For some reason I – with my “basic” FASTgraphs subscription – got access to one of the previously premium features of FASTgraphs, the “Fiscal Fitness” tab. I expect this to vanish any day. Anyway, while we are at it, here’s the quarterly display of FCF vs the Dividend for ABBV.

Seems like a safe bet for now regarding dividends. AKA the dividend seems safe.

This statement surprised me, but you probably know more about it. Debt is actually a little bit more of a question mark for me for ABBV, but I honestly don’t unterstand debt in healthcare well enough to make any reasonable guessings. I’d have to research a bit more. Or maybe @Refugee can chime in.

Seems like I’m too lazy to do any of this before the Easter Holidays end.

The harsher version I believe is Munger saying that EBITDA is “bullshit earnings” IIRC.

At any rate, ABBV does not seem to be affected from any of this, I believe. We’ll see about any of those famous last words …

About debt: I am probably the most lazy person in the world for analyzing debt or any other fundamentals. So a bit more than a decade ago I did define simple rules, formulas.

Over long term a company that does not go out of business will produce money, even if you have to suffer a lot in between (like with chief falling knife General Mills). But all companies go out of business sometimes, life (really, “f”) is hard. I think even the century old Japanese temple building company did go out of business. As a rule of thumb one of my favorite authors did say for a big enough majority of things: that everything existing today will exist more or less the same time in the future that it did exist in the past.

So the point is to hold them business’es as long as they don’t have the odds against them to go out of business. The rest is just suffering the losses and enjoying the gains.

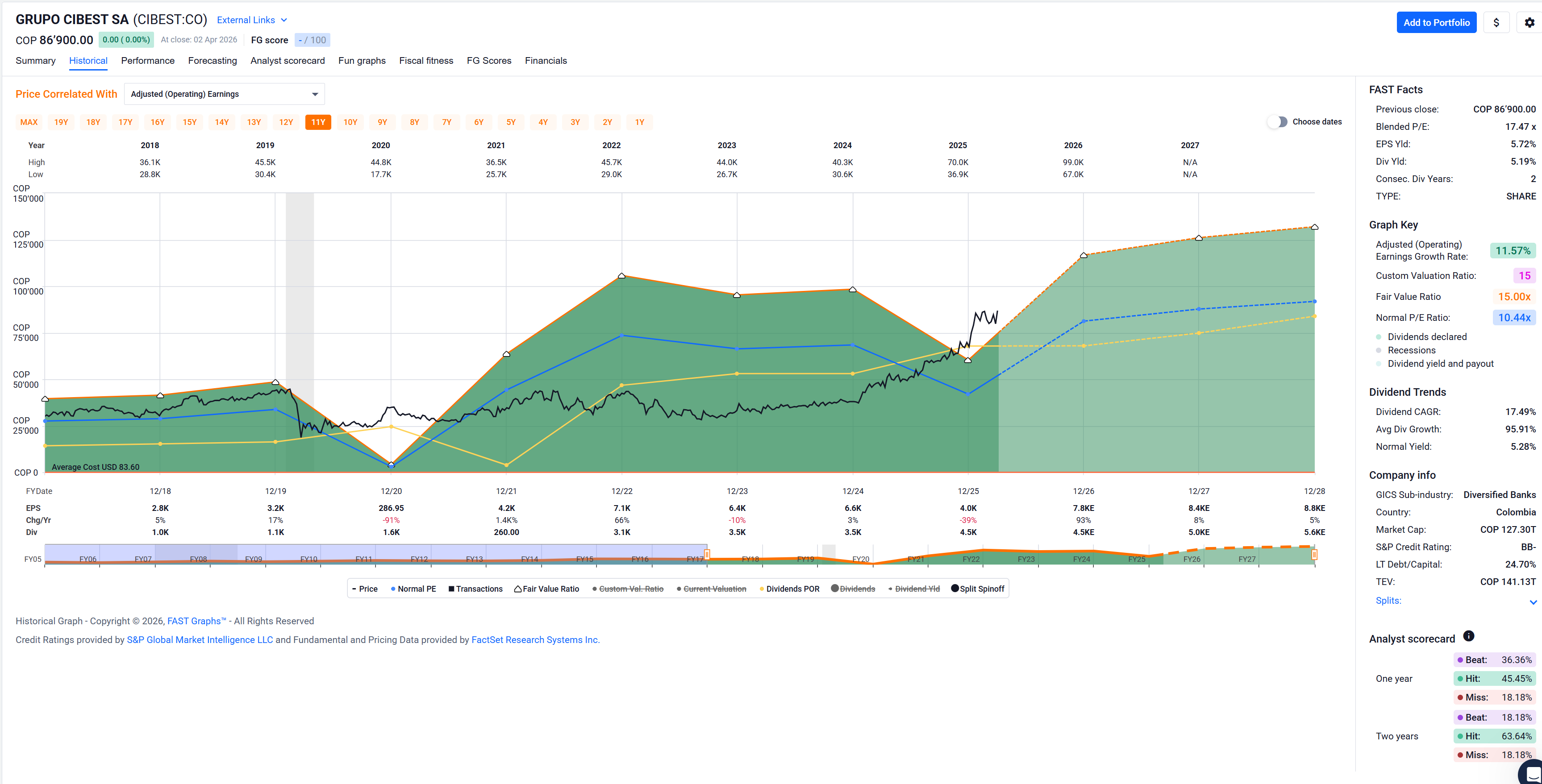

Wow, the Columbian bank Cibest group is in my gambling portfolio already one year. So they must pay rent, sold some at gain of 83.7% after one year. Bienvenidos al segundo año!

I did not, my capt’n did (mechanical stock picking). Stock picking however is the least important of a strategy, more important are money management and position management. “Charging the rent” is part of the position management…

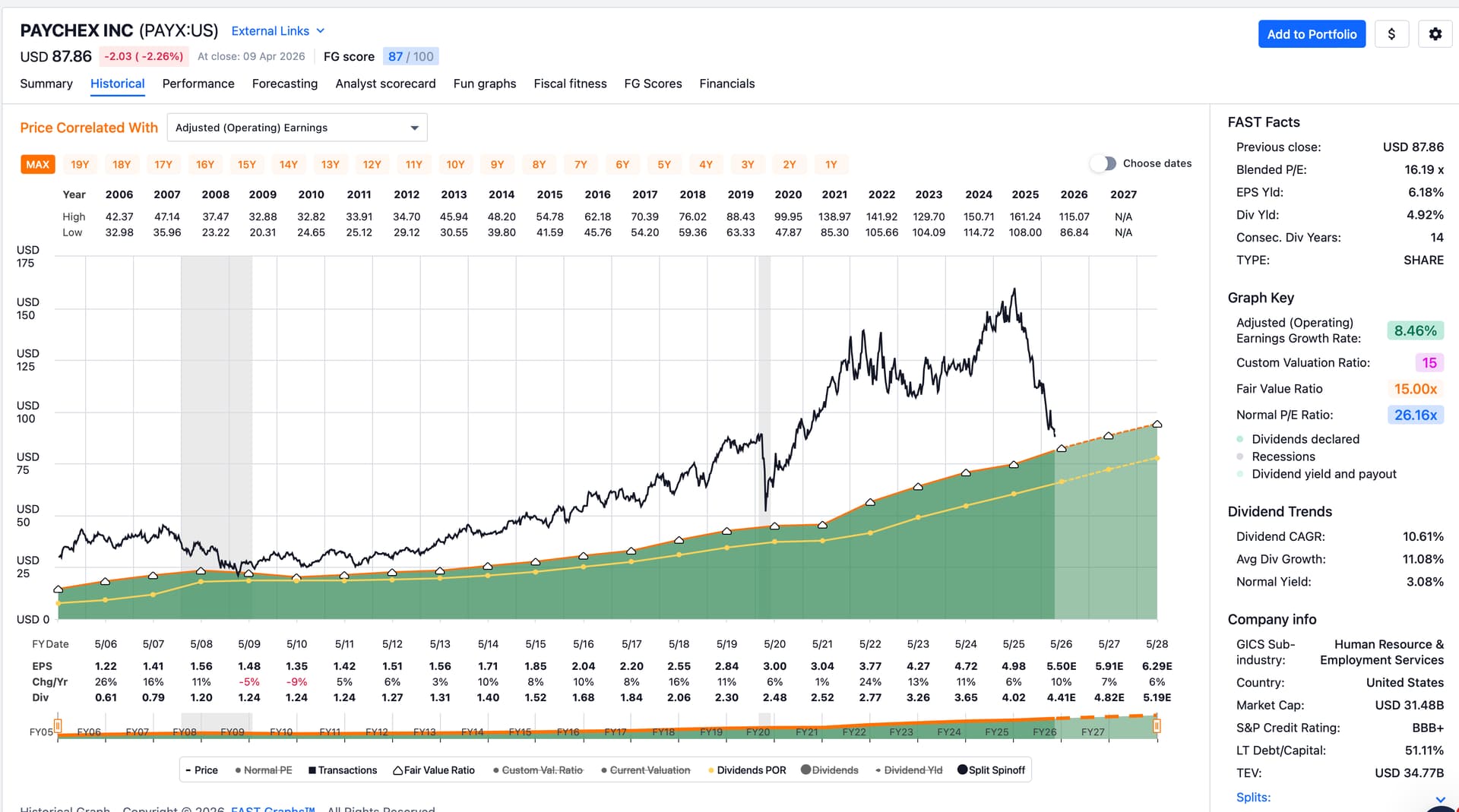

Interesting. While not a fit for my dividend growth portfolio, it looks cyclical but actually mostly nice earnings wise. According to FASTgraphs it might still have some gas left in the tank, too:

Also, on a macro level, they’ll benefit from Venezuela’s drug business decline and Maduro now out. Surely they’ll fill that gap in the drug cartel business …

I don’t do macro, I’m just snarkily making wild guesses about their business model. Please forgive me.

Great, good companies for dividend holding, fulfill all my cash flow criteria. I hold a few insurers too in my dividend portfolio.

I don’t touch metals except for some jewelry for my wife. Not even sure that gold is a rare metal. Ah, and I have a gold tooth since 45 years, like new!

After the close yesterday, Alignment Healthcare did present good numbers. After market it did rise more than 10% which gives me a capital gain of 156.6% according to Interactive Brokers (I suppose google finance does not include overnight movements) since January 2024 when I bought it for my gambling portfolio.

BTW: I sometimes get comments about only presenting gains, not losses. That is not true, but I cut losses fast and write about it. Winning stocks can stay with me forever. My motto: hold as long as possible, but not longer.

To follow up on that, maybe you want to read the 3 articles I wrote about the why, how and an example of a completely mechanical strategy that a computer could trade for me:

Of course the money- and position management are different for a gambling strategy compared to a dividend strategy. The completely mechanical stock picking is different too of course.

I don’t want to publish the details of the stock picking mechanics of my gambling strategy. There are thousands of parameters, technical and fundamental, that can be combined in any way, resulting in more possibilities for stock picking than atoms in the universe. But as I said, stock picking is not that important. I don’t want to publish my method because I have to trade illiquid micro caps sometimes and then I want to be alone, I hope you understand. But I publish the trades usually shortly after I get a fill.

Well, Peter Lynch probably would protest, but I think money and position management is more important than stock picking. Because many of my picks are simply losers. One has to lift many stones to find a diamond, but there are diamonds. With the correct money and position management you can make money, even if you pick a lot of losers. With bad money management you will lose money even if you pick the best stocks. That is why I think stock picking is the least important part of any strategy.

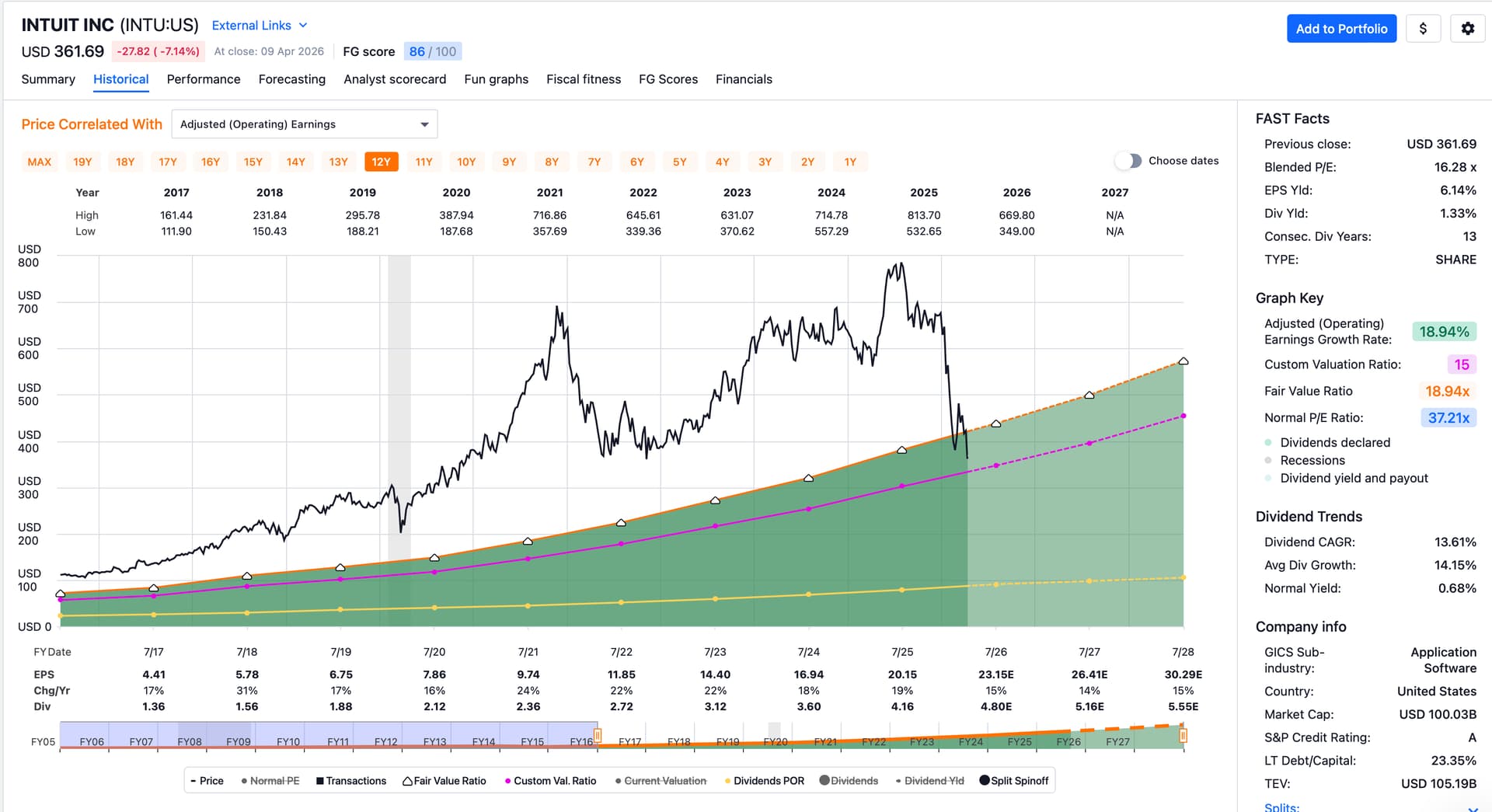

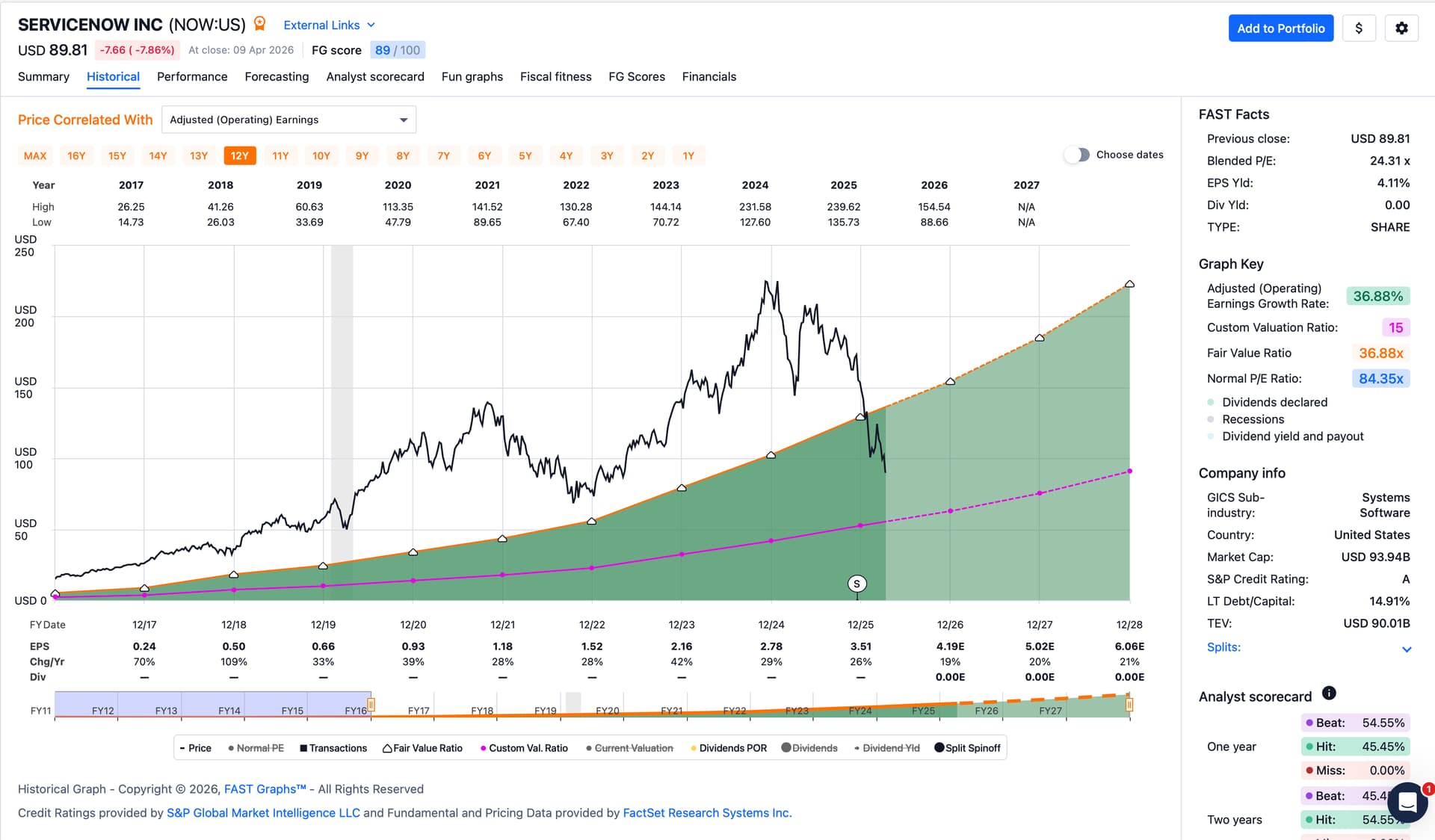

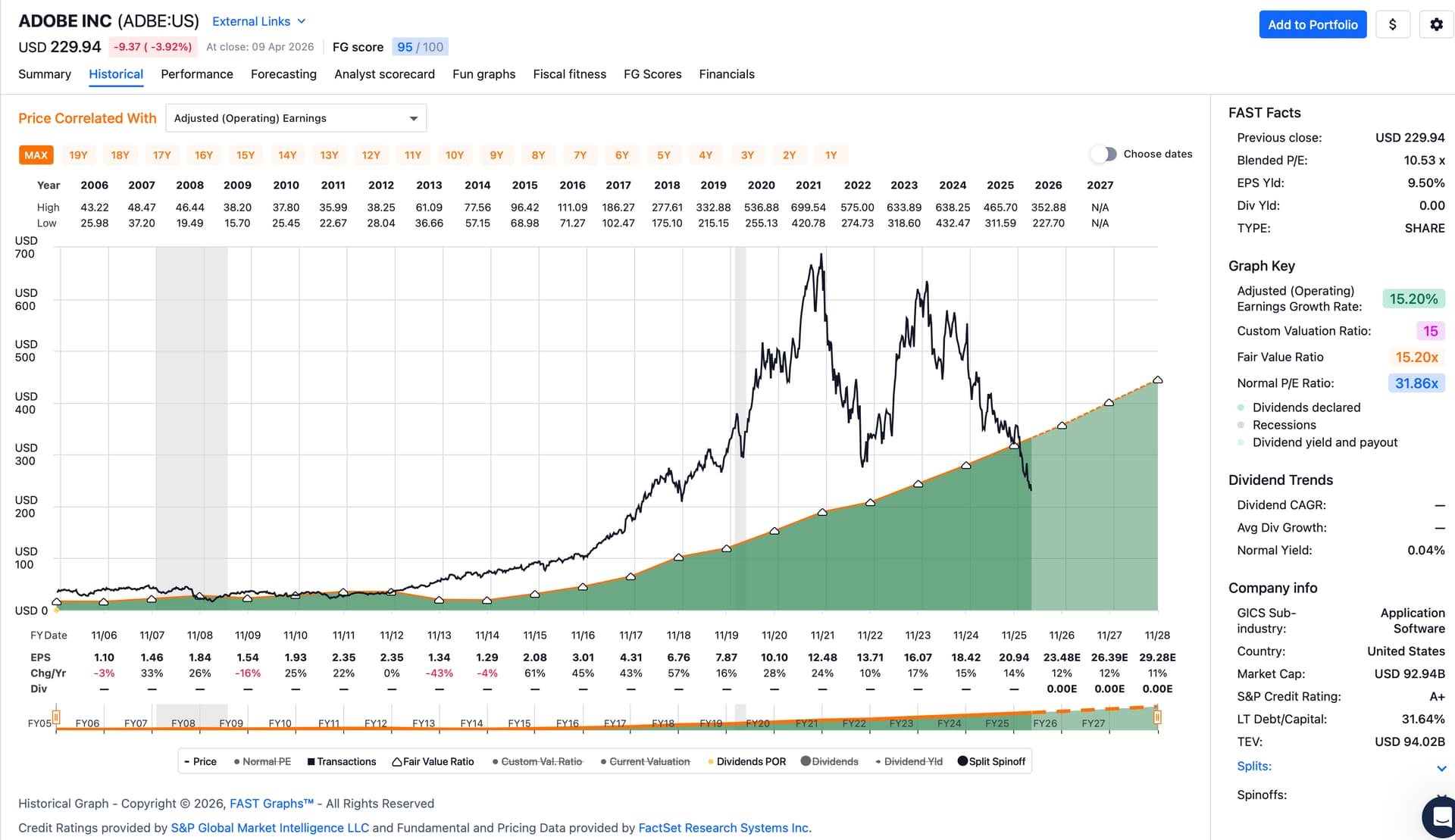

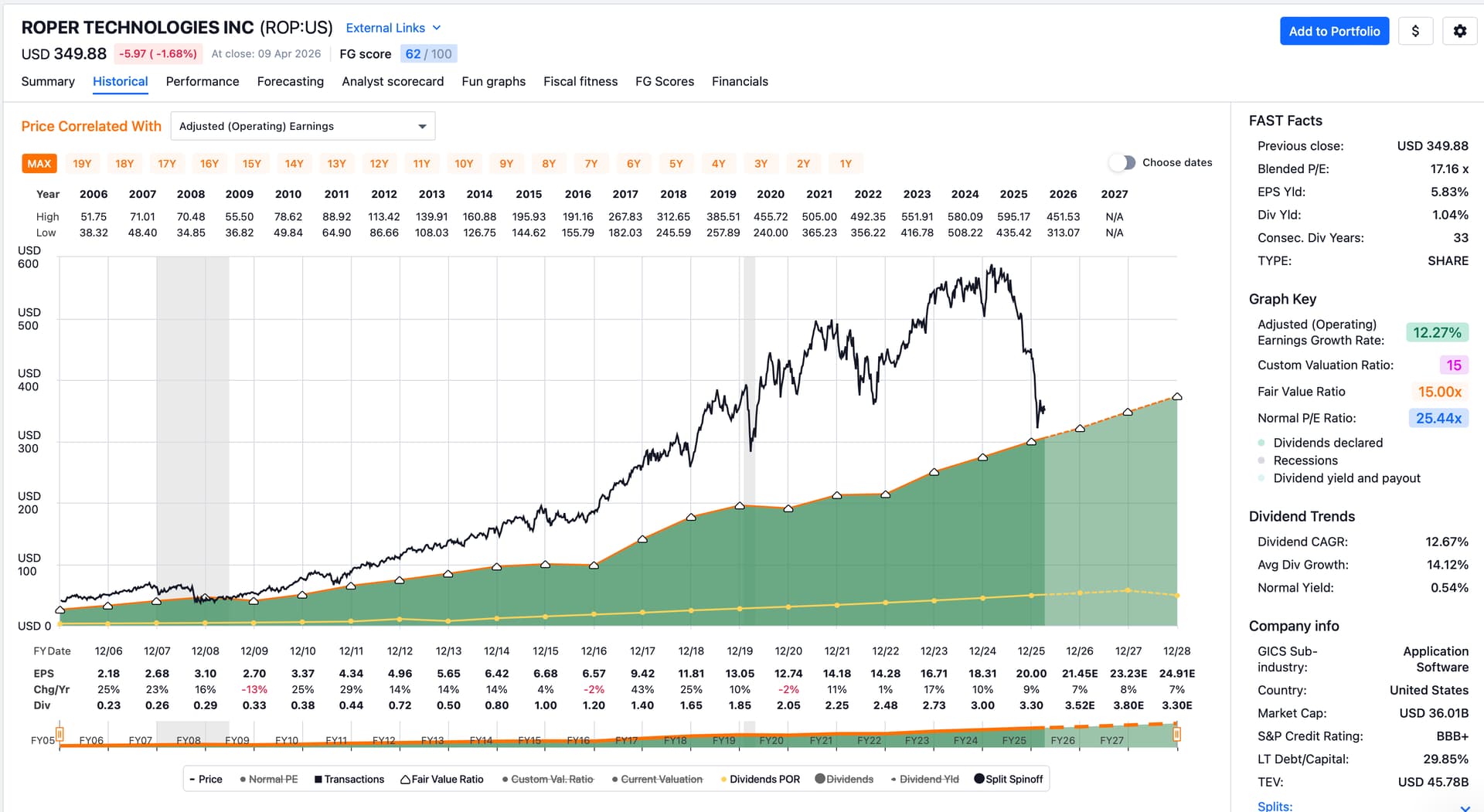

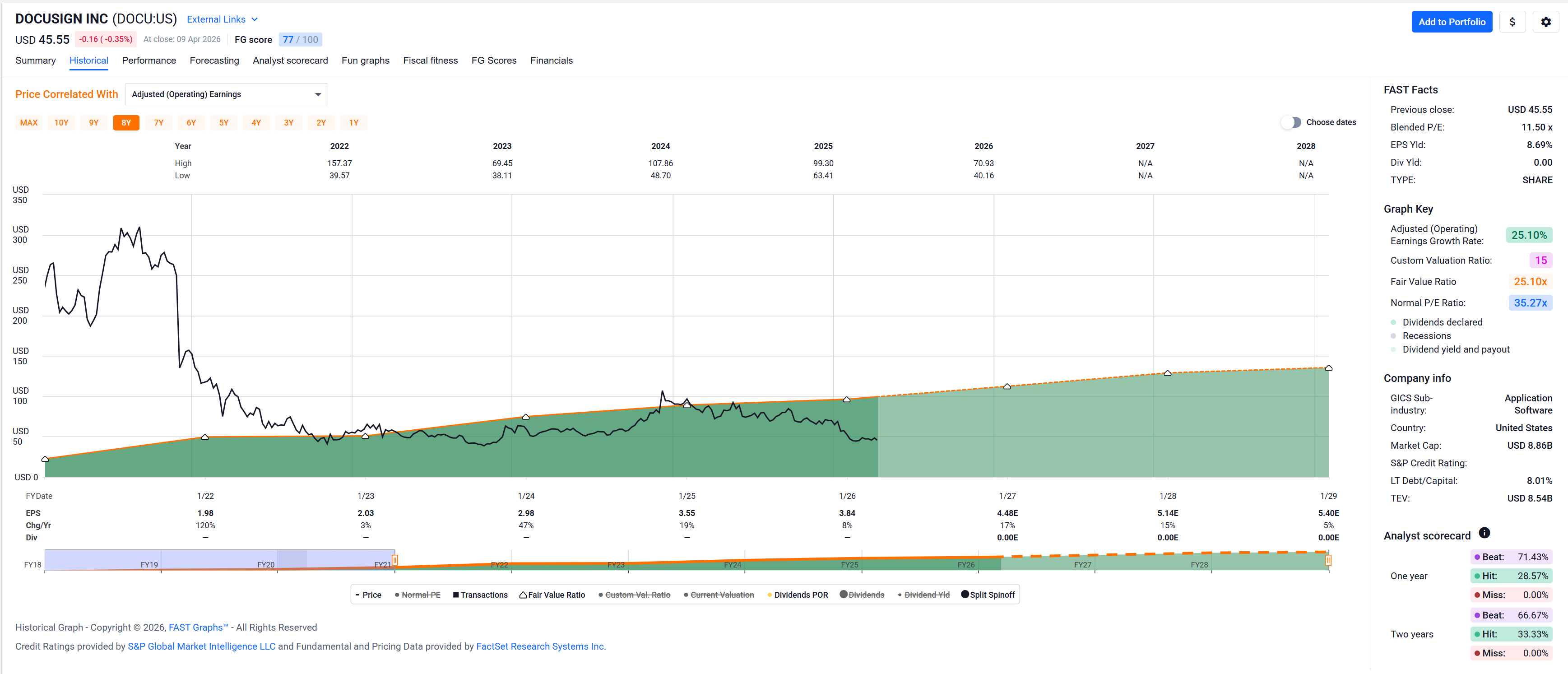

Accenture is the only one I (almost) like valuation wise. The others seem like good businesses (except Paypal which seems to have no growth), but too expensive for me.

Not so optimistic for paypal either, but at this valuation, I’m not sure if they even need growth, they can just chug along and buy back stock to boost EPS.

GWRE is another insanely expensive one, but I keep my eye on it in case it ever comes to value.