And getting uglier again:

There’s a joke out there that WinRAR is more profitable than Open AI.

1 Like

Next up:

ADM

Archer-Daniels-Midland Co. engages in the production of oilseeds, corn, wheat, cocoa, and other agricultural commodities. For company profile details see footnote.[1]

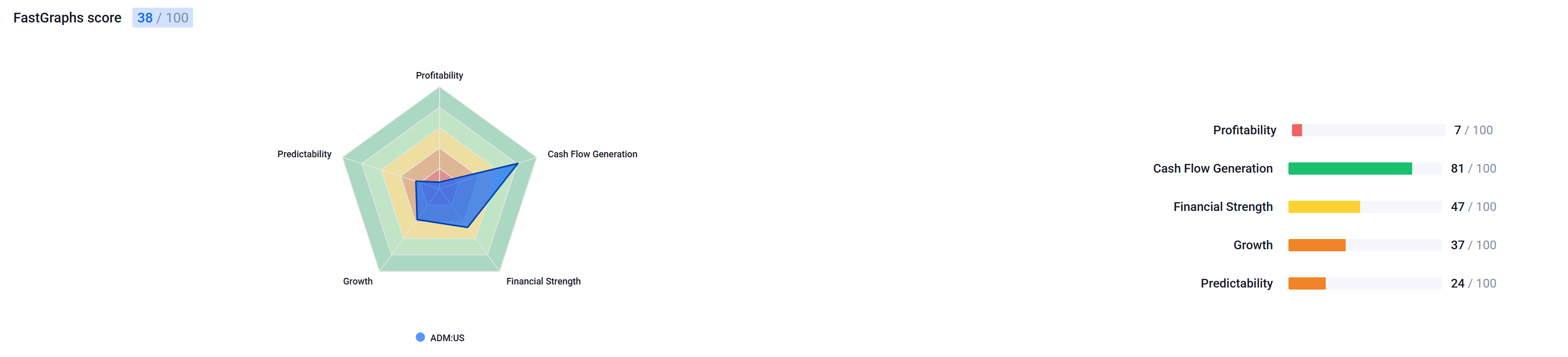

FASTgraphs summary score:

Historical earnings graph, price chart, etc:

Cyclical business (typically not my cup of tea), but realiably been raising its dividend for 11 years with a dividend CAGR around 8% over the past 20 years.

Not the fastest horse in my stable, but reliable and currently even a bit overvalued. I won’t trim the position unless it gets over its skis overvalued, which would be above $80 or so.

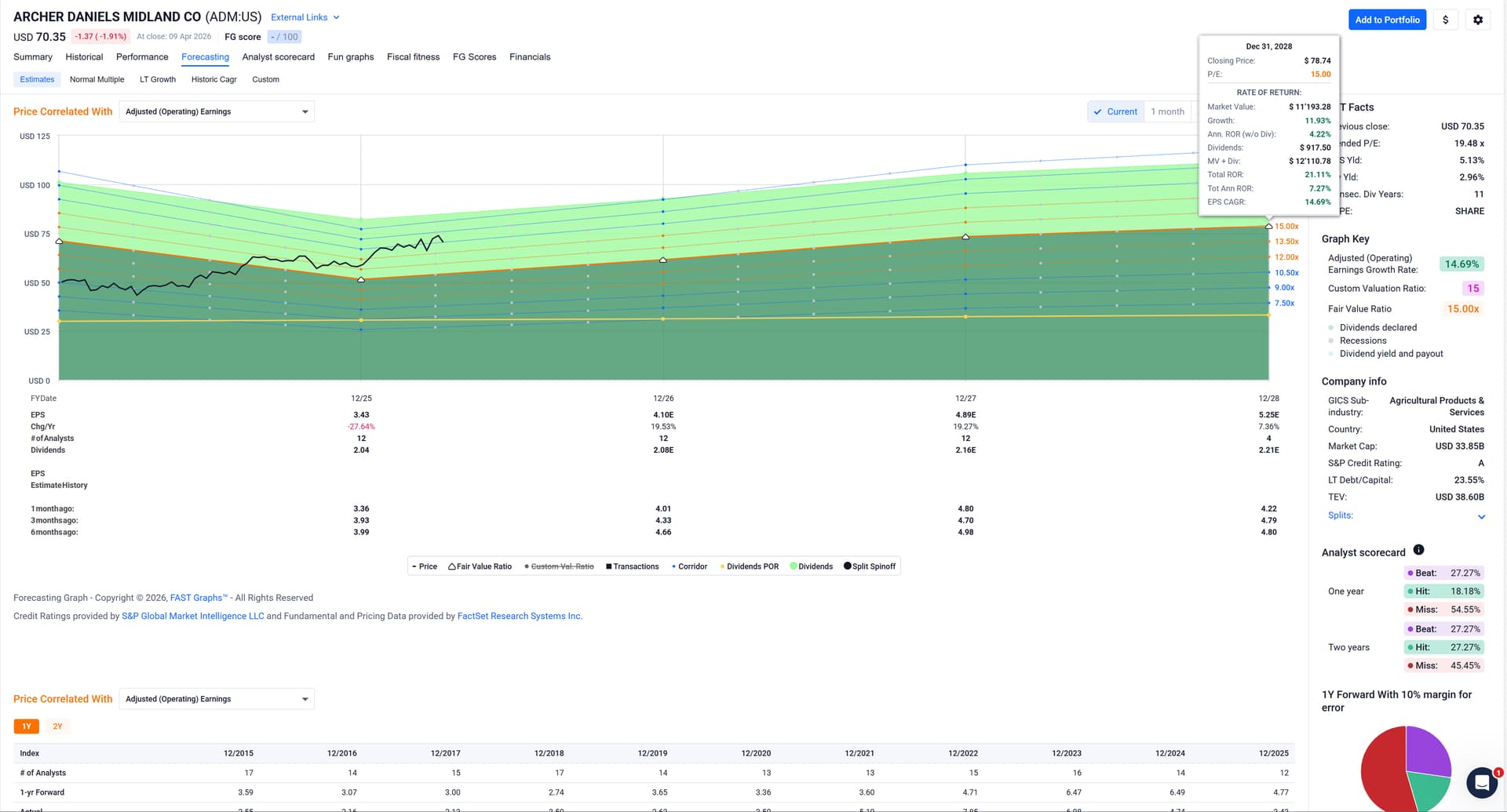

Forward looking earnings chart:

As mentioned it’s not cheap, but even if it returns to a 15 x P/E valuation, I’ll still make some money on this a couple of years out. Earnings wise this one is a little harder to predict as the company is cyclical and company guidance probably varies a lot and/or analysts have a hard time predicting its earnings.[2]

ADM is a hold in my book, tagged with on notice for going onto the watchlist for a partial sell if price goes up another 20% or so.

1 Company profile:

Company description:

Archer-Daniels-Midland Co. engages in the production of oilseeds, corn, wheat, cocoa, and other agricultural commodities. It operates through the following segments: Ag Services and Oilseeds, Carbohydrate Solutions, Nutrition, and Other. The Ag Services and Oilseeds segment includes activities related to the origination, merchandising, transportation, and storage of agricultural raw materials, and the crushing and further processing of oilseeds such as soybeans and soft seeds cottonseed, sunflower seed, canola, rapeseed, and flaxseed into vegetable oils and protein meals. The Carbohydrate Solutions segment consists of corn and wheat wet and dry milling and other activities. The Nutrition segment serves various end markets including food, beverages, nutritional supplements, and feed and premix for livestock, aquaculture, and pet food. The Other segment refers to the company’s remaining operations. The company was founded in 1902 and is headquartered in Chicago, IL.

GICS Information:

Consumer Staples>Food Beverage & Tobacco>Food Products>Agricultural Products & Services

Company website:

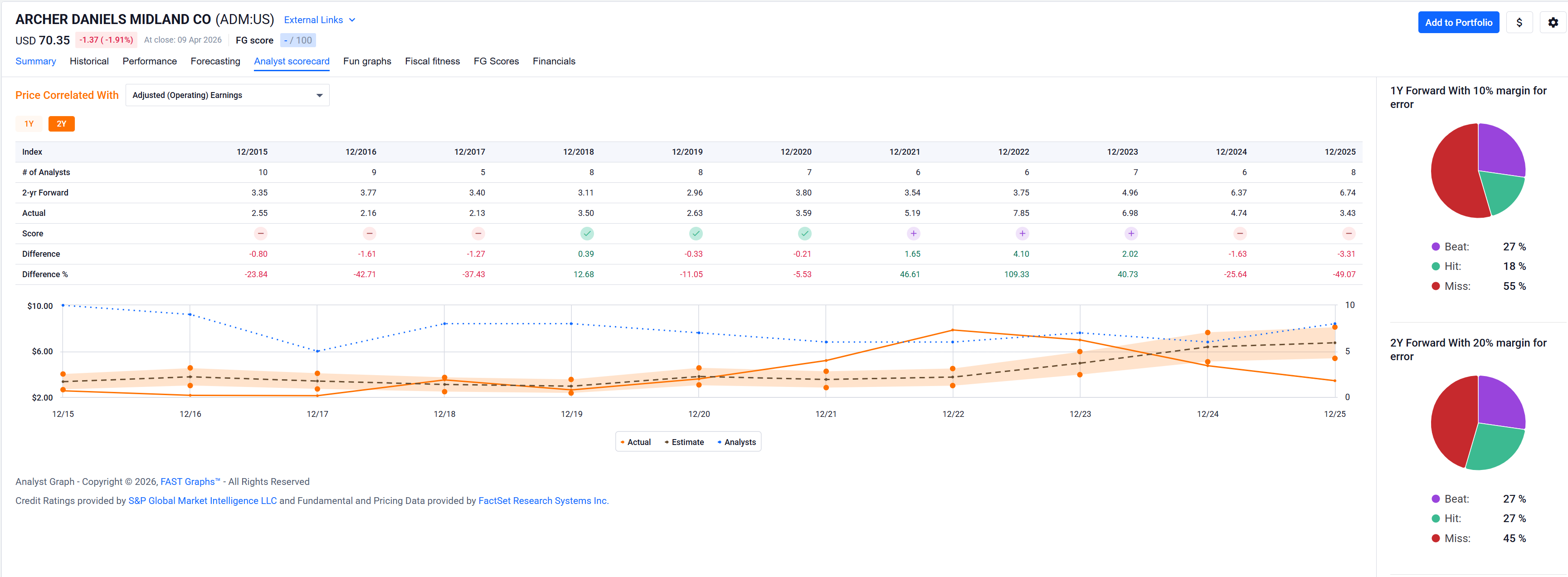

2 Analyst scorecard:

Howard Marks muses a little bit about software in his latest memo:

What’s Going on in Private Credit?

(the memo is mostly about private lending, but he touches a bit on software, too)

They’re both still privately held afaik, but – off topic – I chuckled on your mentioning of WinRAR as it’s had a rich history of security vulnerabilities.

Edit: FWIW (regarding software) I believe this is a market knee jerk reaction for some of these companies. No large company is going to rip out their Salesforce integration that’s deeply integrated in their sales stack, or Workday, which is again deeply integrated with finance and HR.

For some smaller company, maybe the developer vibe coding some “equivalent” app over the weekend will delay the adoption of a more expensive 3rd party app, but not for the bigger customers of those companies, IMO.

Anyhow, pure narrative arguing now, typically not how I want to pick stocks, so please just regard it as a side comment on the software carnage taking place as we speak.

2 Likes

And the whole year nada and now yet another “market dividend” today: Cummins was sold down to 5%.

I could not add to current positions anymore because they are either bigger than 4%, not on buy or from a sector that occupies already more than 20% of my portfolio.

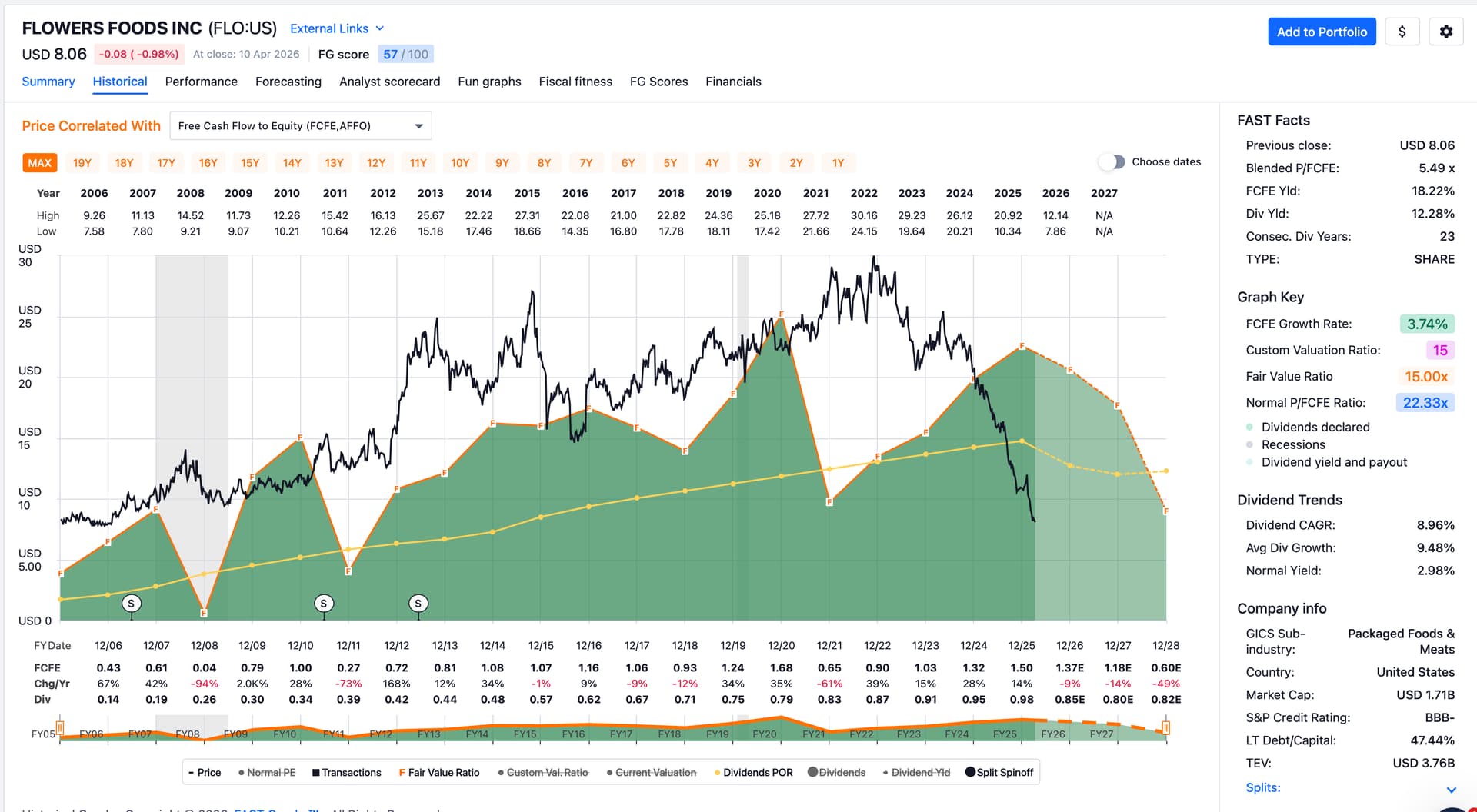

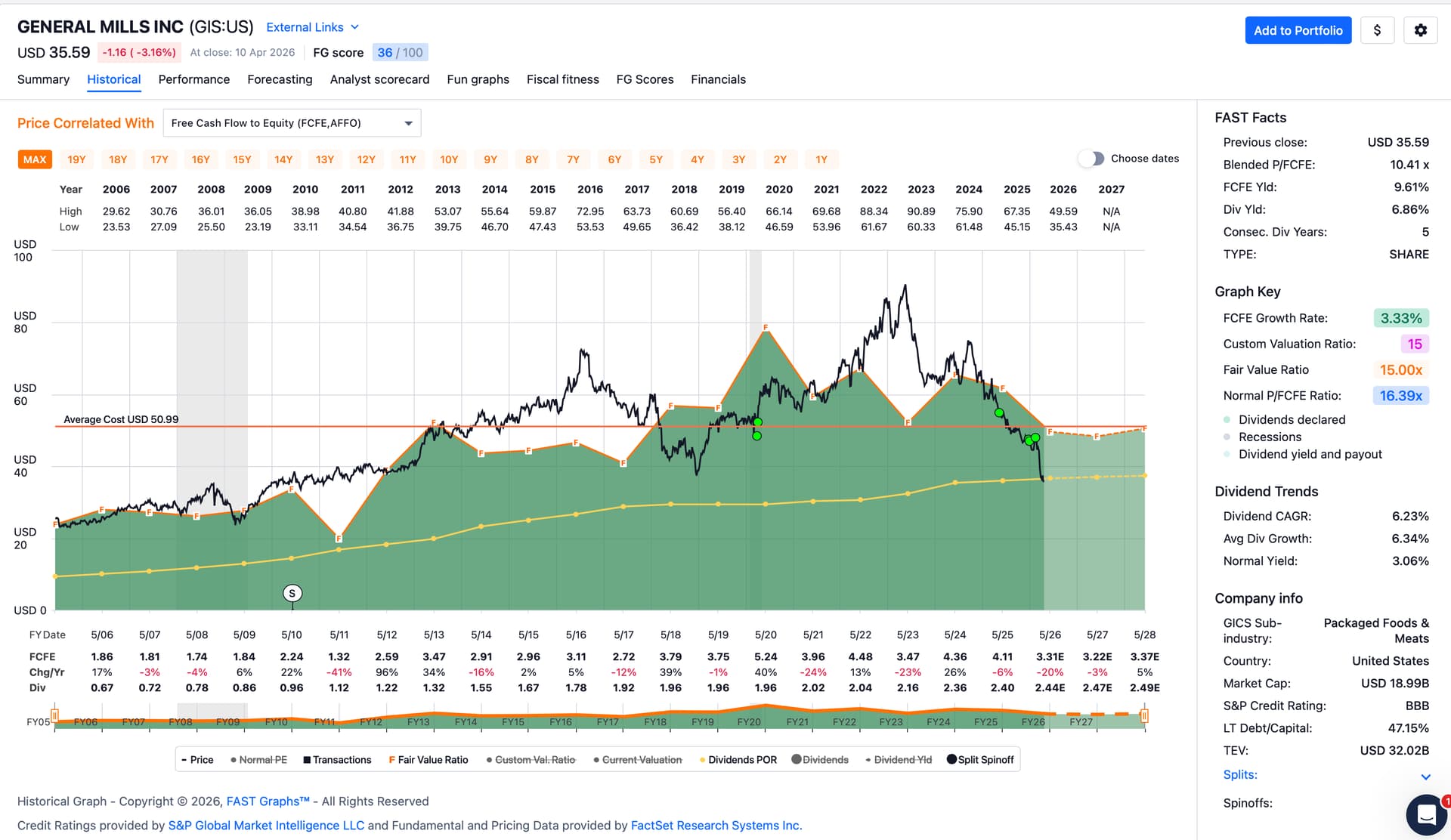

So I bought a new position according to my rules. I had to buy it partly on credit, but with a 12.5% dividend yield that is covered by free cash flow that is not a problem. Chief Falling Knife (GIS) has company now: Flowers Foods (FLO).

Addendum: got it at $7.99, already in the green…

You are braver than me! ![]()

FLO: As many of you know, I ignore earnings. It is the number that is most easy to manipulate, even if it is just to save some tax.

The cash flow statement talks different: the operating cash flow rises since years. They bought some companies last year and that investment may take some time to get profitable.

I really find just one explanation for that market price: passive investment. Nobody analyzes a company any longer. It is bought according to its market capital. Now, if this rises or falls once big a spiral starts to turn and to produce over- and undervalued stocks. On the upper side we can watch this since a decade or so. I think this situation is nice because it produces many chances for me.

Everything is paid from cash flow. That covers the dividend. Nobody knows the future, a company with manageable debt and good cash flow can go bankrupt, but the chances are very small. I want to hold this company for a long time and sooner or later reality gets back to the market price.

Now, a dividend yield of way over 12% is rare and they may cut the dividends. But then, what to do with all the cash that comes in? I prefer them to buy own stock as it is that cheap at the moment. But as I said, they do not need to cut. But if they do, there will be an even better chance to get some cheap.

BTW: as my position sizing in the dividend strategy is simply 4% of portfolio value, that was the biggest single buy ever for me, I am close to all-time high.

Flowers Foods has been on my watchlist and one of my mentors initiated a position recently as well.

They just cut their dividend recently and it looks like their FCF will cover their dividend for another year or two, but I can’t bring myself to buying them.

GIS I still like and it’s on my buy list.

According to their dividend page they did not. Would be strange as the U.S. dividend 100 index was recently reconstructed and they are still present I think. Rising dividends is one criteria of that mechanically constructed index.

Anyhow they pay more than 3% every quarter, so a cut could be possible, would be an erstie for Flowers. I think if the cash flow situation does not change the dividend yield will go down due to market price appreciation. ![]()

1 Like

Huh, you’re right, must be a FactSet glitch.

Thanks for the correction!

Edit: Actually, it’s just me being dumb. The cut is in the forecast part of the graph. And forecasts are just that: forecasts … in this case by 4 analysts that cover FLO according to FactSet.

Given they’ve raised their dividend for 23 years it would be a pity if they cut.

As I said, a cut is possible. Analysts predict a sales downturn and that of course would affect the cash flow. But then operating cash flow was growing all those years and the price went down anyhow. It does not really make sense and I am afraid that analysts are kind of copycats: they may be wrong, but they may not be wrong alone.

Last year they acquired Simple Mills, as always for much too much. Comparable to the Blue Buffalo desaster of General Mills? Maybe, but only the future knows and I left my crystal ball in Switzerland (I am in Spain at the moment).

This is a food company and people eat. That is enough fact for me together with looking at past numbers. Looking at future numbers is analysts game and they have a very bad track record doing that.

Indeed. Guidewire has falling by 50% from peak and is still over-priced!

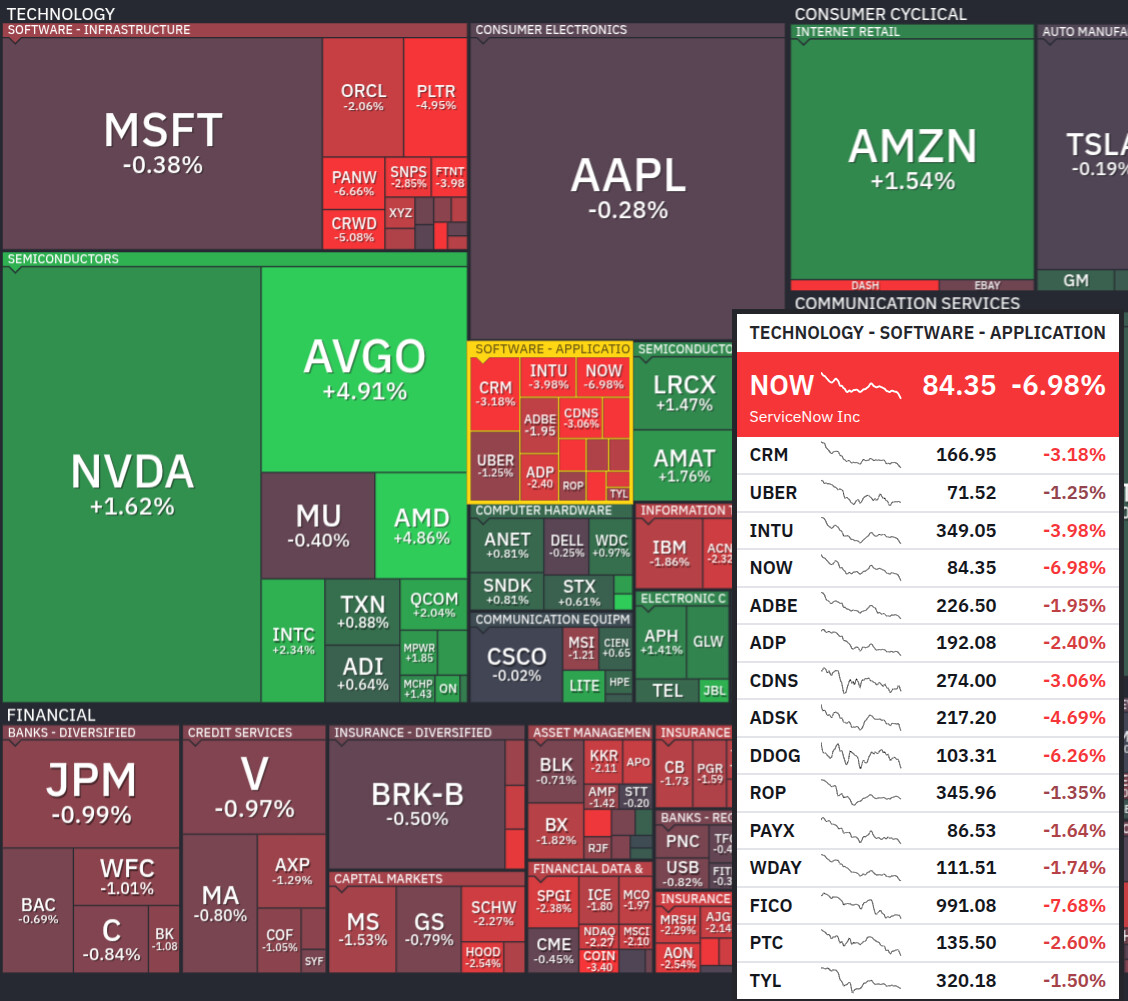

Looking at NOW which has crashed down to $83, it makes me chuckle looking at past analyst recommendations: Dec-17-25 Resumed BTIG Research Buy $1000 ![]()

1 Like

I did dig a bit deeper into Flowers. As I said, the operating cash flow did rise for several years. Last year there was a big position of transitory credit.

But then, as I said too, cash flow statements are not easy to manipulate. So that invoices were real and were paid this year. That could be a pointer to more activity and not less as the analysts predict. I think next month analysts expect a dividend cut, I still don’t see the need. But of course, the company pays 6 times my required dividend, so a cut would not be too hard for me.

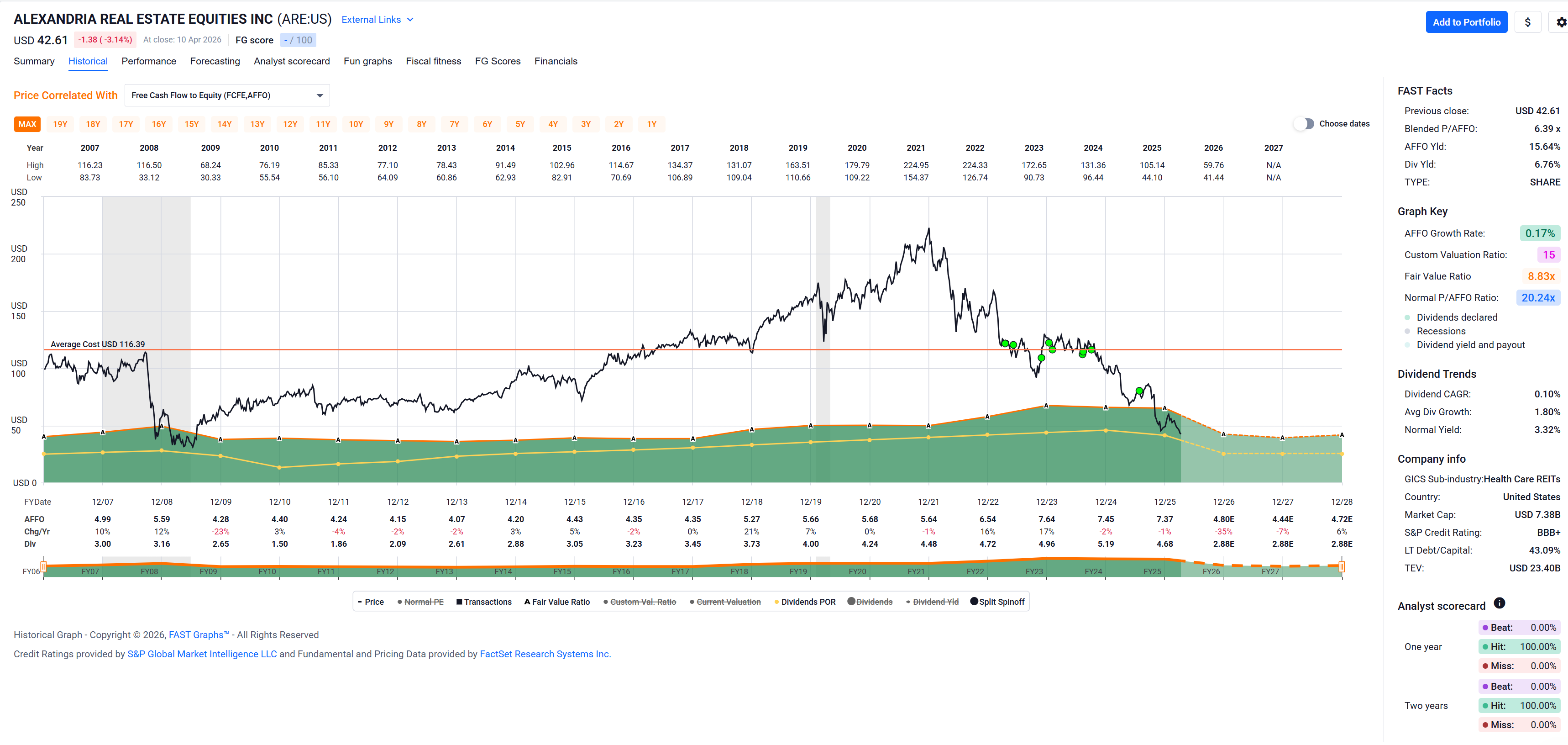

Got rid of ARE[1] today and substituted it with an increased position in GIS.[2]

Typically when I sell I’m looking to replace the (dividend) cash flow that the sell generated with something equivalent that I buy at the same time. ARE and GIS match, yielding about the same at the moment.

I’m getting rid of ARE because they cut their dividend and because my thesis doesn’t hold up anymore: I thought they were a specialized office REIT (for healthcare related companies that use their facilities for research, etc) that is kind of shielded from the office REIT downturn. They were not shielded. They’ll probably do fine long term, but their growth is even more anemic than GIS’, and GIS’ business model seems more robust.

I hope I’m not buying into GIS with them cutting their dividend anytime soon … ![]()

1 ARE:

2 GIS:

I got burned on ARE too.

I am not really into real estate because I own two nice properties. I got burned by ONL, the spin-off from O that I sold recently. My father got burned in the 80s constructing houses and probably still suffers financially from that time,.

I think there is a record of a few centuries of real estate in the Netherlands. Result: it pays more or less inflation, not more.

In Switzerland there was no major real estate crisis since the 80s. But the one in the 80s was brutal and the next one will be worse. There are no market forces in place at the moment because of the “green belt” situation.

House owners get politicians to define a “green belt” where one cannot construct houses. The green belt in Switzerland is thousands of pages of laws and some Kantonal votings. I suppose the same people that voted for the green belt laws (because they sound really green) are now suffering the high costs of renting an apartment.

But that can change any moment, I have seen it in many countries, even in Switzerland. If market forces are left alone there will be no money to be made. House owners can charge more or less what they spend and you can get a nice apartment in Zurich for less than thousand Franks. Banks, which carry “Bankrupt” in their name, will do that: go bankrupt on all the mortgages and people buying houses with 80% credit will lose the house and sleep under a bridge with a lot of debt.

That said, real estate is nice to diversify risk. And that is enough for me to hold some of 'em stocks.

Slightly off topic: “Stockdividenden” and cash for the “last fractional share”

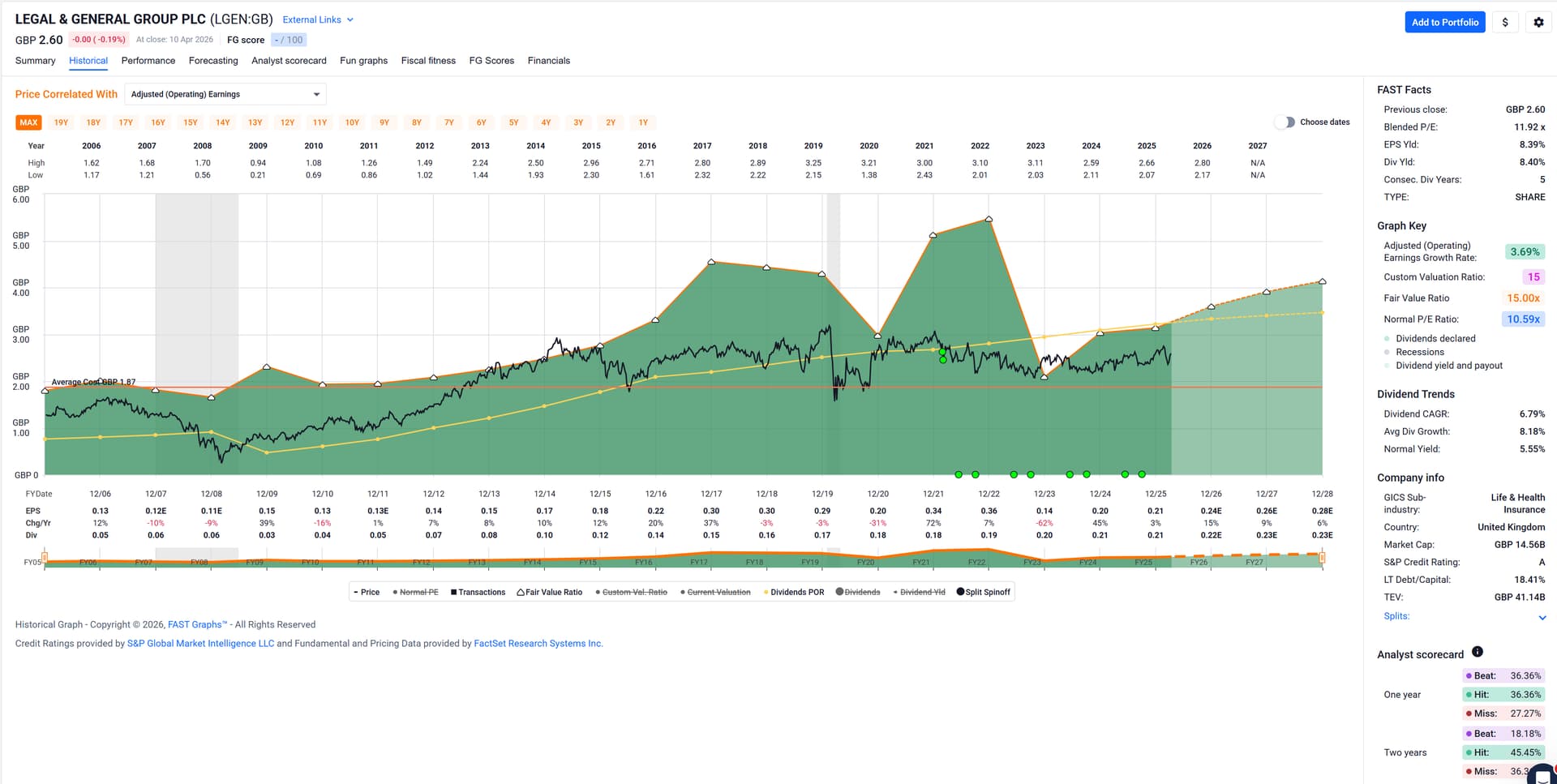

I have two positions – Imperial Brands and Legal & General Group – at Swissquote which offer DRIP (Dividend ReInvestment Program) through corporate actions (i.e. actioned by the issuing company, not the broker). When such dividend corporate actions came up I always chose to DRIP as both companies are still undervalued ever since I initiated the positions.

On payout day (or thereabouts) I receive additional shares – the “Stockdividende” – without me initiating a transaction (Swissquote still substracts a small fee, maybe about 10-20 pence or so, much smaller than if I bought the shares through a standard transaction through broker Swissquote).

The fee structure is what attracted me to receiving the “Stockdividende” instead of receiving cash and buying the shares myself.

About a month ago or so I noticed that the only cash transactions associated with these positions were the fees. However, I expected also cash transactions for the “last fractional share” that was not allocated as a “Stockdividende” as it would exceed the equivalent cash payout and that it would instead be paid out via cash.

I asked Swissquote. Their answer:

Nach Abklärung mit der zuständigen Fachabteilung informieren wir Sie darüber, dass bei Stockdividenden Fraktionen neuer Titel auf- oder abgerundet werden, und nur komplette Positionen neuer Titel gutgeschrieben werden können.

Eine Cash-Überweisung wird demnach nicht stattfinden.

D’uh!

Today I asked my 40 years settlement experience veteran friend and specialist for anything under the hood in trading mechanics – he speaks SWIFT message type almost fluently – how this is properly handled. He told me that the pro brokers offer to their clients to either round up the number of shares received as “Stockdividende” (with additional cash coughed up by the client) or to round down the number of shares received (with the remaining cash paid out to the client). The lazy ones would just automatically round down and pay out the remaining cash.

He has not ever heard of the broker rounding by themselves and no cash flows associated with that … as either the broker would make money off the client (by rounding down) or lose money on the client by rounding up (and who has ever heard of a bank willing to cough up money for the client? ![]() ).

).

I’m on two minds.

- Either just let it go and elect to receive cash dividends. Both positions are actually full, but I bent the rules a bit for both of them since they’re so attractive valuation wise.

- Or … take off the gloves and do a little sparring with Swissquote. I’d honestly be surprised if they have this case covered in their terms and conditions. I instead believe they just haven’t thought about it or were too lazy to implement it properly.

Anyway, has anyone come across this before? Or something similar?

Note that most Canadian or US companies that offer to DRIP – e.g. MAIN, BNS – actually pay out the full cash dividend and new shares are allocated (with the highest integer number of shares possible for the paid out cash dividend), again with a fee much lower than the equivalent broker transaction. The last “fractional share” will remain in cash.

It doesn’t seem right that they steal your money, but being fractional shares, I’m supposing it doesn’t amount to much.

BTW, did you ever own IT or ACN? I’m just wondering about the insane levels of debt for IT.

For Legal & General the share price has been between GBP 2-3 so indeed not a huge amount missed even if all “Stockdividenden” were rounded down from x.99 shares to x shares for the 8 “Stockdividenden” I’ve received so far.[1]

For Imperial Brands the share price has been between GBP 13 and 31. A little heftier, but still a probably smallish amount for the about 21 “Stockdividenden” so far if I counted correctly.[2]

To be honest I am more annoyed by Swissquote’s answer to my inquiry which felt like “let’s give this dumb retail investor just some answer they will probably not understand anyhow” versus acknowledging an issue and maybe offer some compensation (in the past they were fast with “compensating” with free trading fee credit when I pointed out issues that were clearly wrong).

Anyhow, still unsure whether it’s worth following up … but then again … FIRE provides time for fixing the world, no? ![]()

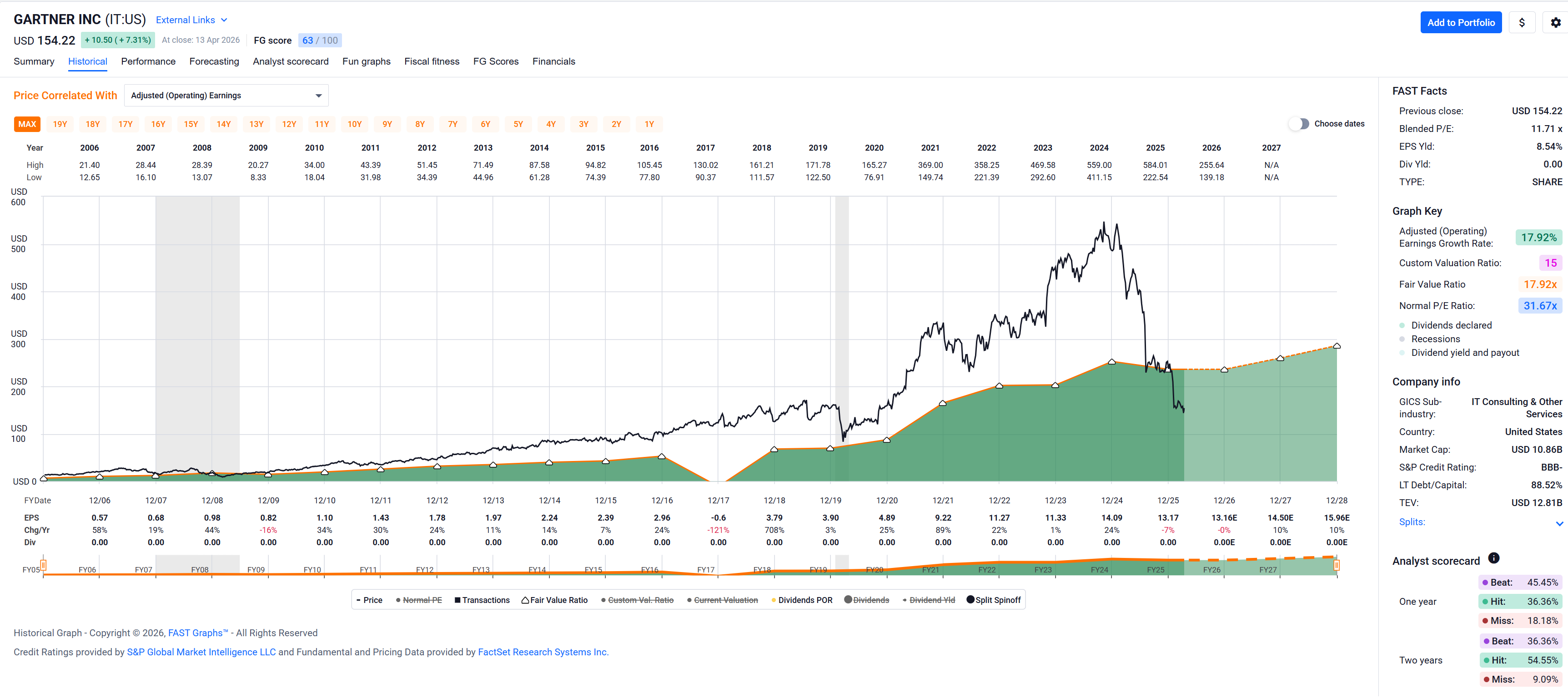

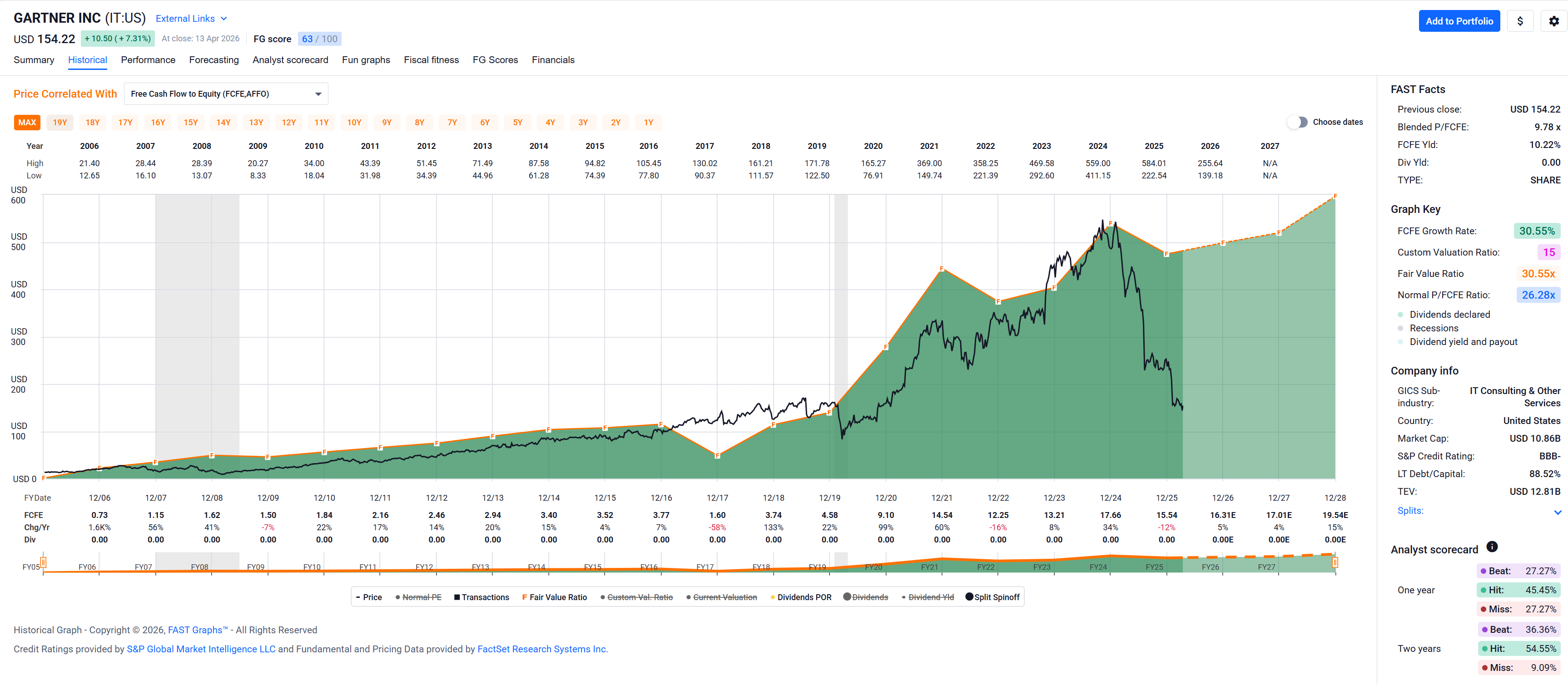

No. Gartner does not pay a dividend, and personally speaking, I never really believed any of their research stuff and only used them (purely as a tool) when e.g. one of their magic quadrants was supporting what I wanted my management to support/buy. If there was no supporing Gartner opinion for what I wanted, I would conveniently leave them out. ![]()

Obligatory FASTgraph:

Edit: Indeed, IT’s debt seems huge. OTOH they still seem to be able to generate lots of FCF to finance their debt:

Ditto for Accenture, never owned them. My early career experience with Arthur Andersen probably shaped me forever regarding consulting.

I was involved in a 2000/2001 e-banking project with a large Swiss bank that consulted with AA and subsequently flew in a team of about 50 AA consultants, all nicely dressed up in a suit, all technically incompetent, to deliver over probably a year or so something that I could have built better with a team of 5 in maybe 2-3 months.

In fact, I built two critical components in their setup that they could not (2FA with RSA tokens and an interface to the proprietary IBM z/OS running mainframes at the time being the only record keeping custody systems at that bank).

Of course, later AA went down alongside Enron …

Anyway, obligatory Accenture FASTgraph:

1 Legal & General:

2 Imperial Brands:

Love it😀