![]()

![]()

he’s found his ikigai

1 Like

Bought some more Smucker[$] the day before yesterday when it dipped for whatever reason.

Fairly slow (earnings) growth, but nice dividend yield (but slow’ish dividend growth) and a nice record of 23 years of dividends raised.

Free Cash Flow (FCF) is a bit cyclical but covers the dividend well.

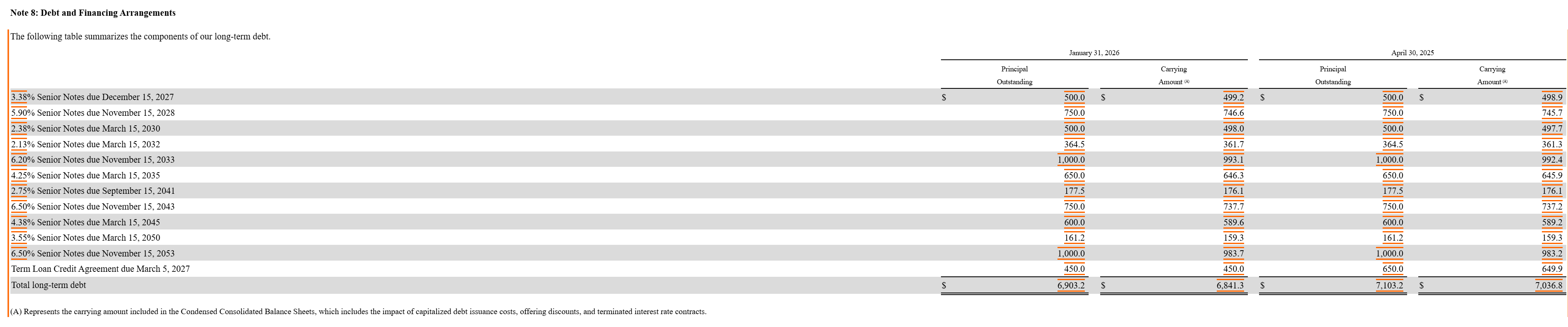

A bit high on debt with almost 55% of long term debt to equity, but decent BBB credit rating. According to their latest 10-Q their long-term debt is fairly staggered out

and again the FCF should cover interest payments on their debt well.

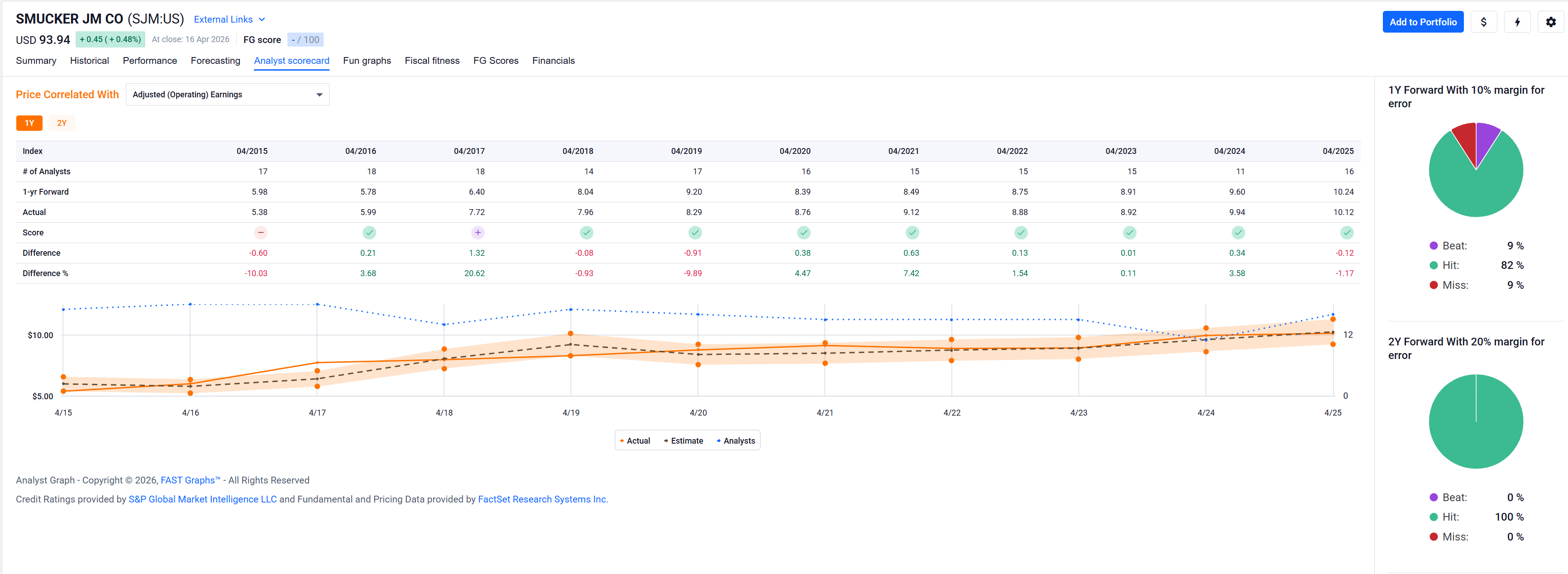

Price has been falling essentially since the weight loss drugs came out. Market fears that nobody’s going to eat their junk food anymore. Goofy believes differently. Earnings and cash flow predictions by analysts also point in a different direction and analysts have a near perfect track record for this company:

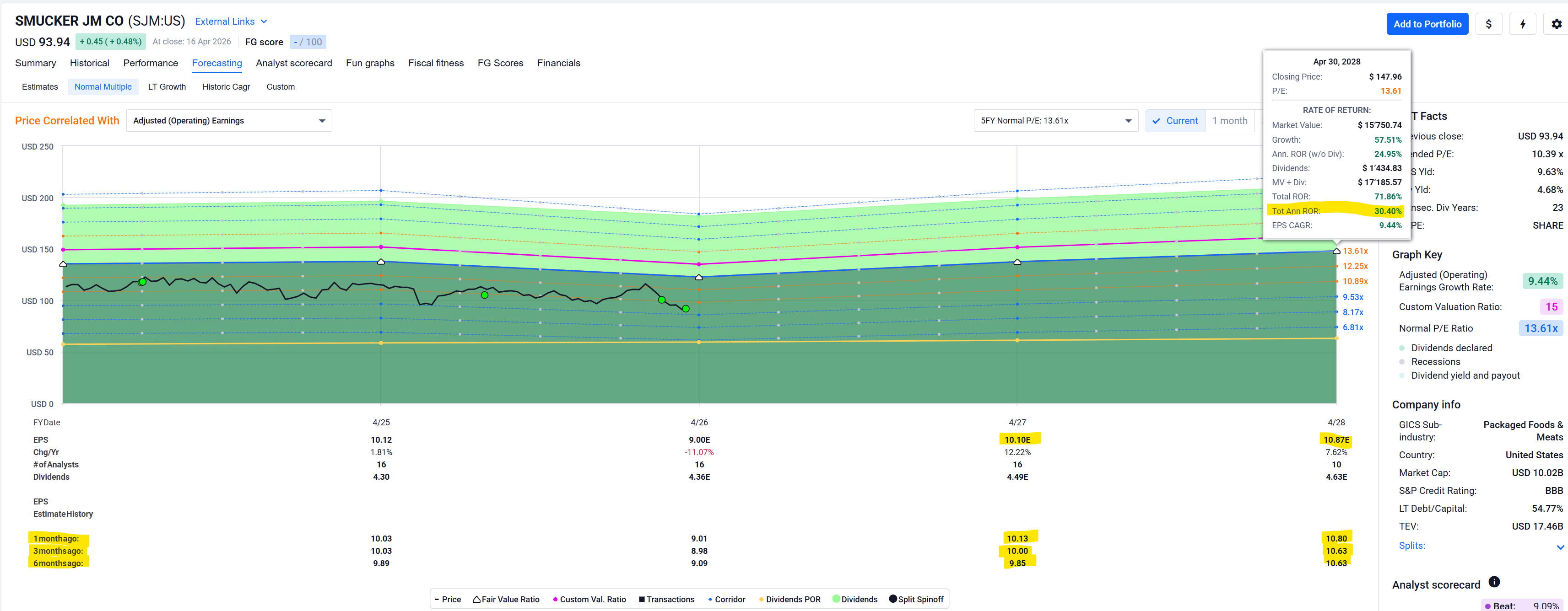

If the company returns to its normal multiple of about 13.6 x P/E, then I’d be looking at a 30% total annualized return which is fine by me … ![]()

… if not, I’ll just have to get by on the dividend, which is fine by me, too. I also like that their earnings forecasts for a year or two out have been mostly stable in the forecasts half a year ago to just about a month ago.

Today I also noticed that the company’s chairman and CEO is also a Smucker, a fifth-generation member of the family. I kind of like that. Half of his relatives will be breathing down his neck if somehow tilts towards messing up the business …

$ The J. M. Smucker Co. engages in the manufacture and marketing of food and beverage products. It operates through the following segments: U.S. Retail Coffee, U.S. Retail Frozen Handheld and Spreads, U.S. Retail Pet Foods, and Sweet Baked Snacks. The U.S. Retail Coffee segment includes the domestic sales of Folgers, Dunkin’, and Café Bustelo branded coffee. The U.S. Retail Frozen Handheld and Spreads segment focuses on domestic sales of Smucker’s and Jif branded products. The U.S. Retail Pet Foods segment is involved in the domestic sales of Meow Mix, Milk-Bone, Pup-Peroni, and Canine Carry Outs branded products. The Sweet Baked Snacks segment refers to all domestic and foreign sales of Hostess and Voortman branded products in all channels. The company was founded by Jerome Monroe Smucker in 1897 and is headquartered in Orrville, OH.

1 Like

It is like your broker declares love and wants to marry you. BUY BUY BUY

Still hold PBF, I am made that way. I’ll hold until I can press out some life-on (Goofy: I hope it is not life on)( I don’r know that fancy changes of fonts)) money out of them. The whole state of California will go under a bridge but that company?

1 Like

Energy is really getting beaten up today. My Valero (VLO) position is down a nice 10% today, and even Chevron (CVX) and Exxon (XOM) are down 5% or 6%.

It’s the efficient market showing off its efficiency, probably.

A day is a day. I don’t own that energy stocks but I bought oil all over the world since October. Had the all-time high a bit before the S&P500 and now I just lean back and watch.

I will probably pay a bit more this time when I fill my oil tank (4’000 liters). I do not even watch the price but just fill it up when it gets empty, every 30 months or so, This time I hope to pay really really much so my oil stocks rise.

Just to share the hurt: PBF -12.83%, LYB - 11.98%, CVI -10.41% and so on. I just lean back and wait. Remember, I am the Managing Siesta Director!

Next up:

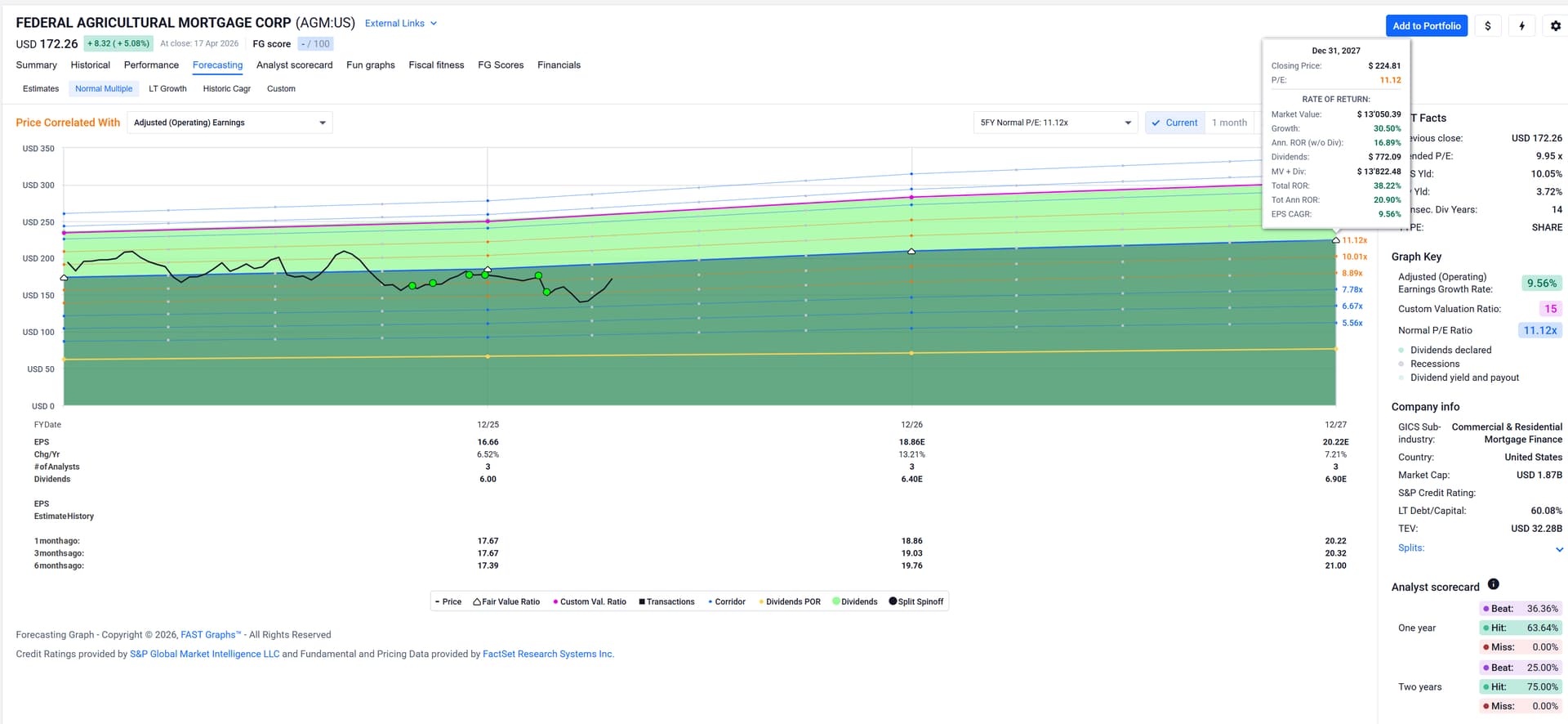

AGM aka “Farmer Mac”

Federal Agricultural Mortgage Corp. is a stockholder-owned, federally chartered corporation, which engages in the provision of a secondary market for a variety of loans made to borrowers in rural America. For company profile details see footnote.[1]

There is no FG Score available for this company.

Historical earnings graph, price chart, etc:

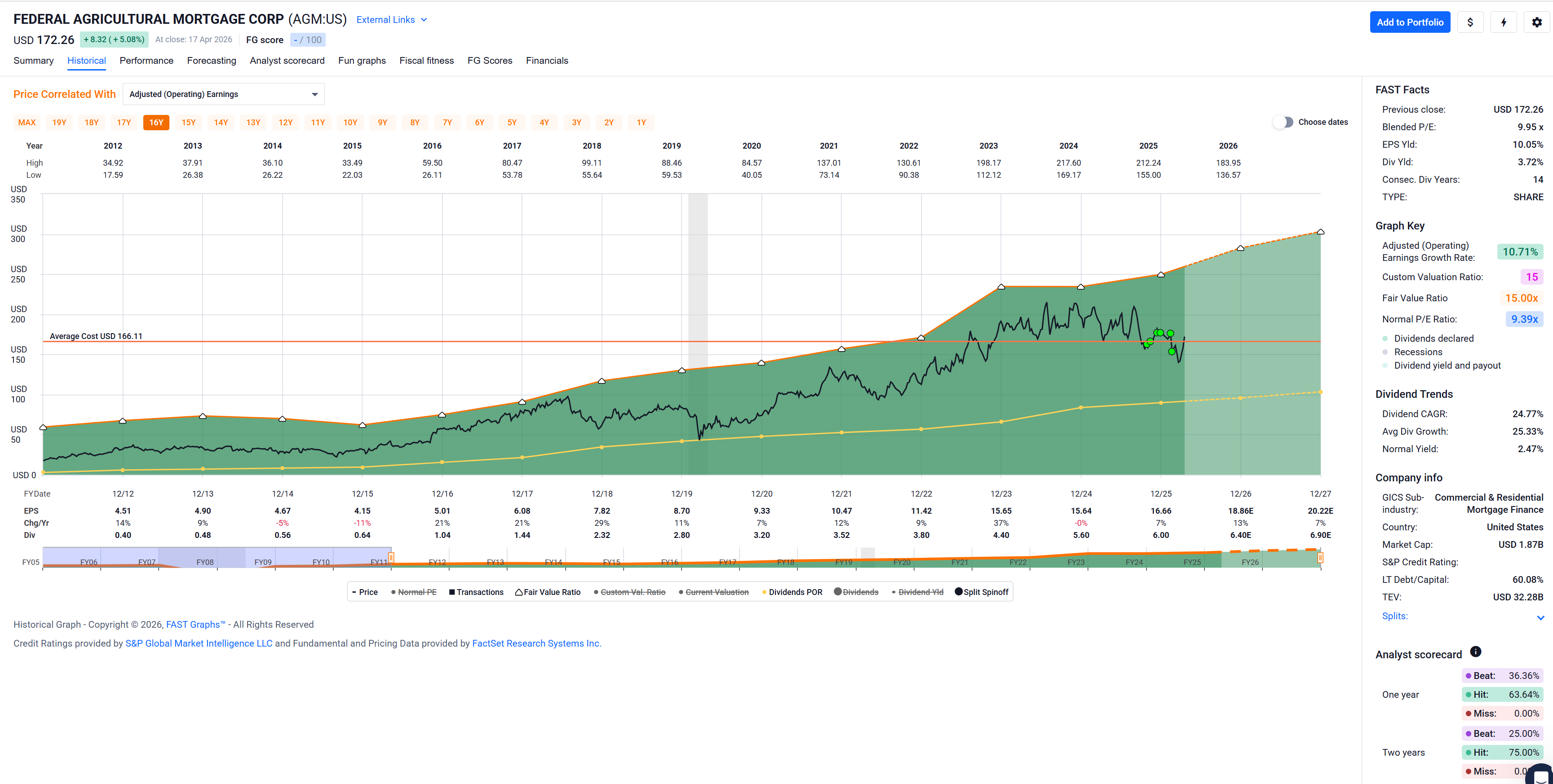

Steadily growing earnings since post the Global Financial Crisis, raised their dividend for 14 years with a dividend CAGR of around 25% (!).

It’s a little high on debt, but since it’s federally chartered, there is an implicit guarantee that the government wouldn’t let it fail.

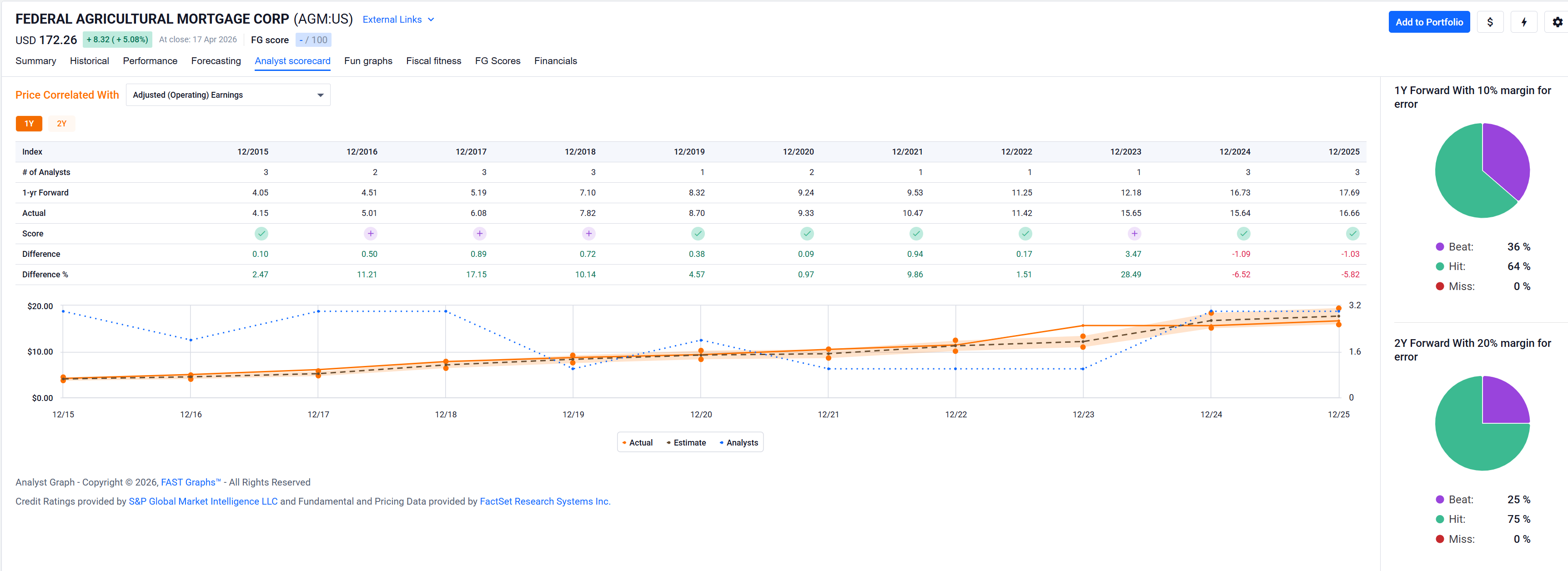

It also hits or beats analysts’ earnings expectations 100% of the time.[2]

Forward looking earnings chart:

It’s fairly cheap, but its normal valuation has only been about 11 x P/E. If price returns to that normal valuation, I’d be looking at a 20% CAGR (total return). If it somehow returns to its fair multiple of 15 x P/E, I’d be garnering a fat 40% CAGR (total return) … one can always dream.

AGM is a buy in my book. I’ll add opportunistically when I have cash and when it dips.

1 Company profile:

Company description:

Federal Agricultural Mortgage Corp. is a stockholder-owned, federally chartered corporation, which engages in the provision of a secondary market for a variety of loans made to borrowers in rural America. It operates through the following segments: Farm and Ranch, Corporate AgFinance, Power and Utilities, Broadband Infrastructure, Renewable Energy, Funding, and Investments. The Farm and Ranch segments includes the USDA Securities portfolio, Farm and Ranch loans, and AgVantage securities. The Corporate AgFinance segment focuses on loans and AgVantage securities to larger and more complex farming operations, agribusinesses focused on food and fiber processing, and other supply chain production. The Power and Utilities segment refers to the loans to rural electric generation and transmission cooperatives, and distribution cooperatives. The Broadband Infrastructure segment represents the loans to rural fiber, cable and broadband, tower, wireless, local exchange carrier, and data center projects. The Renewable Energy segment is involved in the rural electric solar, wind, and gas projects. The Funding segment consists of debt issuance, hedging, asset and liability management, and capital allocation strategies. The Investments segment provides a financial result of the investment portfolio, which is held for liquidity purposes. The company was founded in 1987 and is headquartered in Washington, DC.

GICS Information:

Financials>Financial Services>Financial Services>Commercial & Residential Mortgage Finance

Company website:

2 Analyst scorecard:

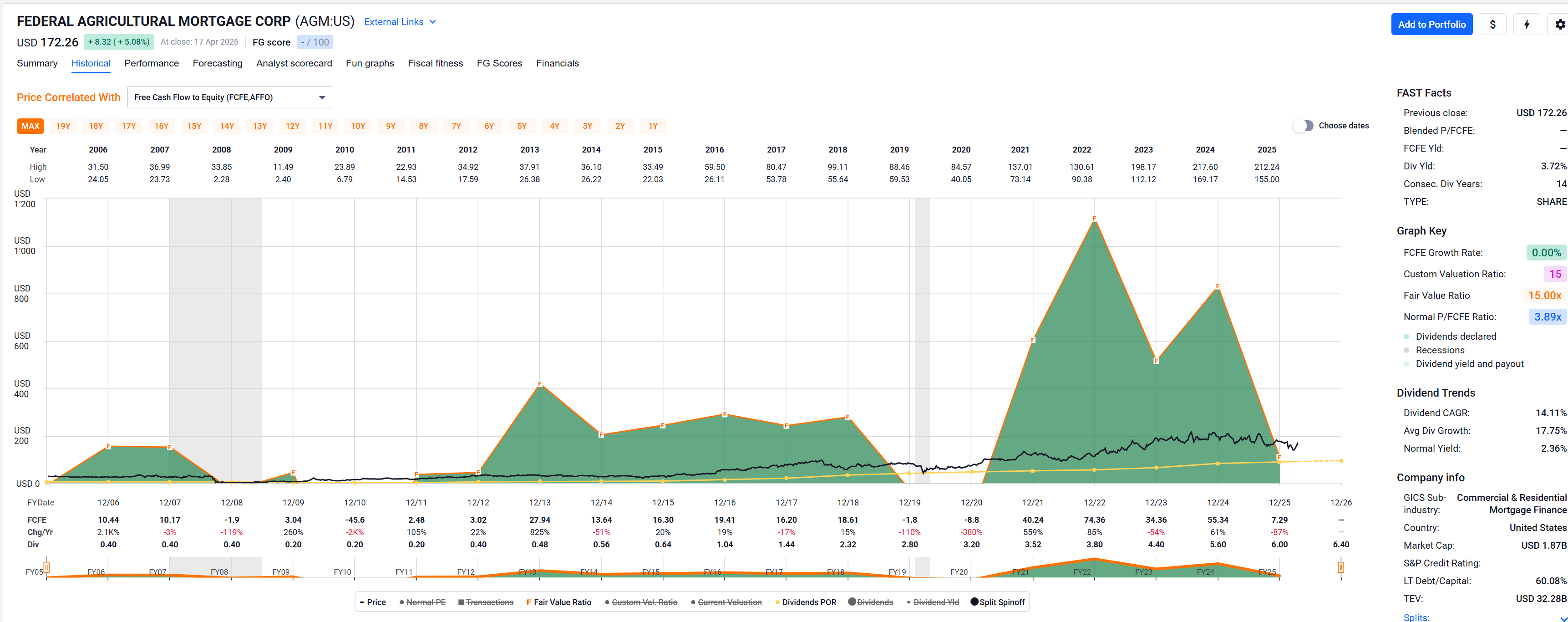

AGM is part of the U.S. dividend 100 index. Financial stocks are always a bit difficult to analyze, but here there are some red flags for me:

- FCF/Dividend payout ratio is over 100%

- Enterprise value divided by FCF is like >400. They don’t work very efficient with their capital.

- Debt would be almost impossible to manage if it were a private company. It seems to be more of a state supported institution. Otherwise it could go bankrupt any moment according to my cash flow formulas. That does not mean it has to go bankrupt, but the risk is higher than I like.

The business model is basically “lend me money and I lend it out for a bit more interest.” That is very risky, not my pair of shoes. If I want to do that I use my own good credit, but I would rather not.

1 Like

I guess they’re a little bit of a special snowflake by their “state guarenteed” status …

You’re right, FCF looks iffy, even in FASTgraphs. For a “normal” company/business this would be a red flag (unless they’re capital intensive, like e.g. Energy or Basic Materials companies).

OTOH they’ve had multiple years without any FCF where they still paid (and even raised!) their dividend. They only cut during the GFC (but still paid a dividend) and have been raising it for many years now since post GFC.

I agree with your description of the business model, but to me that’s the exact definition of not risky if you have the government as a back stop. The government simply won’t let them go bankrupt, IMO.

I also like that they’re tiny (market cap about USD 2B). They’re under the radar (I am actually surprised they’re in the U.S. dividend 100 index) and if indeed shit hits the fan, USD 2B is pocket change for the US government, a rounding error in the US budget.

Anyhow, this is what makes a market. ![]()

Yes. But that is a single big risk that I am not willing to take.

Many utilities are in a similar situation. But then I just don’t understand why they have to pay a dividend at all. If the dividend is not covered by cash flow they pay it rising debt. That sounds to me like moving money from your left pocket to your right pocket, paying tax inbetween.

I was criticized a lot for avoiding many utilities for that exact reason. But I think I did good to do so, At the end the Dollar-gained-by-unit-of-risk counts for me.

1 Like

Betting against the US government, eh? ![]()

Jk, I understand you probably mean the risk of the US government not backing them in case of bankruptcy.

I like my utes. Buy them at a decent valuation and live happily ever after since (almost) nothing will ever happen to their earnings and dividend CAGR …

… and occasionally, they even get ridiculously overvalued, e.g. when AI needs more power or so.

I suppose your cash flow consumption and mine are different as I rely mostly on (steady and growing) divvies while you live off total return. If I pursued the latter, maybe utilities wouldn’t be my cup of tea, either.

Not really. But I think there is a difference between keeping up a utility or a credit institute. If they go bankrupt it is more than probable that they are saved. But that does not mean that stockholders get paid anything.

1 Like

What’s going on with CPG?

CPB, GIS, CAG, KHC all have had terrible performance the last few years.

Yes, check the charts here.

As I always say and said here, sector diversification is the most important kind of diversification… not country diversification as is en vogue at the moment. If a sector does bad it does bad in all countries!

My sector diversification in the divi strategy looks good, no sector with more than 20%. Good companies performing bad is actually a good thing, you get them cheap. The problem is to find out if the performance is bad because it is not a good company. That’s what my numbers and formulas are for…

IMO they’re all in general suffering from the weight loss drugs (just like SJM) and suspected fear that nobody is going to eat carbs ever again.

Additionally, Campbell ain’t really growing much and expects earnings for FY 26 (ending in July) to drop by about a quarter.

It’s kind of unbelievable they were valued at 20 x P/E as recently as at the end of 2022. I guess they’re a household name and maybe were bought because of that?

I bought GIS just a little over a week ago. As mentioned they’re similar to SJM, IMO.

Conagra Brands is again a slow grower.

Not sure why they were ever overvalued …

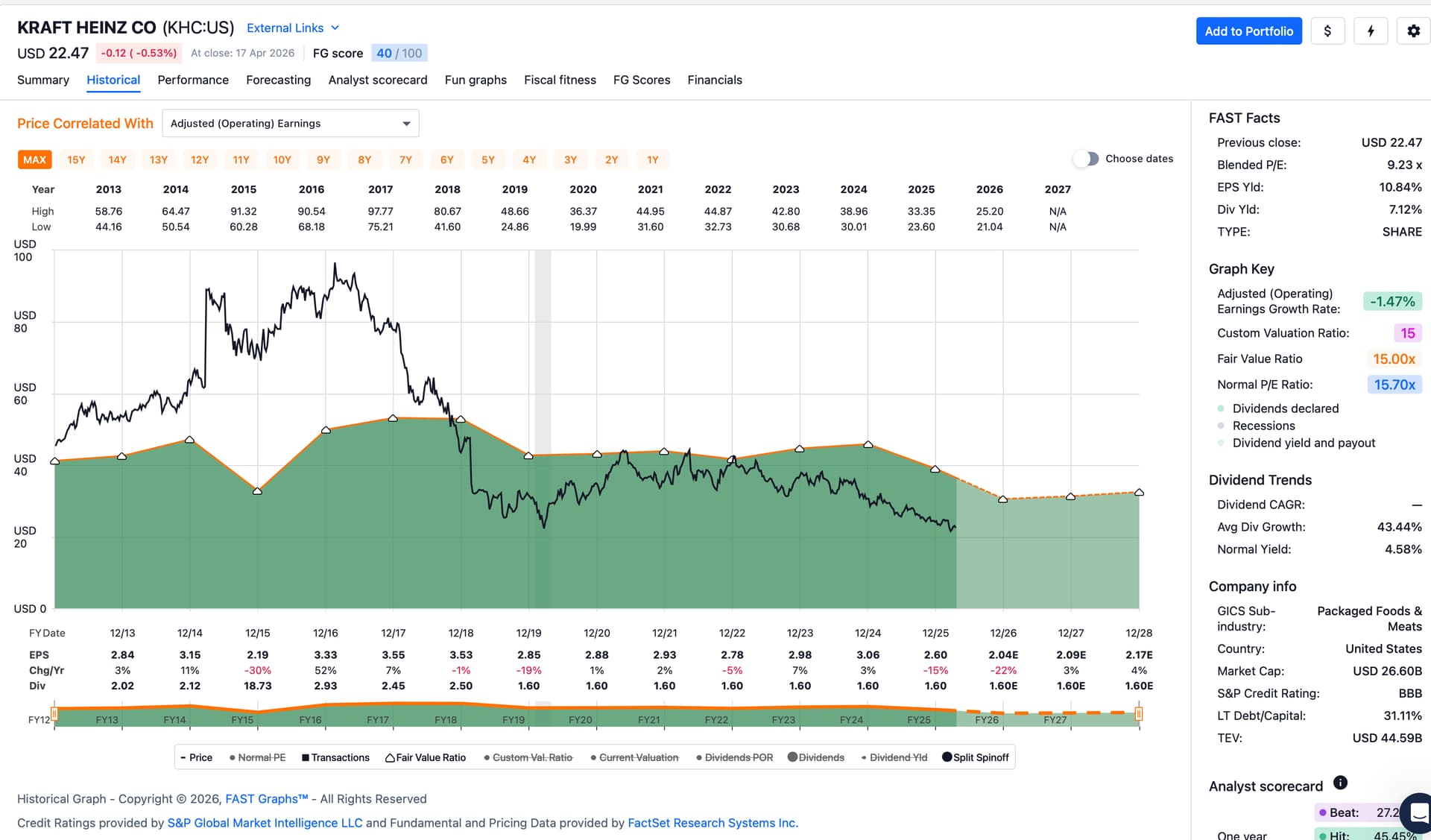

And finally Kraft Heinz … well, they’re shrinking.

(I left the dividend line out as their special dividend in 2015 distorts the chart.)

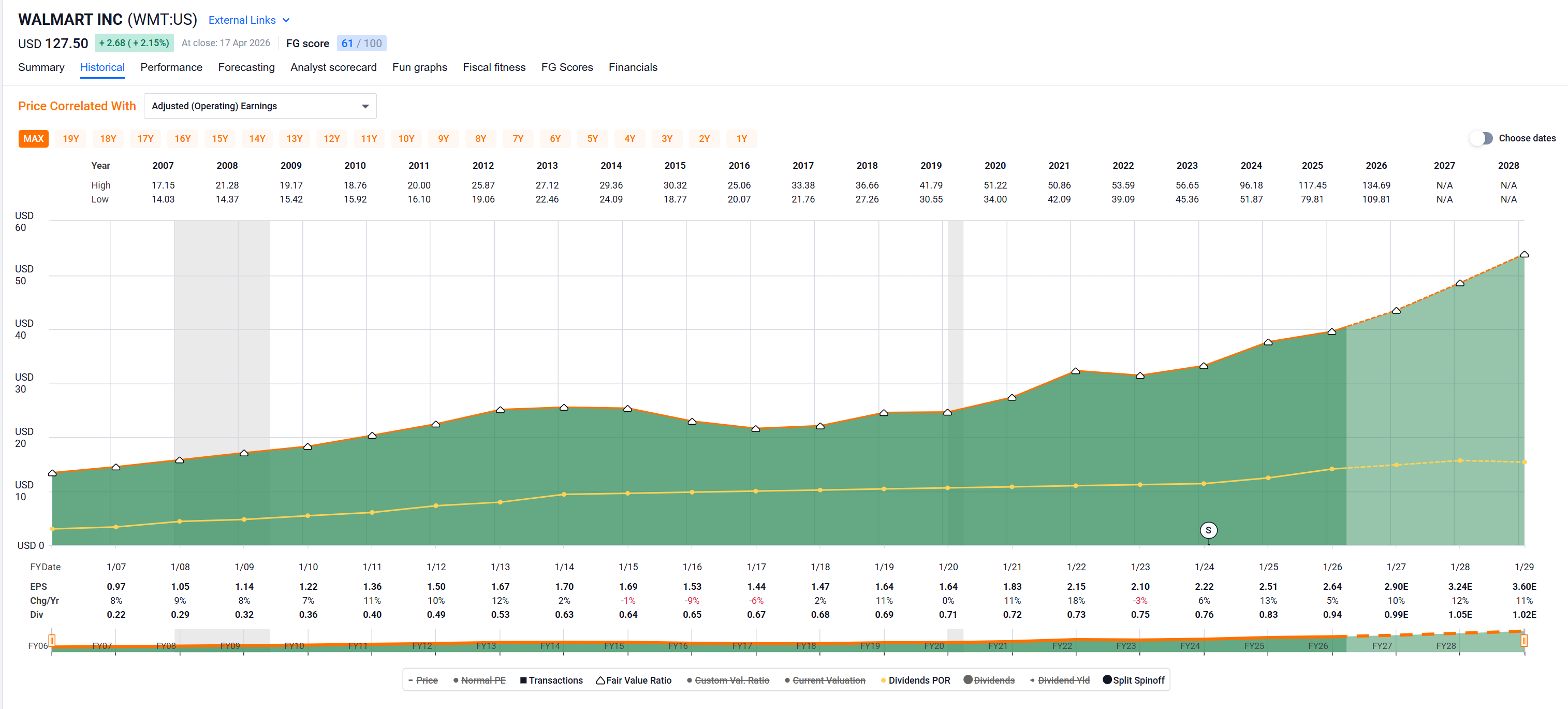

Well there are a lot of high valuations. WMT at >40 PE?! Not to mention the SaaS stocks…

True, but at least the earnings go (mostly) steadily up:

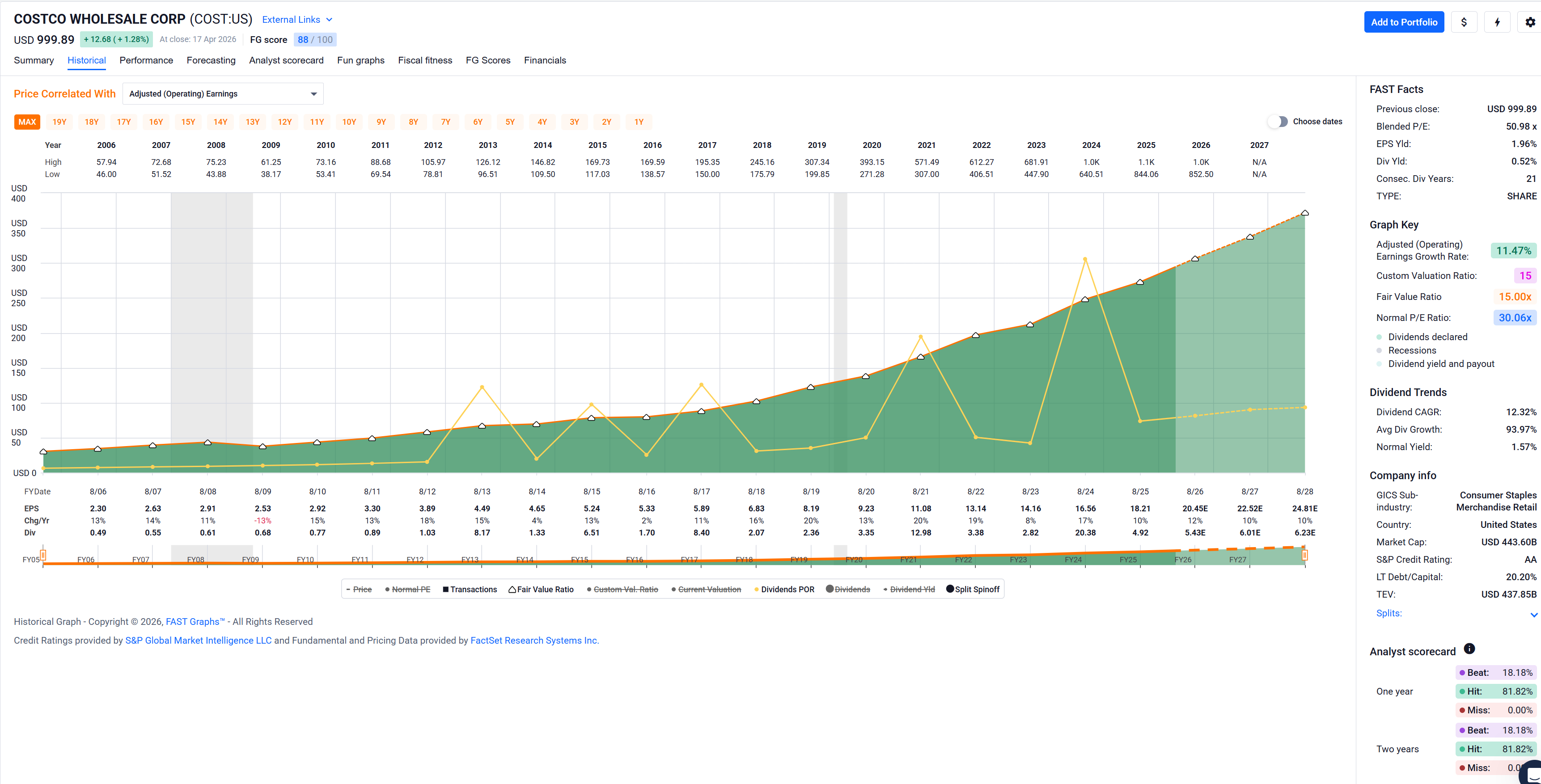

I’ll one up you with Costco at 50xP/E …

Now, that’s what I like to see as an earnings curve …

That is pretty crazy. How can you justify paying 50x earnings?

Easily explainable: Costco’s $1.50 All Beef Hot Dog and 20 oz. Soda (with refill):

![]()