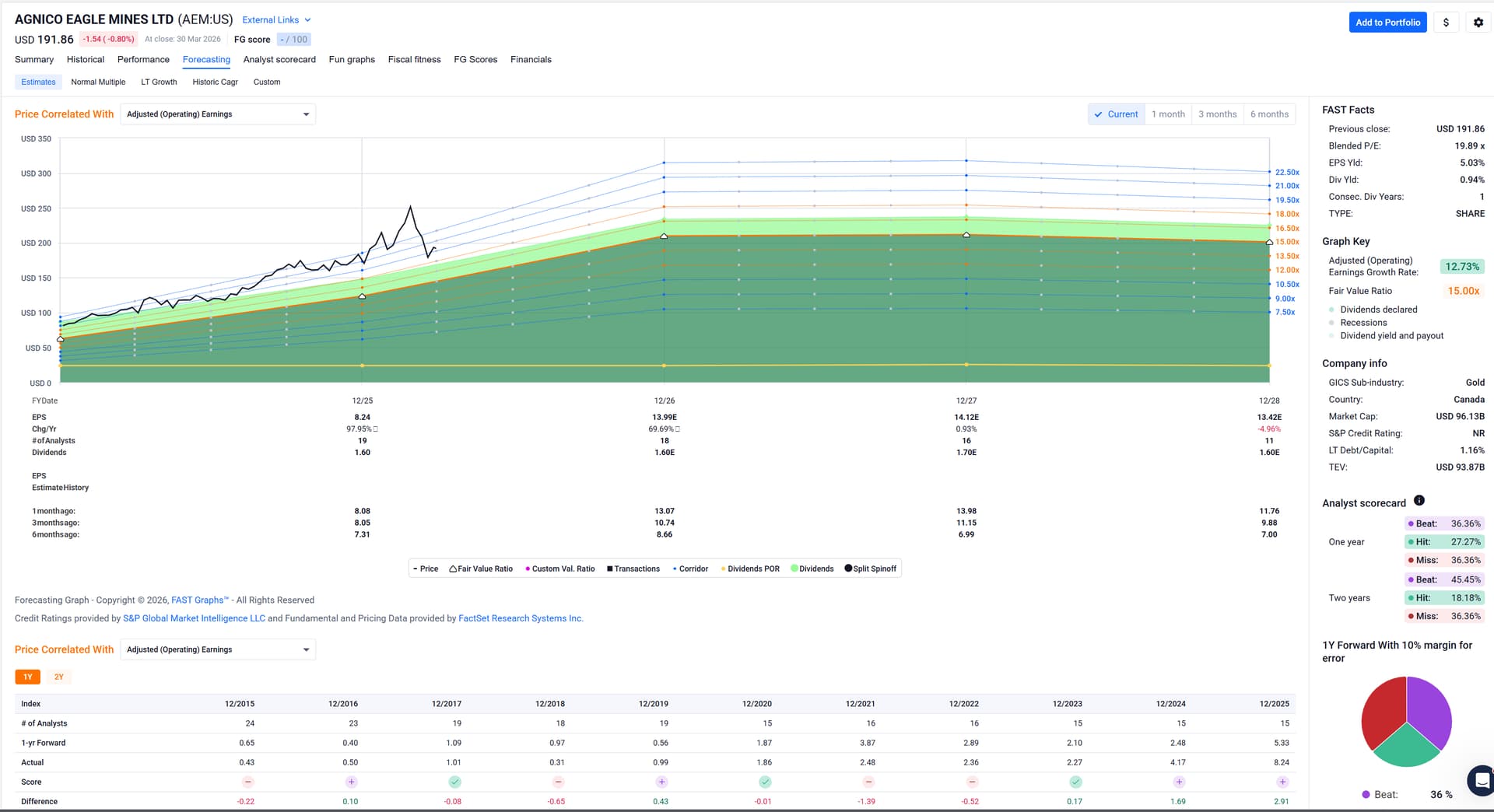

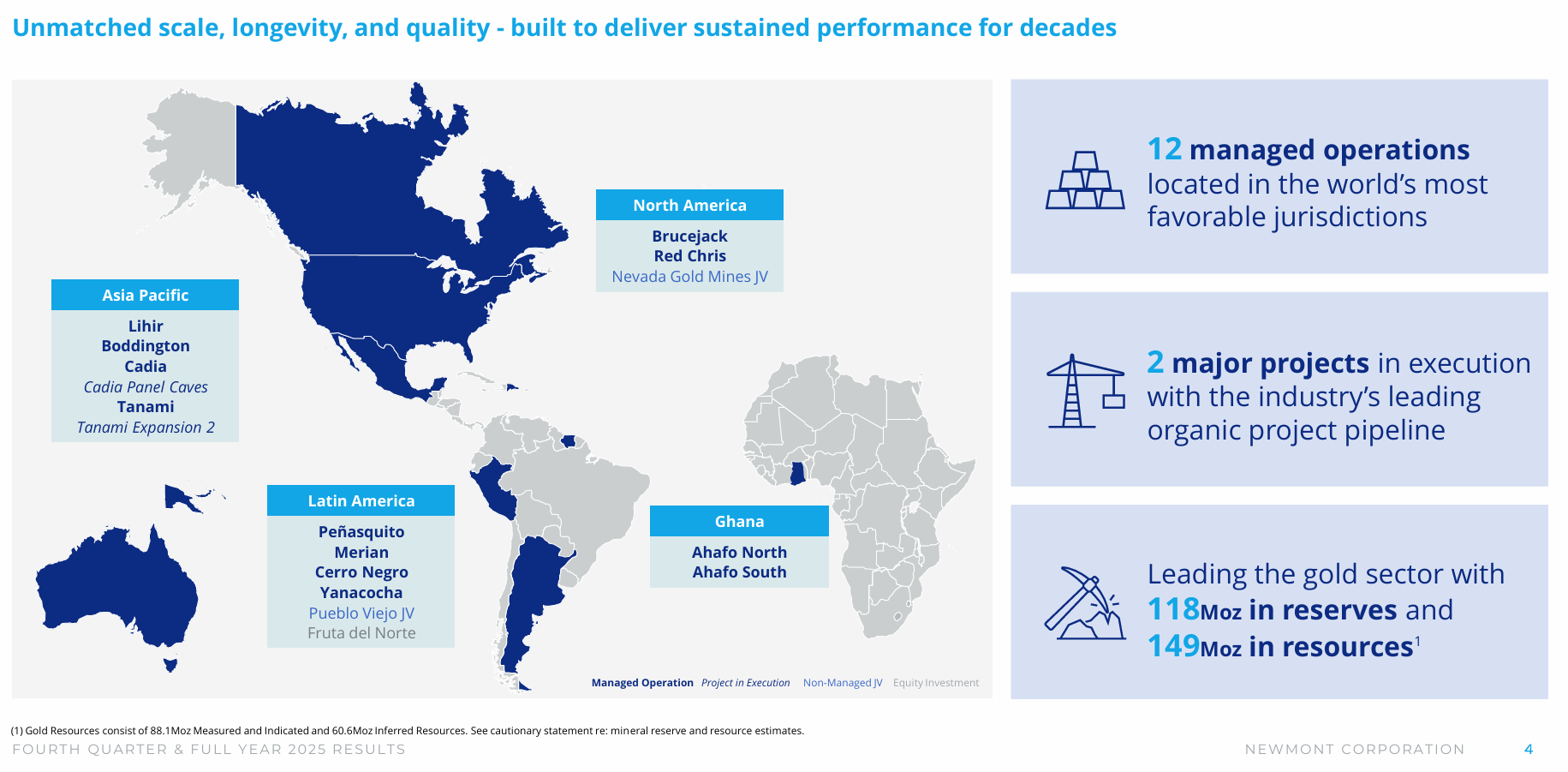

AEM. Established large cap miner, cranks out profits reliably, even pays a dividend. In forecasting it looks like they’ll have a hell of a year (profit wise), but will then flatten out.

Looks like they operate in Canada, Mexico and Finland. Slightly more stable countries than Papua New Guiney (but less cool sounding country names, IMO).

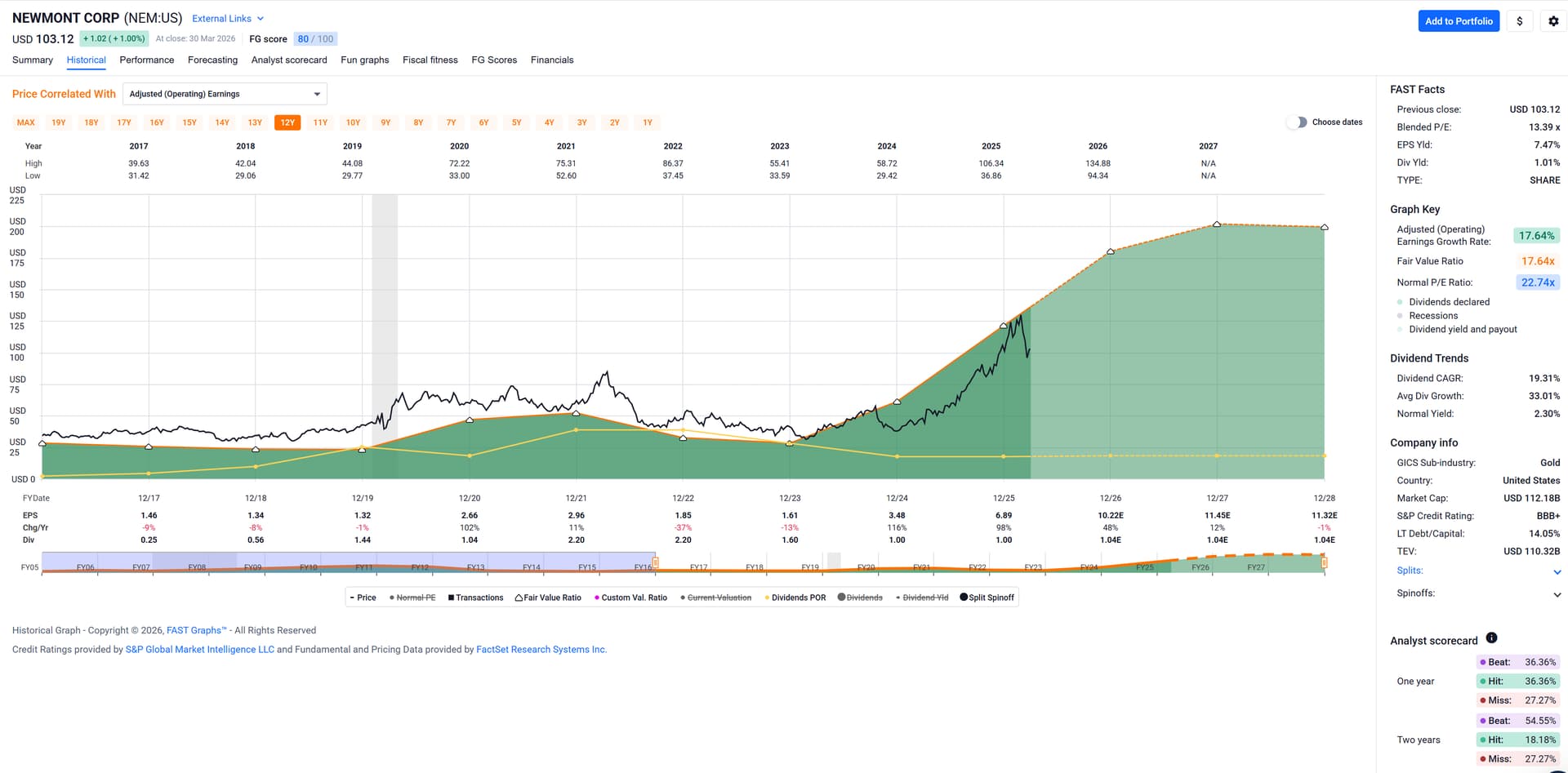

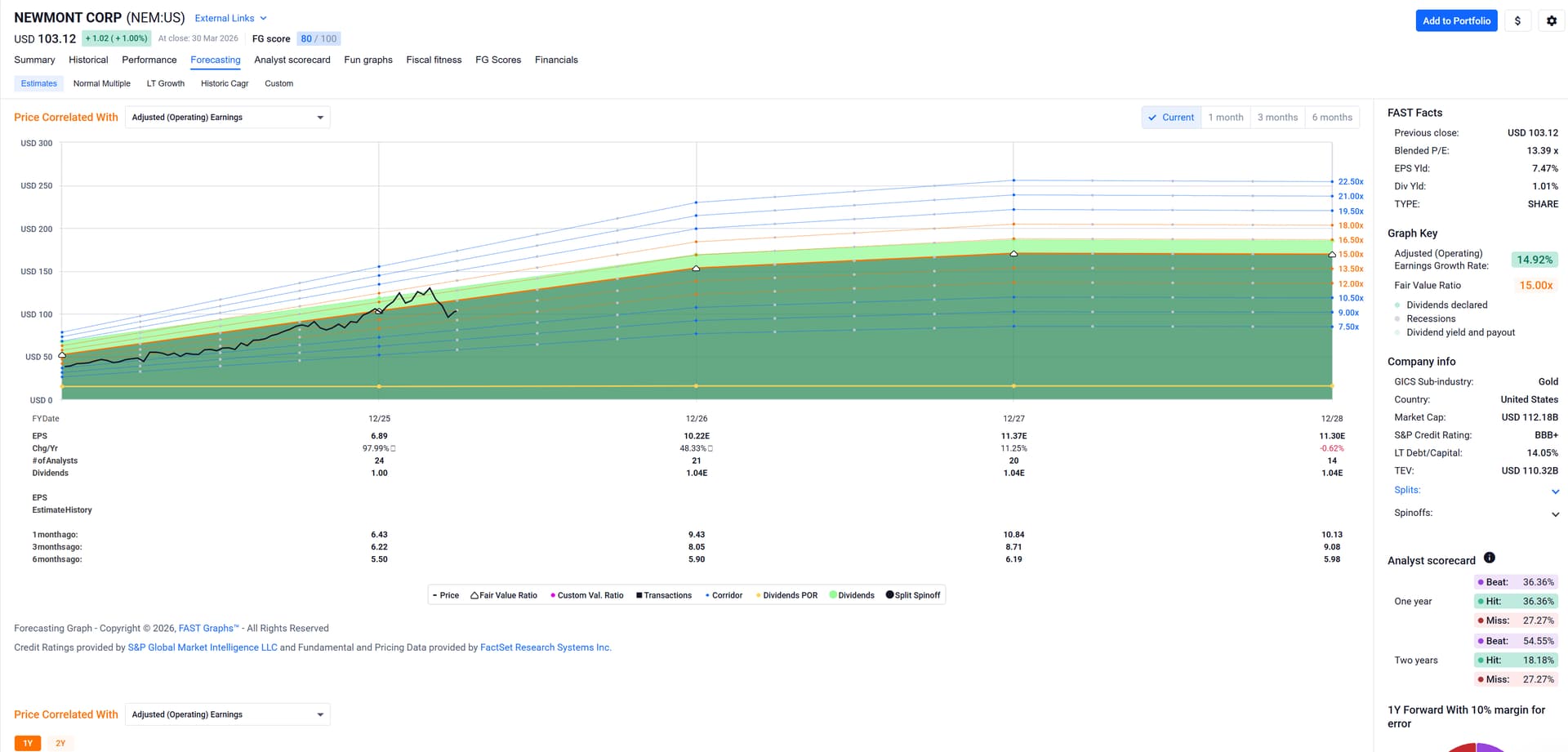

NEM. Established large cap miner. Profits are expected to explode as well and then perhaps also flatten somewhat.

Of the three, just looking at FASTgraphs and their investor presentations – where of course they appear as cute as possible – I like NEM best, but wouldn’t buy any of them, not for my son’s portfolio, let alone for mine. That K92 Mining (KNT) FASTgraph looks much more attractive to me (for a growth portfolio).

For my normal holdings (in my dividend growth portfolio) I check the analyst scorecard which gives some indication whether the earnings forcasts are reliable. They are not for any of these mining companies. NEM looks best but still somewhat shite.

For my normal holdings this would be a red flag, but I guess for a mining business it is very hard to give guidance to analysts. Analysts seemingly make their own estimates and seem to be wrong a lot.

I just scratched the surface with this, will dig a little deeper to see if there’s really any … ahem, gold, further down.

Gold kind of never looks attractive to me. It’s just not a productive asset and I suck at speculating.

Of course I recognize that by investing in gold miners, I’m basically on a derivative of gold, which is even more speculative …

That may be true, but the Papua New Guiney mudmen witch doctors will cure you from the disease within one Séance.

I’ll take a closer look at the reliability of the financial numbers (at least for KNT) later (hopefully tonight) when I have access to a Bloomberg terminal.

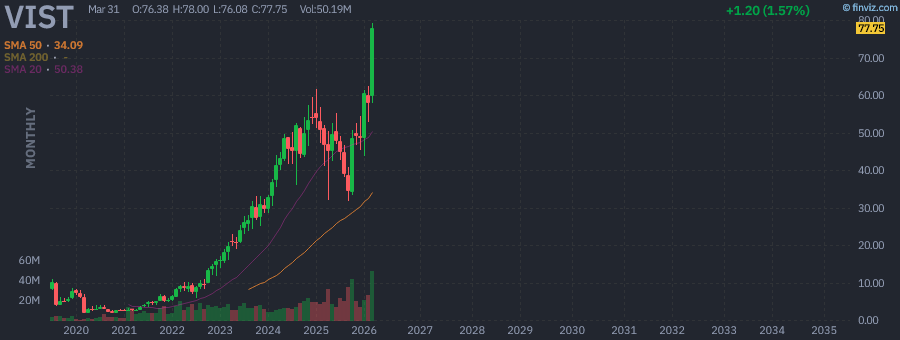

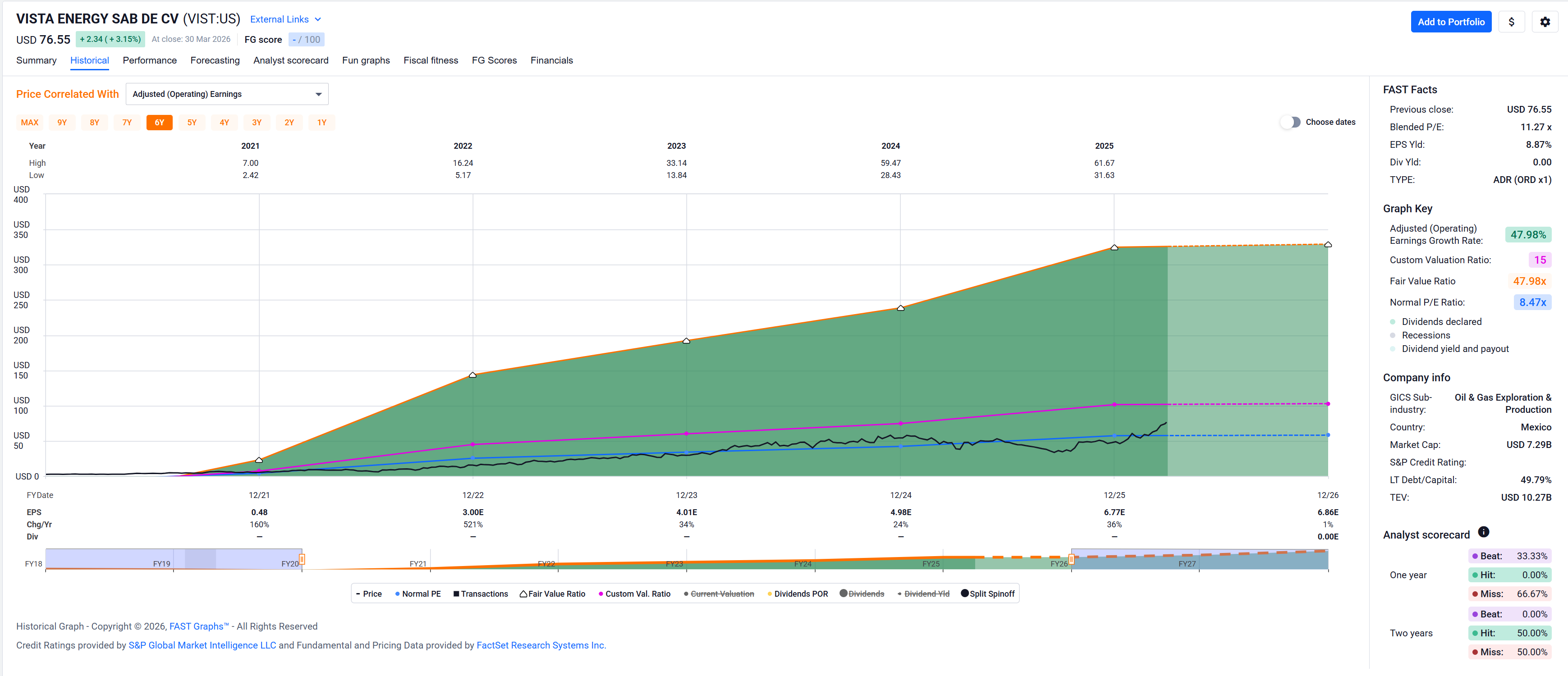

Today I sold a bit of Vista Oil & Gas for my gambling strategy. It crossed 1500% gain, is at 1572% at the moment. Nice, for every buck invested I get $16.72. Took out already many times more than I invested and the position is still worth much more than initially. It is the oldest stock in my gambling portfolio. I hope other of my oil stocks can follow its footsteps, but I doubt it.

In my gambling strategy I don’t look for dividends. But every stock there has to pay a yearly rent and a bonus when it reaches 500, 1000, 1500, 2000 and then 2600% of gain.

I still get some more trading to do today and will keep you updated. And it is the last trading day of the month and the quarter, if possible I give an update on both of my strategies after the market closes.

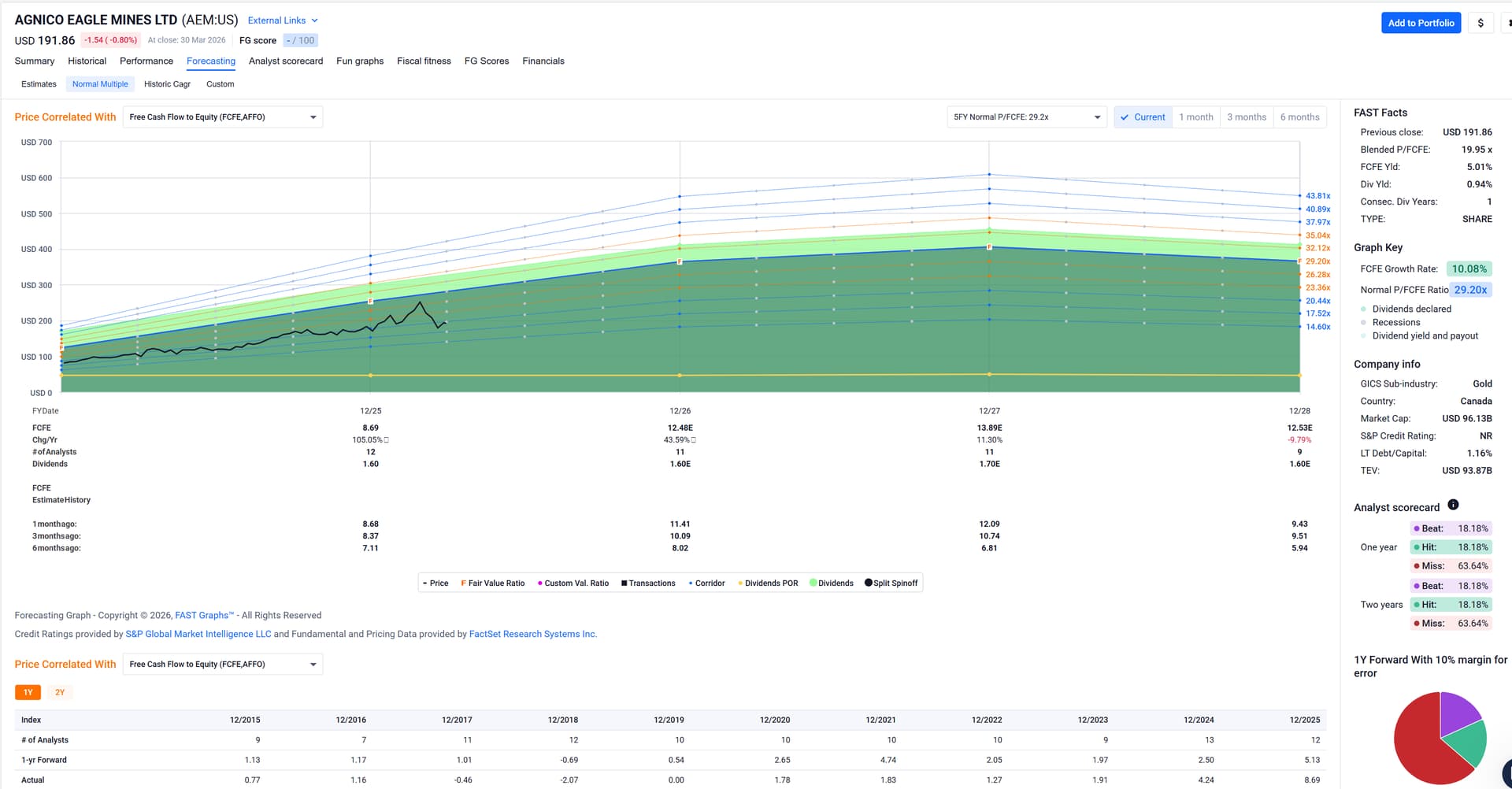

This sucker still[$] looks not really overvalued, but I would have taken some chips off the table as well.

$ I understand your momentum portfolio isn’t about valuation, really (I think), but even bringing my FASTgraphs hammer (pretty much the only tool in my toolkit) to the table, it seems still undervalued. The fair value (given its future growth) would IMO be 15 x P/E, which is respresented by the pink line. Price is still below that line …

I ignore earnings completely in all of my strategies, as it is probably the number that is most easy to manipulate. Often the planned retirement of the CFO has more influence on earnings than the real money the company made.

The second bad is probably book value, then a bit better either sales or cash flow. I think I did read a book on contrarian investment once where you should buy only if two of those four numbers looked good. If all 4 look good there may be a good reason it is that cheap.

In case of Vista it is probably cheap because of the geographical risk. Operations are in Mexico and Argentina, mainly in Argentina.

And the last trades this quarter, both for the gambling strategy. Sold TWI, the Titan wheels roll away. With a loss of almost one third, 32.87% after 8 months.

Then I made a strange buy: LyondellBasell (LYB), the chemical brother. This stock is usually a candidate for a dividend strategy, not a momentum and gambling one. However, it was thrown out of the U.S. Dividend 100 Index this month, I suppose because of the valuation. We’ll see what happens, I hope no chemical accident. However, you can lose only 100%.