LYB was on my screener for long time. It was very tempting as it approached 2020 lows, but I didn’t manage to buy before the big jump.

And a very nice quarter is over for me. This thread is not even a month old, feels like forever.

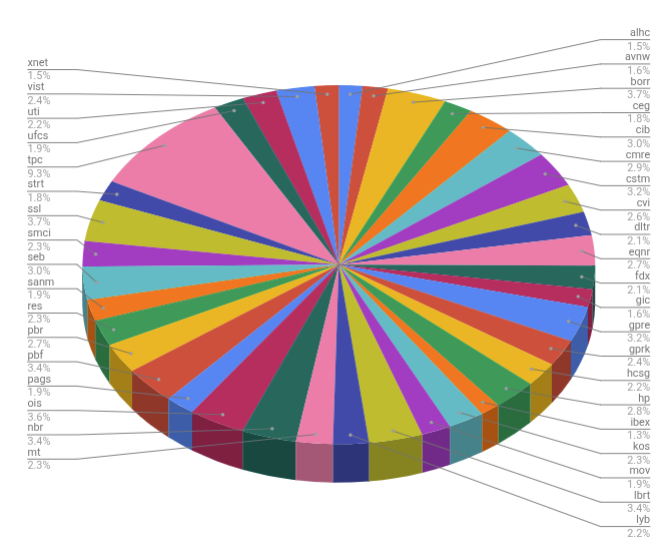

Here my report. I start with the gambling / momentum strategy:

Actual margin multiplier is 134.04%.

Very nice YTD performance of 25.23%. CAGR since 2020 (XIRR) is 29.81%

Table of positions:

And the “wheel of fortune”, position sizes:

Remarks: one of the best quarters ever while indices are in the red. Mainly because of oil.

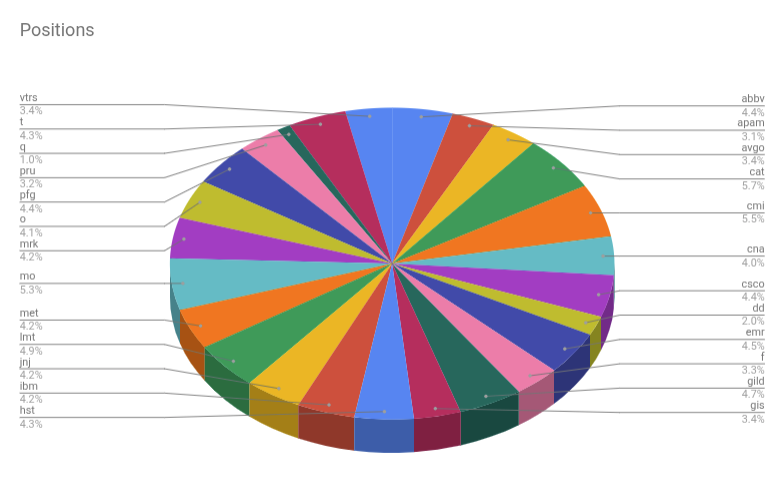

Now for the dividend strategy

Portfolio finviz link

Dividends: F, CMI, EMR, IBM, JNJ, MET, CNA, PRU, O, DD, Q, VTRS, LMT, PFG, GILD, AVGO

Sold ONL.

Bought additional shares of CNA, F, GIS (twice) and MET

Margin multiplier 100.2% (almost no debt).

Carry premium 3.01%

Performance YTD 3.6%, CAGR since 2014 11.02%, since 2020 13.79%

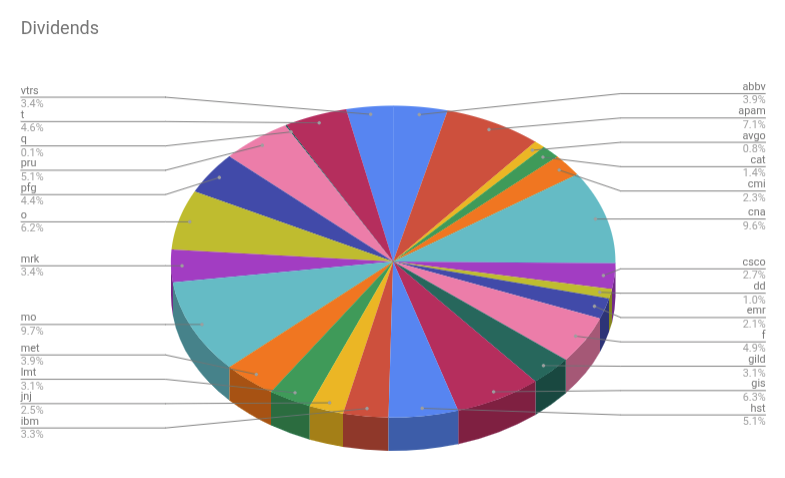

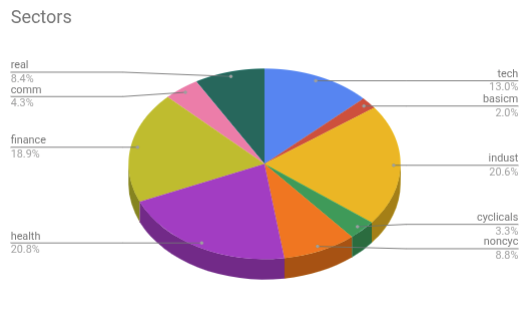

And the loved “wheels of fortune” of position size, dividends and sectors:

Remarks: back to 25 positions. Probably will need to buy an additional position soon, but as I have a 20% sector limit I cannot buy more health or industrials.

3 Likes

Yep. I call my mechanical system “the capt’n”. I wish the capt’n would have made me buy a bit earlier. But then it is a gambling/momentum strategy, so it is almost impossible to get a bottom.

Anyhow, bottoms or tops are pure luck. Fortunately picking tops or bottoms it is not needed to make money in the stock market. And Yippie, the gambling strategy performance is at Peter Lynch level. But he did it over 20 years and I am only at 6 years and 3 months.

Snap! I bought GIS today.

1 Like

No noise, all discussion about stocks are welcome.

Strange. It is true that the Toronto exchange does not enforce GAAP rules, but the requirements for annual and quarterly reports are there in theory. The audit requirements are less strong too.

But there is no EDGAR, no SEC page where you can check them numbers out. I would never rely on yahoo finance (where I found some numbers) they often switch Canadian for U.S. Dollars. ![]()

2 Likes

Was afraid, but the cash flow looked all right for the 3rd quarter. It is therefore still on buy with me.

Looking at the charts (day/week/month) it looks like chief falling knife may have found bottom. Hopefully it did finally digest the dog food from blue buffalo.

2 Likes

I have bought today some short term puts on carriers such as HAFN, FRO, STNG. Let’s see if I get assigned. This is still my desperate attempt to get away from the US (even if these companies are listed in the US). Besides this I bought some more VT as I wanted to pay back my JPY that I got on margin but realized that JPY still looses to CHF every day and it’s not smart to pay it back and hence did want to invest it in something.

@cubanpete I liked your mindset of not having cash left on the broker.

Unfortunately, I got kicked out of ESLT with my trailing stop after 100% gains, to bad

I think you meant “sold puts” not “bought”.

Not my style, I explain: long options give you the possibility to make a lot of money but not often. Most of the times you lose. Now short options make you very little money a lot of times, but one missed big move and you would make even more. You may still win but over time you win less than if you would just hold the underlying instruments. On top of that you have liquidity issues and a gigantic spread.

Now an ETF with 10’000 components that is not even diversified is another story. I better shut up about it because I am like 1:1 million, it seems to be like a question of religion. I can’t help but being a contrarian. I can just repeat: you have the non-diversified risk on all that high flyers of the past and you invest only cents in stocks that may make thousands of %… you get a few dollars out of it and that is it. But you carry all the garbage that a few filters would throw out.

Stops may be good if you don’t have a strict plan or don’t have the discipline needed to execute a plan. But they carry the risk of being fished. And remember, you pay performance in the currency of volatility.

Please, don’t be offended by my style, English is not my mother language. And please keep posting, it is always interesting to see other perspectives.

@cubanpete Como podria ser ofendido de vos? Tranquilo disfruto cada uno de tus posts ![]()

You are actually right on all your inputs, I meant sold puts. I do that mainly for stocks that I do not fully believe in (I know that sounds stupid). With regards to VT that is also y compromise, I have VT, VWRL, VWO and EIMI as my core values representing around 60% of my portfolio and individual stocks make up for the rest of my portfolio. On top of that I have 1 BTC as reminder to listen more to people that are smarter than me (had a very good friend recommending me going full into crypto like 20 years ago and I did not listen to him and only bought this 1 BTC and 5 ETH).

I think that the smart approach would have been to learn first everything that there is to lern and then apply my strategy. However, the impulsive nature that I am (that’s the Latin part ![]() ) I could not wait and just jumped in the game and learning on the way ever since.

) I could not wait and just jumped in the game and learning on the way ever since.

This is also the reason why I enjoy to read you and @Your_Full_Name so much because I feel that from every post I get some more good inputs to build my own defined strategy.

2 Likes

Do you still own SMCI?

They are calling it uninvestable, thats normally a trigger to look at investing!

1 Like

Exactly. The day that it was published it rallied.

Happens all the times and often with SMCI. A few years ago Sequoia Capital published a very bearish article to get some cheap. Unfortunately they slipped into the mandatory declaration position size and had to declare that they bought a lot at the same time their article was published. They made 9 figures on that trade, still enough sheep around that belief analysts bullshit.

Most of those comments are just copies of copies, analysts may be wrong but they may not be the only ones being wrong. But sometimes it is a very egoistic “do what I say, not what I do” thing. The only action one can take is just ignore it. I have to ignore it anyhow because I use mechanical strategies, so I am immune of any comments.

SMCI was my first investment that crossed 2000% gain and I took out a lot more than I ever did put in. Since then it was quite a sad play, but I just do what my capt’n tells me and charge the yearly rent (by selling some).

I expect the fines to be brutal, but the real risk is whether Nvidia/AMD will cut supplies to SMCI to manage their own risks which would be a death sentence for SMCI.

Not sure what will happen to SMCI, they have a scapegoat, a very high one. That may be enough.

- I think the risk is priced in.

- Nobody knows the future and when you make that much money with a stock it is normal to do the same the owners do: take out some chips from the table. I do that with the 500% rule.

Nice performance! ![]()

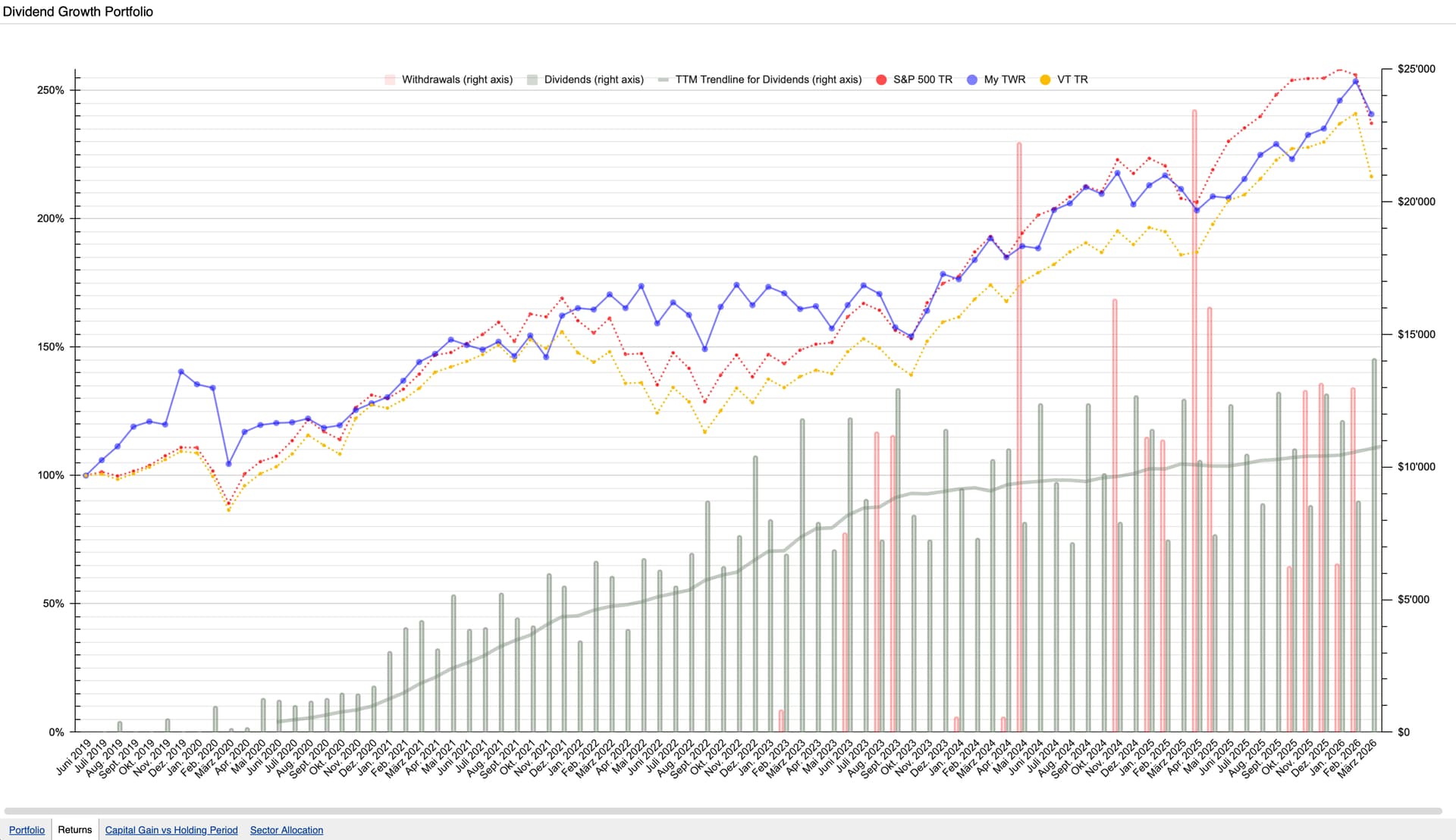

My (dividend) strategy is always mostly up to date and linked at the previous post Simply stock trading - #11 by Phil_MCR. [$]

I’m at a paltry 2.4% TWR YTD.

No margin.

Dividends in March: ~$14k

March trades:

- increased OMC

- increased CHCT

- increased SJM

- increased KDP

- increased MAIN (via automated DRIP)

I now also provide some actual $ numbers on the published spreadsheet. Hope you enjoy.

$ The Returns tab usually has a lag time of a couple of days until I have updated all dividends that sailed in. And a couple of days of delay until the final Total Return (TR) numbers for the S&P 500 and the VT become available.

1 Like

Nice, I have a practical (for you) question, out of pure curiosity: given most US companies pay 4 times per year, and I imagine it to be in the “regular” quarters (Mar, Jun, Sep, Dec), how do you manage cashflow?

I may be wrong about everything, and quarterly not being in the “regular” quarters, but I can’t imagine you selecting companies based on when they pay a dividend as that’d be introducing a variable that doesn’t make good economic sense.

Edit: of course it’s absolutely none of my business how you manage cashflow, it’s just curiosity, but perhaps a broader question is how would a dividend growth investor who depends on dividends to fund their life manage cashflow considering the timing of dividend payments. A decent European blog, aptly named EuropeanDividendGrowthInvestor, had at some point suggested ETFs based on the when they pay dividends but I consider this idea a bit suspect, but may be driven by practical considerations. (Also imagine the field day the dividend irrelevance crowd would have if they caught wind of “people making investment decisions based on covering calendar months”)

Also didn’t extend the question to Pete the Cuban Swiss as I imagine he manages with margin.

1 Like

Dividend payouts do spread out over all months. The ones you mention are the months with the highest payouts; February, May, August and November have the lowest payouts.

You can see the actual payouts on the Returns tab in my published spreadsheet. It currently looks like this:

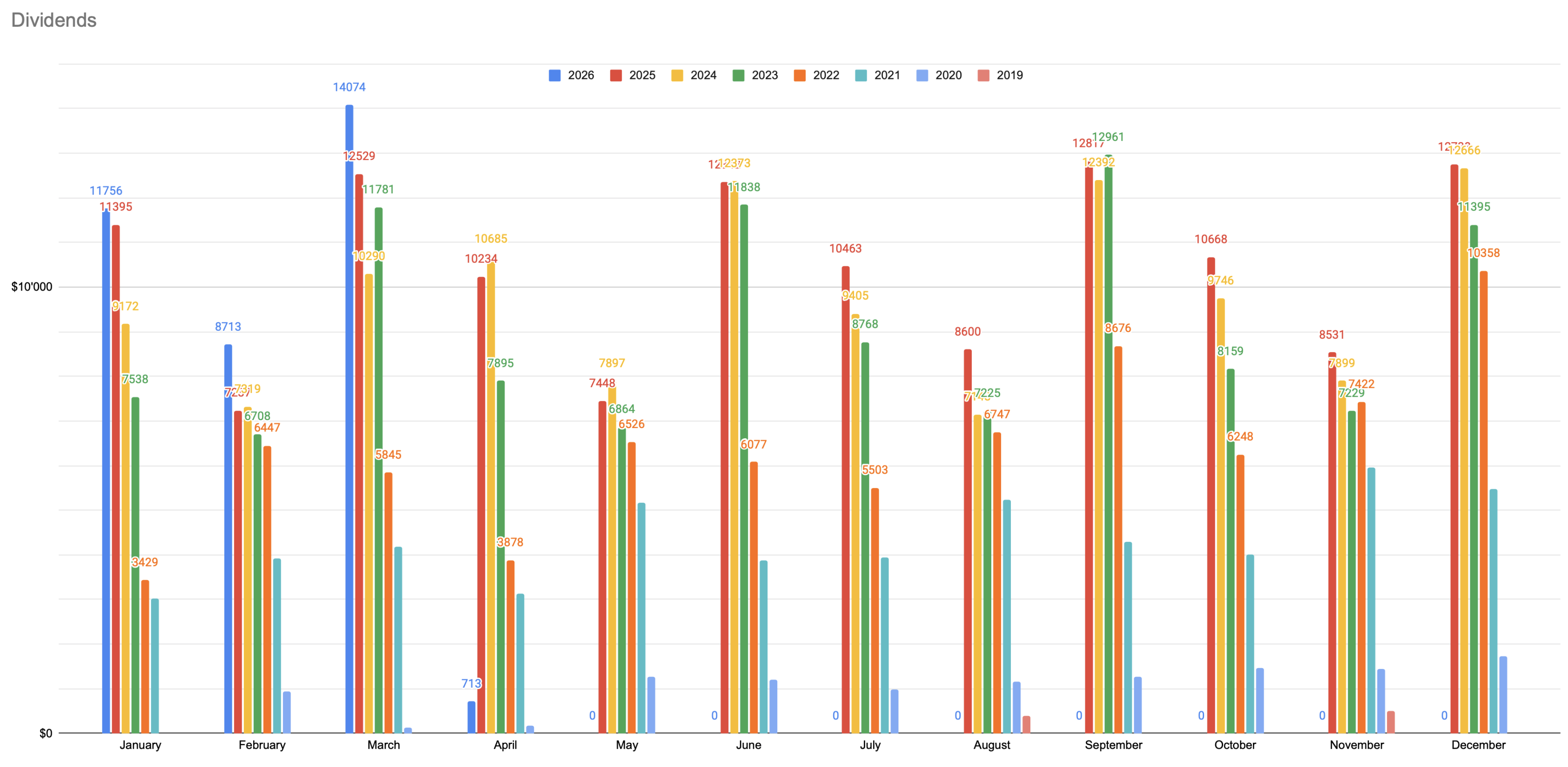

The following chart isn’t on my published spreadsheet as it’s somewhat redundant with the above, but it gives you perhaps a better view of the ebbs and flows of dividends over the course of a year.

I stopped paying into the portfolio in 2022 and started withdrawing in 2023, so the dividend payout numbers from 2023 on are probably best representative for how the divvies grow by themselves (versus thanks to new positions funded by cash injection into the portfolio).

You’re right, I don’t select the companies on what month they pay out. And companies anyway sometimes change their payout schedule.

It’s a good question, especially if you’re a global dividend growth investor.

It’s certainly easier to manage if you mainly invest in US companies (Canadian and UK work, too) as they focus much more on shareholder return. Cash is paid out at least quarterly (or even monthly, for some REITs) while e.g. Swiss (or probably most European) companies pay out only once a year, typically in Spring.

To be honest, I don’t really have an answer if you’re not US (CA, UK) focused. I suppose the simplest answer is just to have a larger cash pile that you can withdraw from in those months/quarters where you typically don’t receive divvies from your global stocks, but it seems not very efficient as that cash is kinda “dead” most of the time.

Outside my stock picked portfolio I hold some ETFs. Some smoothen the payout schedule with monthly payouts (e.g. VDET or MTBA), some are even more uneven in their payouts (e.g. VXUS).

I plan to reduce the “money like” instruments like VDET and MTBA over time. For now they give me the comfort of new cash very reliably arriving in my account which just helps with sleeping better at night.

2 Likes

For me the answer is quite simple: remove the “depends”. I once said to myself: “no need to be the richest man in the graveyard”, so I just take out money whenever I need it. I don’t even have a budget, I know, that is a bad idea, but what for? I am not in the habit of spending much money, don’t have to pay rent and whatever has to be done at my house or vacation home has to be done anyhow, budget or not.

For additional cash flow I could use the “market dividend” (what I call selling down to 5% whenever a position reaches 6% of my portfolio value). But I don’t, I just use credit and let it pay back by sells and dividends. In other words: for me only the total performance counts.

Anyhow, the dividend strategies total net performance (Dividends + capital gains - tax - debt interest) measured as money weighted rate of return (CAGR, XIRR) is 13.87% since 2020 and I am not able to spend that much.

I use dividend stocks mainly to reduce risk and that seems to work.

2 Likes

I wouldn’t be opposed.

![]()

(although it is not my goal, either)

I typically go through my stock picked portfolio about once a week (with FASTgraphs) to see whether there’s any new buy or sell changes.

I thought maybe I’ll provide a deeper dive on one company whenever I find the time. Perhaps others will find it useful or can point out flaws in my reasoning.

I usually go through the portfolio alphabetically and the first company on the list is AbbVie.

ABBV

AbbVie, Inc. is a research-based biopharmaceutical company, which engages in the development and sale of pharmaceutical products. For company profile details see footnote.[1]

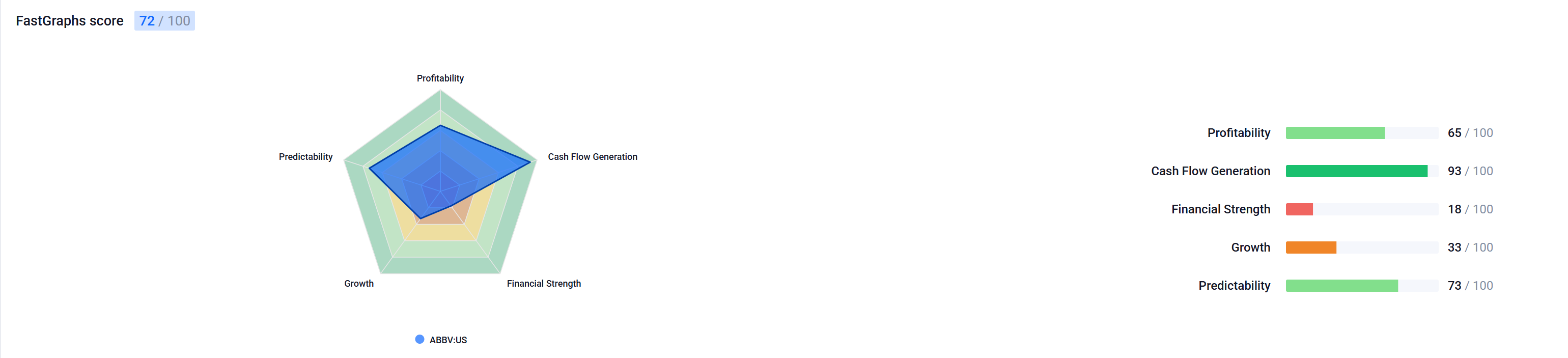

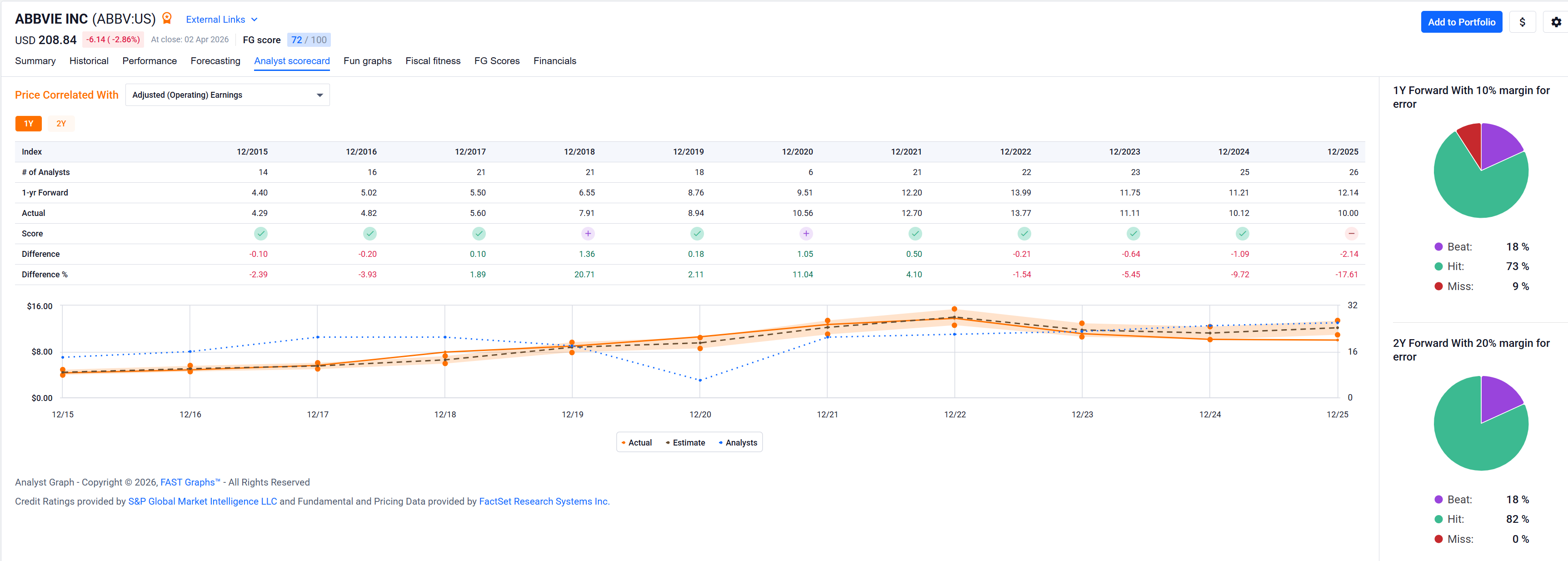

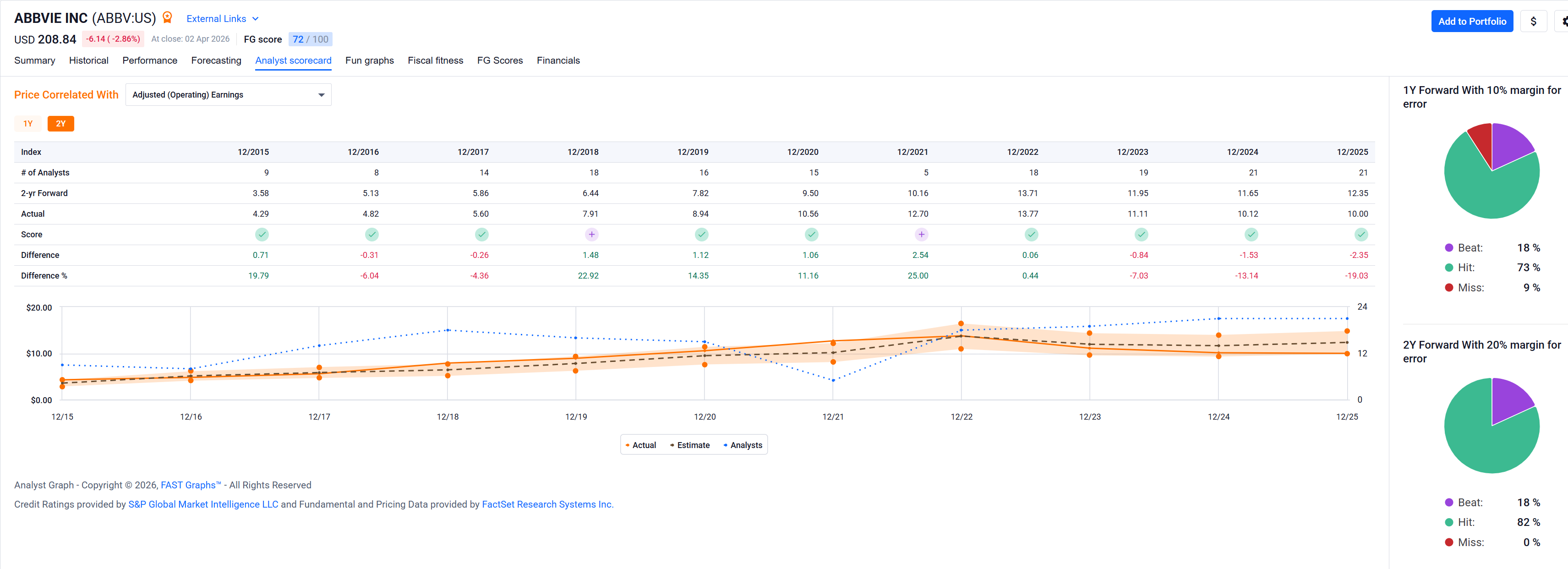

The FASTgraphs summary score (which was only introduced recently) looks like this:

The historical earnings graph, price chart, etc:

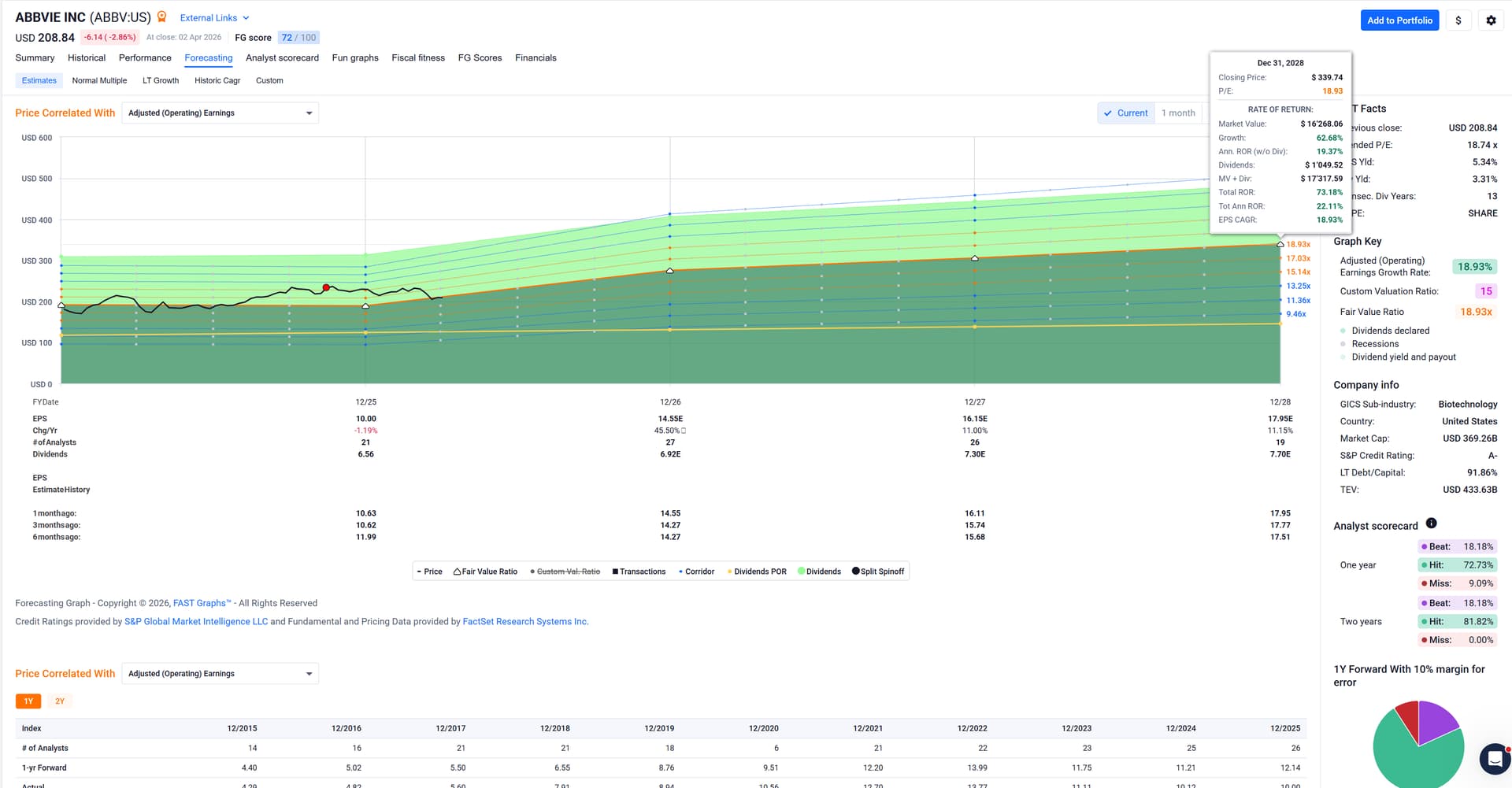

Going forward the patent expiry of the blockbuster drug Humira seems to no longer impact their earnings and analysts expect[2] them to grow again at a nice clip.

I like their dividend growth rate – 11.34% CAGR over the past 14 years – and the fact that their payout ratio is less than 50% (for expected 2026 earnings).

Forward looking earnings chart:

Company’s not cheap given its expected growth rate of about 19%, but seemingly just about fairly valued. I like that earnings growth expectations are steady when looking at analyst estimates for 2026, 2027 and 2028 from 1 month ago, 3 months ago and 6 months ago (even pointing upwards slightly).

If the company stays at its current valuation (18.74 x P/E) until December 2028 we’re looking at a 22% total annual rate of return (ROR). If the PE drops to 15, we’ll still see a 13% annual ROR.

Unless things look iffy, this is roughly where I stop and move to the next company. If things look iffy, I’ll dig deeper.

Things don’t look iffy to me. ABBV is a hold in my book.

1 Company profile:

Company description:

AbbVie, Inc. is a research-based biopharmaceutical company, which engages in the development and sale of pharmaceutical products. It focuses on treating conditions such as chronic autoimmune diseases in rheumatology, gastroenterology, and dermatology, oncology, including blood cancers, virology, hepatitis C virus (HCV) and human immunodeficiency virus (HIV), neurological disorders, such as Parkinson’s, metabolic, comprising thyroid disease and complications associated with cystic fibrosis, pain associated with endometriosis, and other serious health conditions. The company was founded on October 19, 2011 and is headquartered in North Chicago, IL.

GICS Information:

Health Care>Pharmaceuticals Biotechnology & Life Sciences>Biotechnology>Biotechnology

Company website:

2 The analyst scorecard looks great. Either the analysts are great at estimating the company’s future earnings or the company provides accurate guidance. Or likely both. ![]()

One year forward guidance:

Two year forward guidance:

3 Likes

I hold ABBV since quite some time. It is still on buy, but the position is more than 4% and the health sector is more than 20% of my divi portfolio so I don’t buy more at the moment. Last buy was 31jan2025. (Sorry for my strange way of writing dates, I think we did that when I was working for an international air transport company.)

I mainly check cash flow for my divi stocks. FCF payout ratio as Goofy said is way under 50% so the dividend is safe. Debt is manageable (OCF/Debt 0.28) and they work effective and are not overvalued by looking at enterprise value divided by free cash flow (EV/FCF 24.27). I think I described all my formulas used in my methods before.

I ignore earnings, prefer cash flow for my formulas. Earnings sometimes can be manipulated and one would need to go back many years to check for bookkeeping entries that affect earnings for years later. Unfortunately it does not help to compare earnings to other companies of the same sector; the CFO of one company may plan his/her retirement and therefor use some of the many legal tricks to change earnings.

Don’t remember who said it, but “Earning reports are lies that contain just as much truth to be still legal”. I think it was Ben Graham, but I’m not sure. Could be Buffet too.

1 Like