I am always the bad guy here, but then I did not find anything new to invest in for some time.

Costco is strange and it does not generate enough cash flow compared to it’s enterprise value. Yes, I know, that may be not that important, especially because they hold a lot of cash. But a lot of cash holding was never good for stockholders, they should give it back before getting strange ideas on how to spend it.

I don’t criticize management, never do. I just don’t buy if I know that a lot of that precious money I pay land in the coffee pot of the company to spend it on… say bullshit. No CFO, learn your job before I buy your stock!

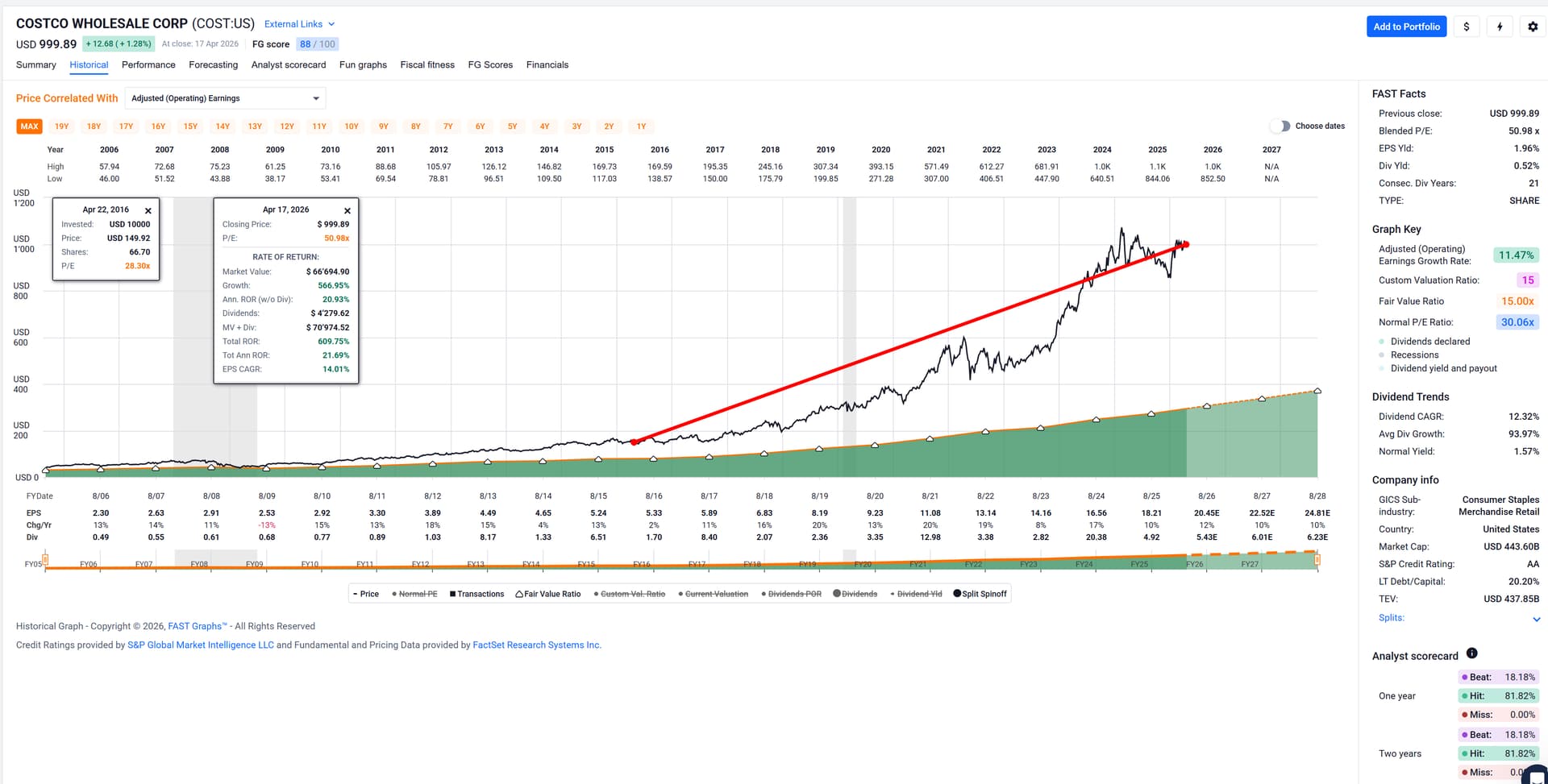

Don’t fret,[1] I believe Phil and I would never buy Costco (at least I would not) at these valuations. They would have been last interesting to me personally in 2008/2009. Of course, I would also have missed out on a nice return compared to buying already overvalued at 28xP/E 10 years ago or so:

Costco has some of its investment fame from Charlie Munger being excited about it. Of course, good ol’ Charlie bought it back in 1997 or so.

I just a couple of days ago came across a clip of a Berkshire Hathaway meeting with a Costco mention from years ago that made me chuckle:

“Charlie and I were on a plane which was hijacked. They asked Charlie about his last wish and he said he wanted to give a speech on the virtues of Costco.

Warren just called and mentioned he would like to have a word with you …

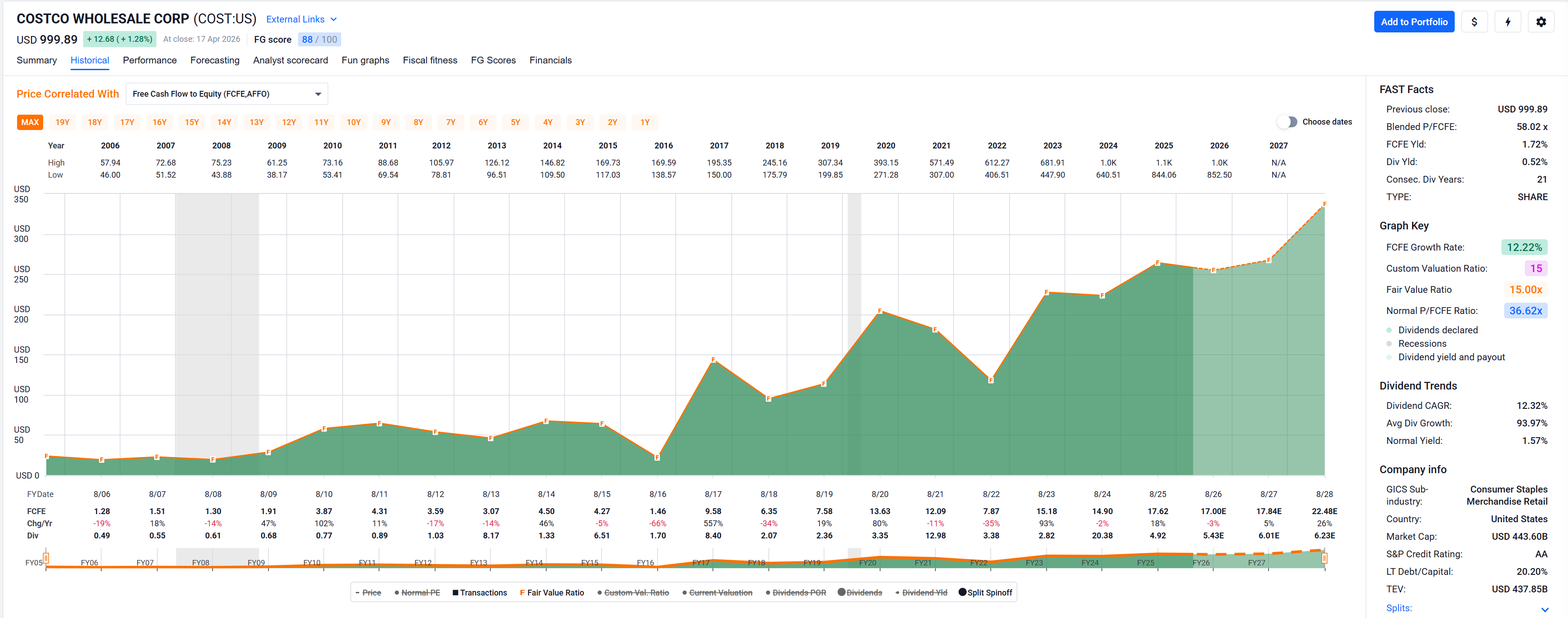

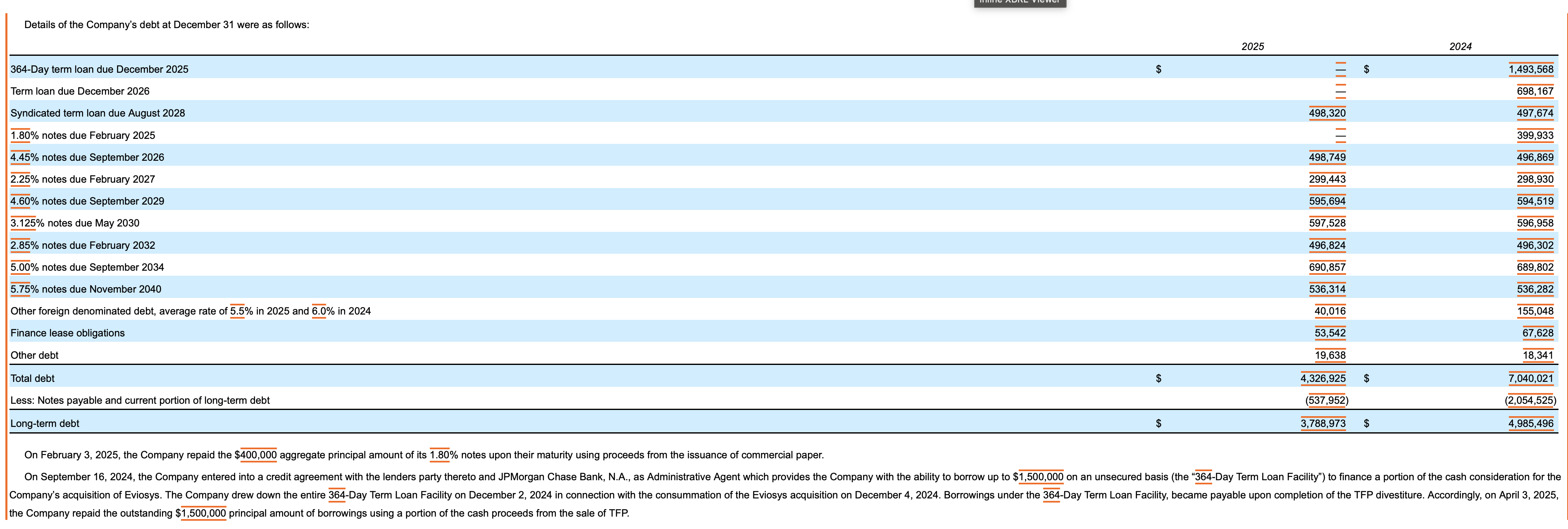

1 Although, maybe feel free to fret a little … . I would say Costco is a great business. Just not investable at its current valuation. Since you like FCF, check out how they’ve been growing FCF:

My first and only contact with Costco was 15 years ago in the UK. A financially savvy colleague told me that we as university staff could sign up to shop in Costco (was not available to most people at the time) and make big savings. I did sign up but never went because it was out of the way, I had no car, and no use for buying mayonnaise by the gallon (I am Greek, I need olive oil by the barrel, not other fats).

Edit: did some reddit Sherlocking out of curiosity, seems “the books are an accountant’s dream” and “all Costcos are packed from open to close since before the pandemic” and “they have fine-tuned the business model of volume while minimising costs”. That “always packed” point has Peter Lynch vibes (Lynch’s anecdote about driving past Dunkin’ Donuts during a recession and always seeing queues outside).

What I always found very interesting about the FASTgraphs process, and noted it in the MP forum, is that it doesn’t care if the business sells plushies or F35s, and the only “understanding” it tries to do is of the fundamentals (unlike say Buffett who, as far as I can claim to understand, when saying “companies he understands” means staying within his circle of competence over and above fundamentals).

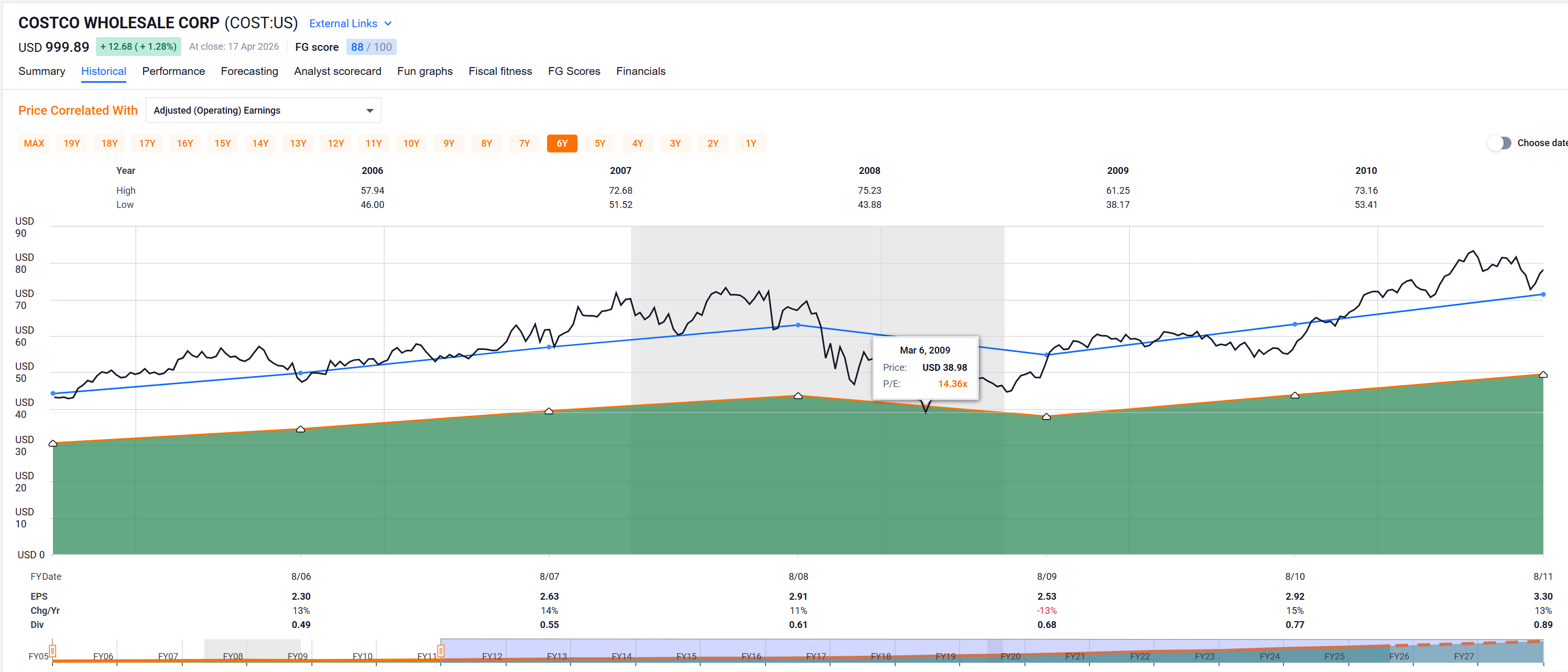

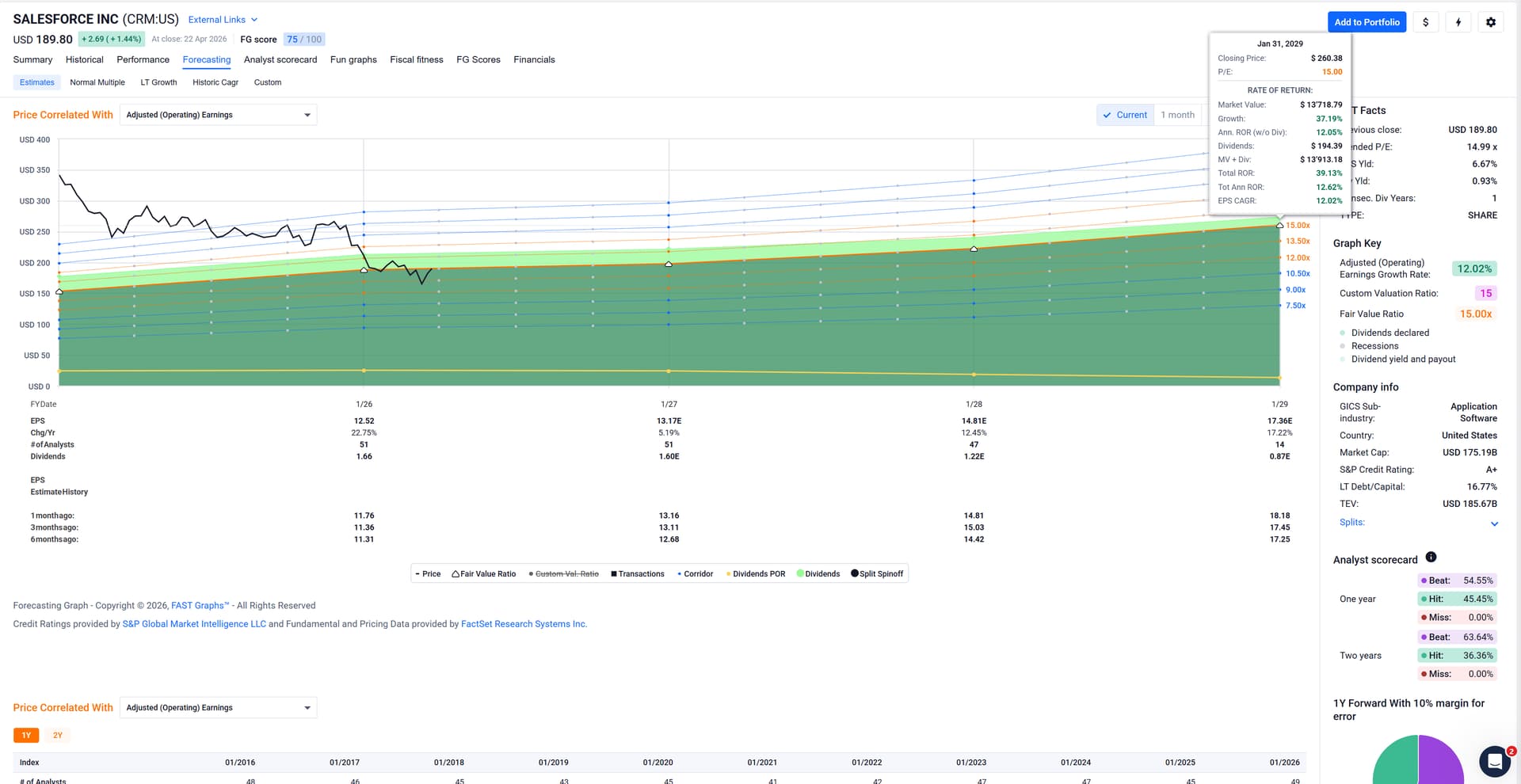

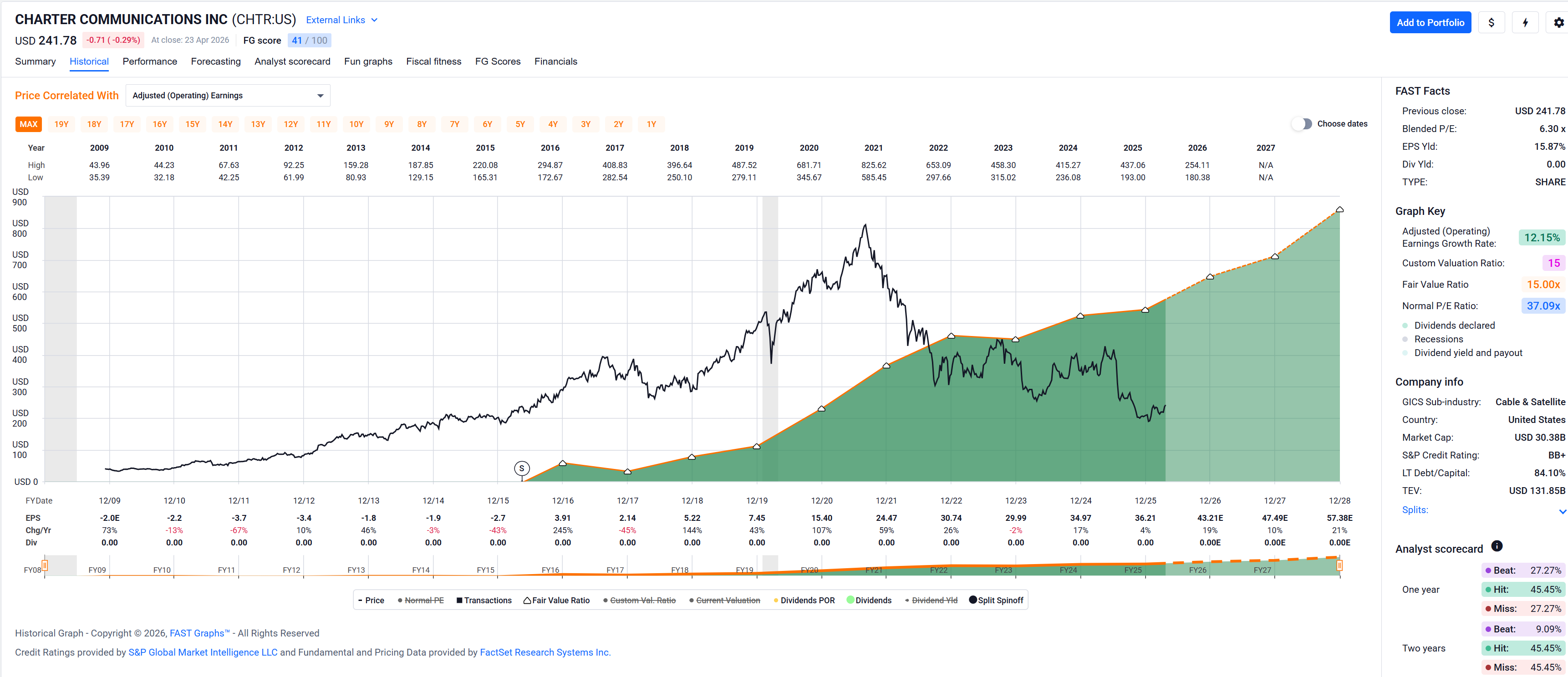

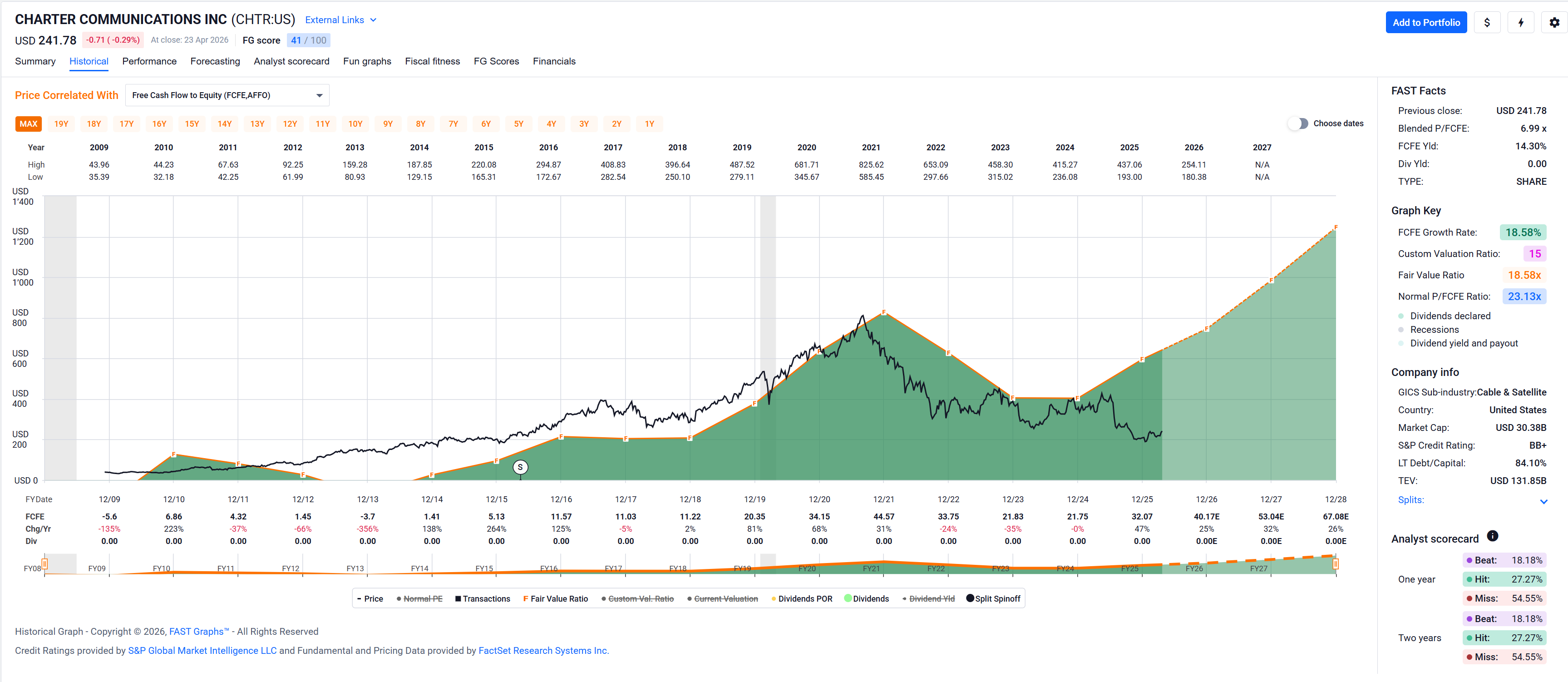

I would note that the clip is from (presumably May) 2011. Looking at FASTgraphs for September 2005 to end of August 2011, the normal P/E for Costco was about 21 or 22, occasionally even hitting 15.

FASTgraph displayed data only goes back 20 years, but Munger joined Costco’s board in 1997 IIRC and I’m sure he bought a bunch of their shares even before that. Even if he bought at a higher PE, I’m pretty sure he didn’t buy at 50 x P/E …

I can’t, really. Seems like a cult (with member cards) to me. Not as extreme as TSLA, but on its way there …

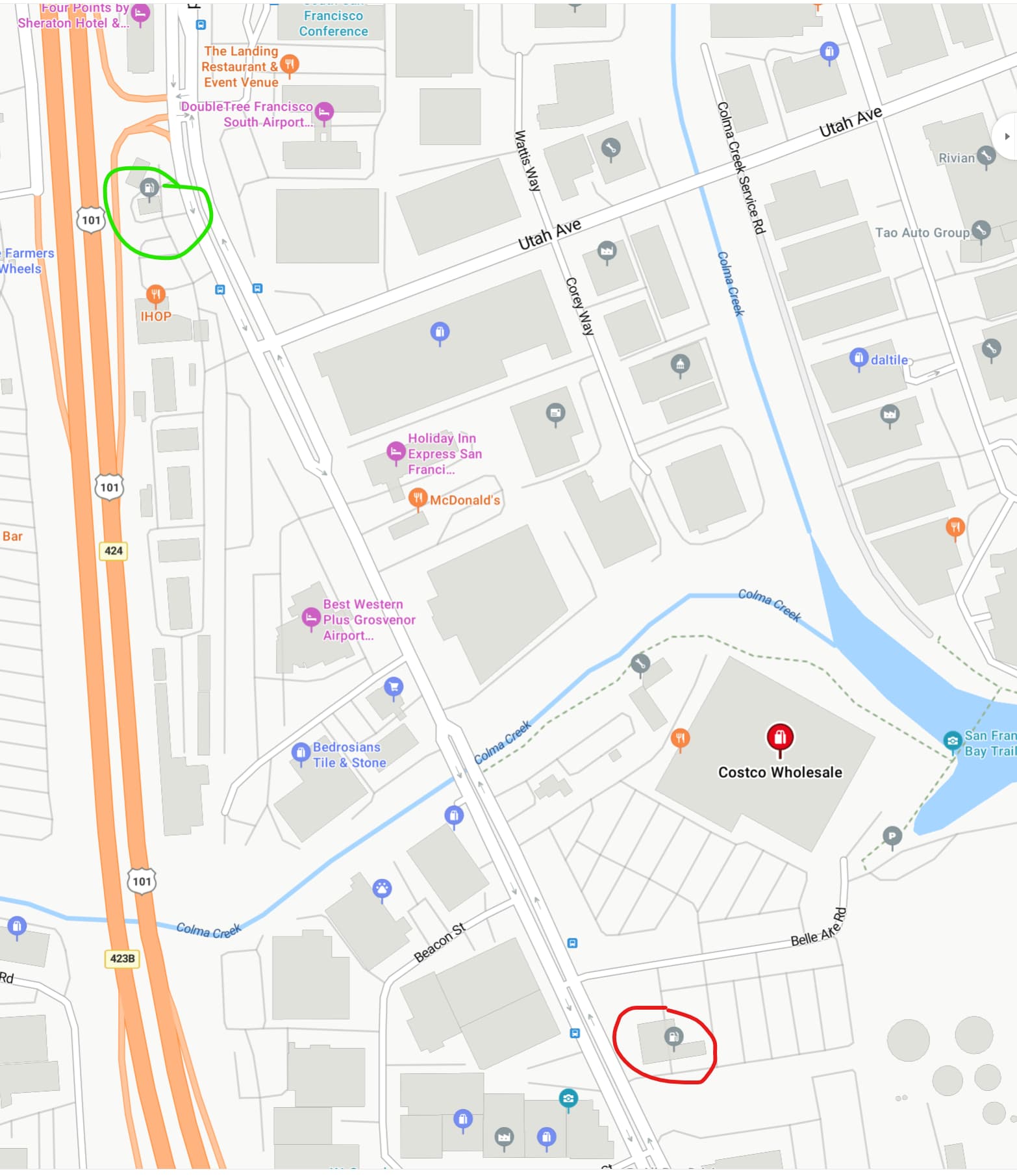

My first, only and last contact with Costco was when returning a rental car at SFO in probably some year between 2005 and 2010 or so. Not having heard of Costco before I saw this large gas station on the South Airport Boulevard and figured I’d fill up the tank of my rental there before handing it back to Hertz at the airport.

Pulled up, waited in line, drove up to the pump, learned that you need a member card, cursed, pulled out and drove up to the next nearby gas station.

As I just looked this up on maps I noticed that I eventually pulled into a Valero gas station. Valero? Valero! Bought them in 2020 and 2021 for an average price of $60, now at $227, paying me about $1500 per year. Dividend raised by about a quarter since my first buy.

Yay!

(I should have bought Costco between 2005 and 2010, though)

I love them as they’ve been raising their dividend by a cent every quarter since Q4 2021. They’re undervalued and their dividend CAGR since I first bought them is about 10%.

They currently pay me about $3000 per year.

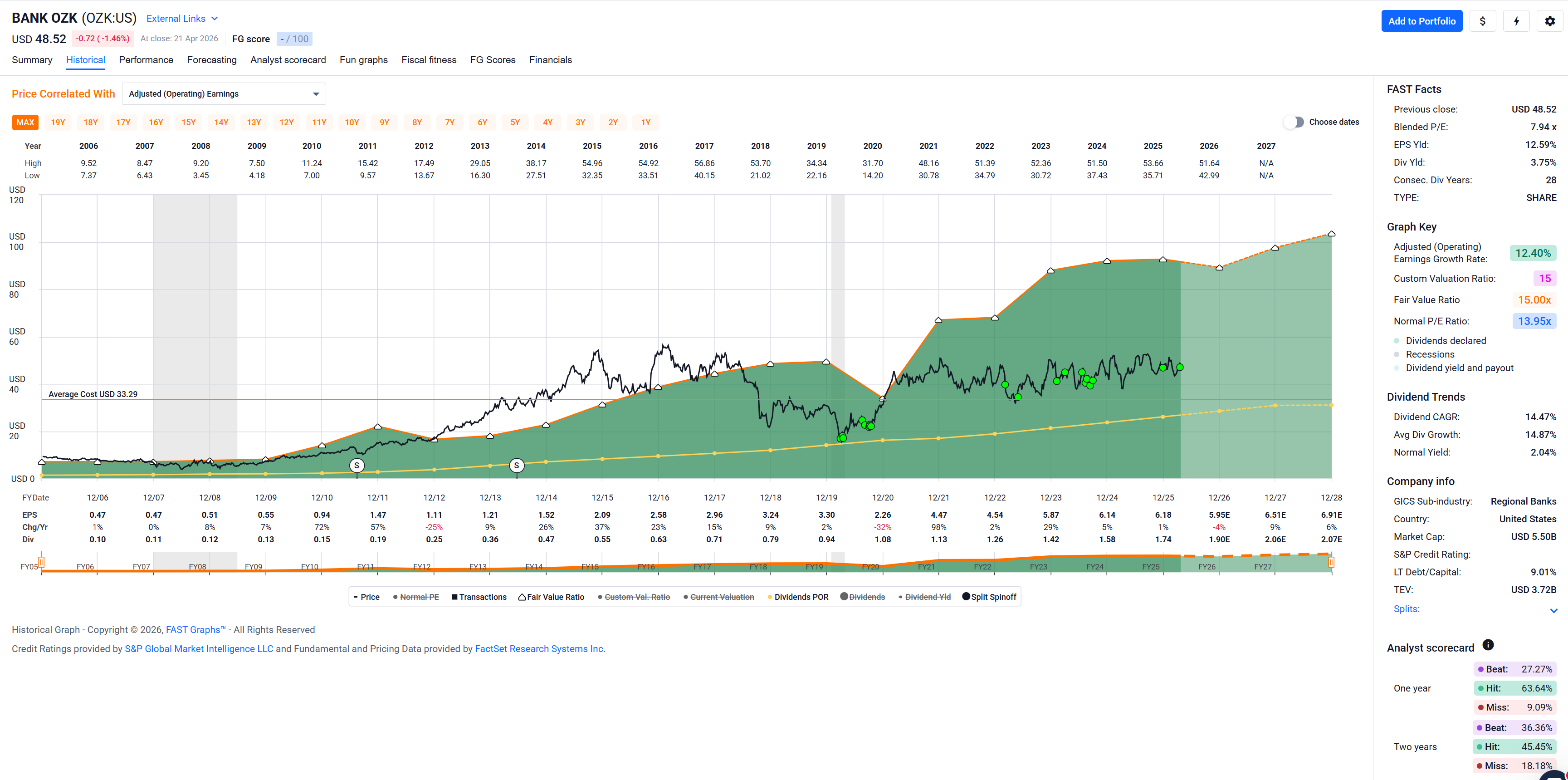

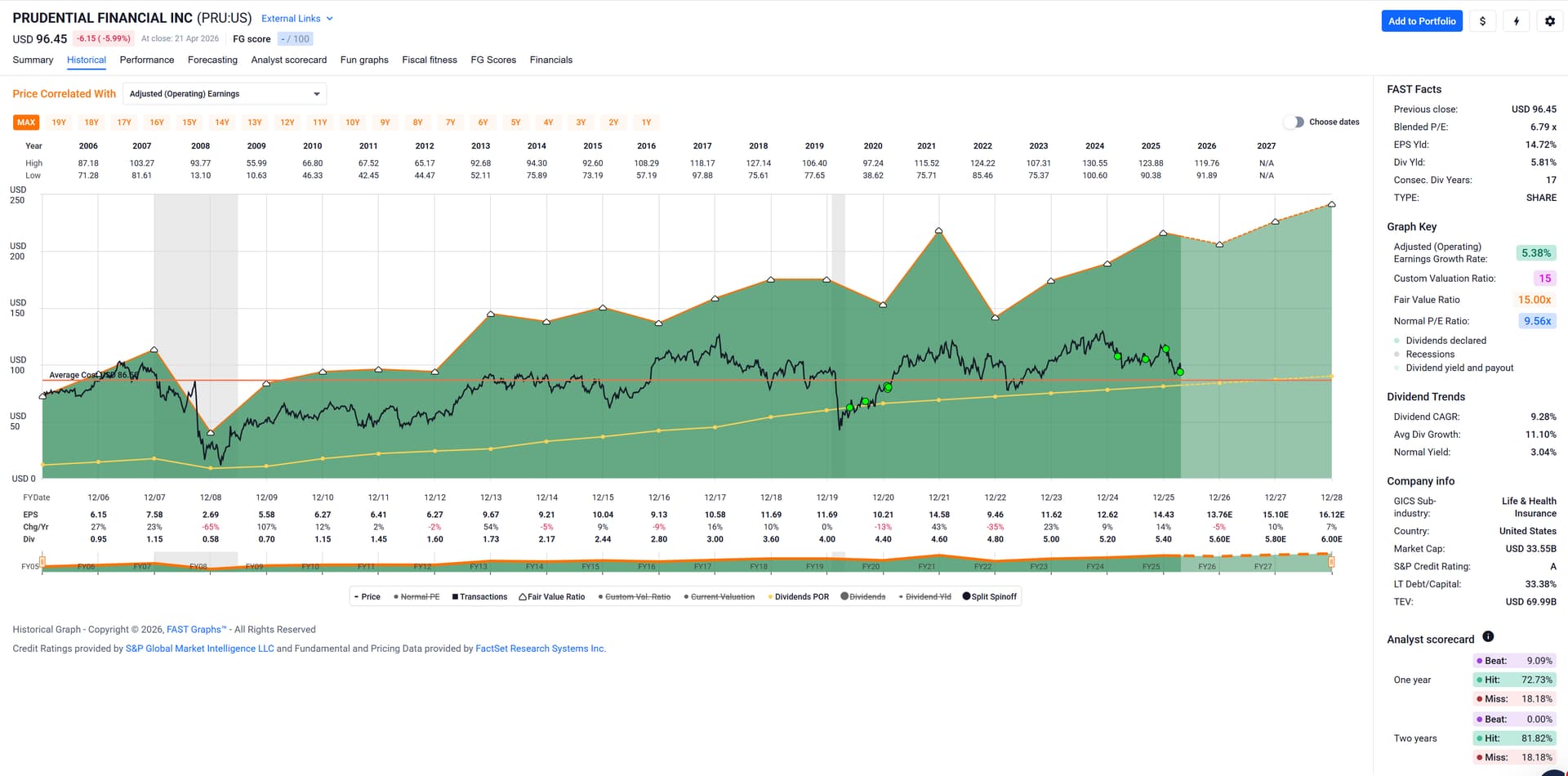

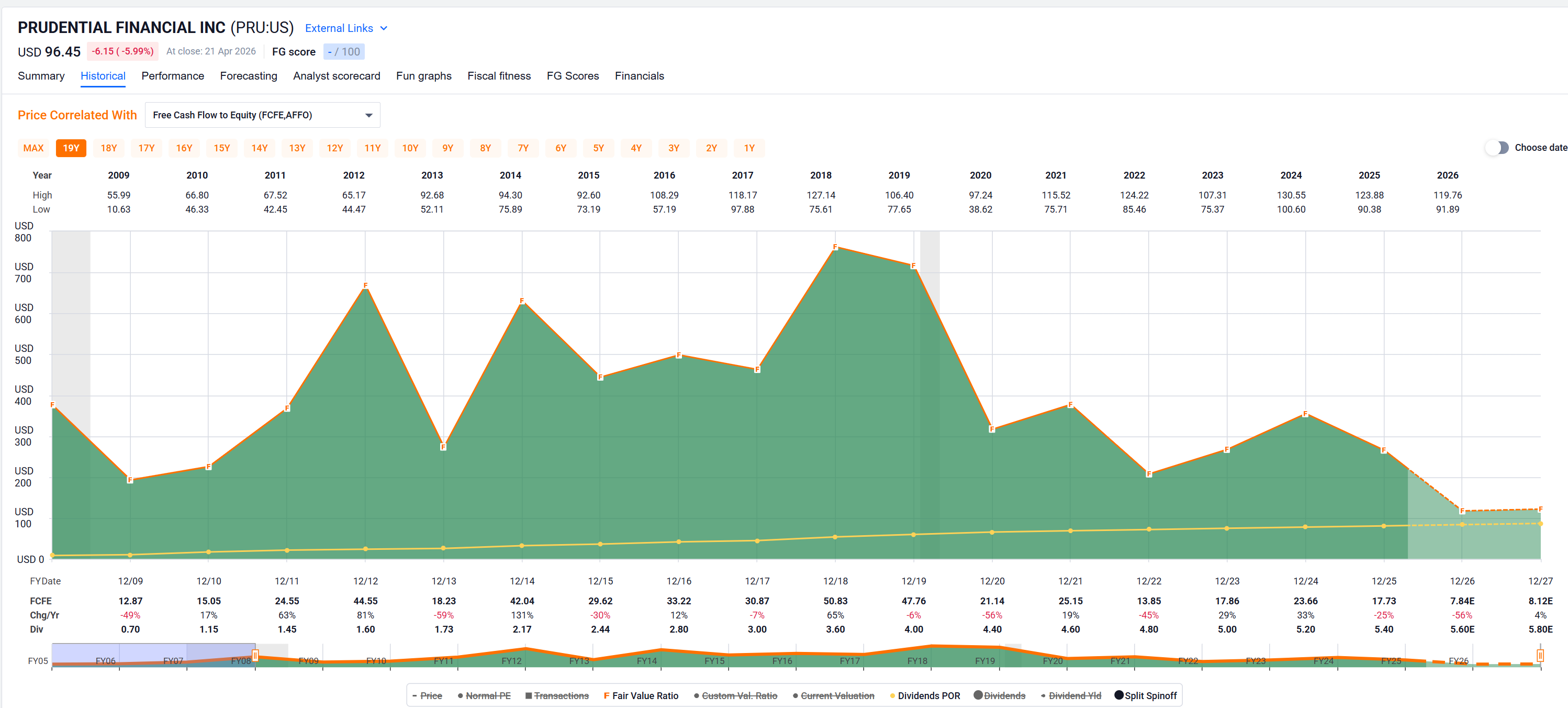

Prudential went down because there was news about them further “voluntarily” suspending sales in one of their divisions in Japan because of some employee misconduct (employees making inappropriate investment solicitations, whatever that means).

Ain’t gonna affect their long-term business, so I bought the dip and increased my position.

Price has been flat since pre GFC, but dividend has been going up steadily since 2008.

They currently pay me about $3250 per year.

Both holdings will require patience for price to appreciate, but I’m in for the dividend and will console myself with the cash flow paid out until they become fairly valued again (if ever).

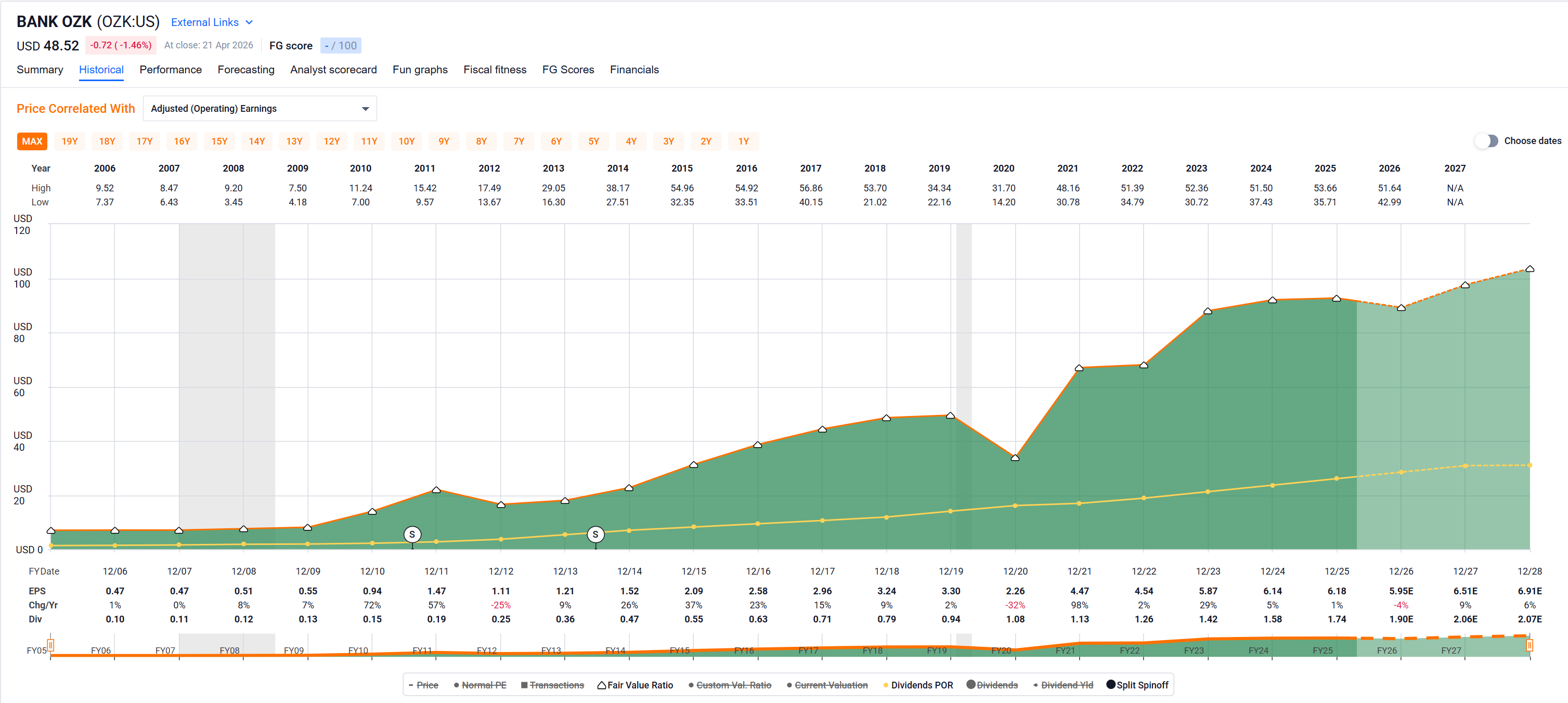

Edit: Was tempted to also add to Unum, but my position there is already overfull (as with Bank OZK and Prudential), but then thought adding to two Financials is enough for today …

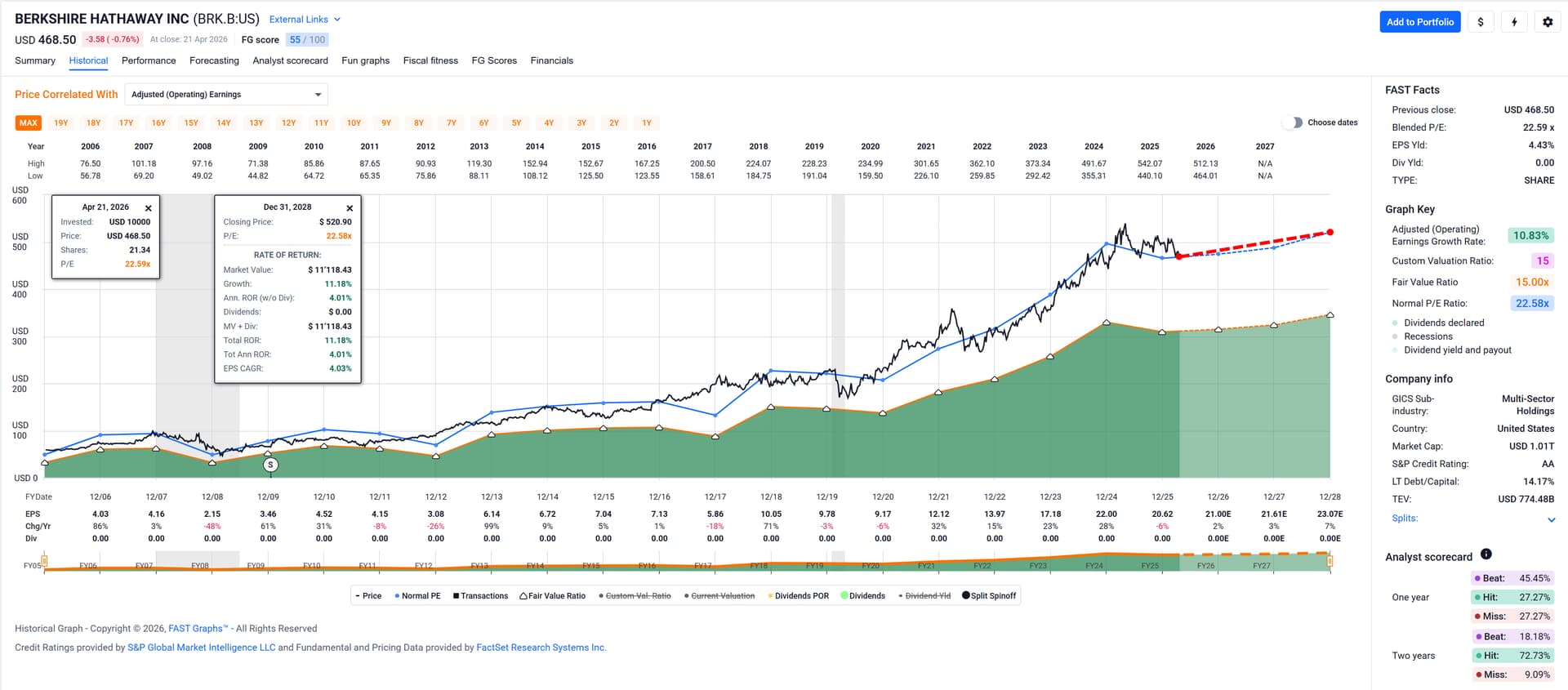

The stock seems to be at its normal valuation (i.e. not cheap) which seems to be the wrong time to buy back stock. Not sure why Abel with his decades of investment experience won’t listen to Goofy (I have been picking stocks since 2019!).

¯\_(ツ)_/¯

Anyway, the stock’s been flat for a while now, and if price remains around its normal multiple, returns will be average or below.

Probably still a good investment if your time horizon is 10+ years. I would probably wait for a dip when Mr. Buffett moves on to greener grass (for me to buy BRK.B into my son’s portfolio – for my own cash flow generating portfolio it’s anyhow not a match as it pays no dividend).

I hold Prudential since a long time for my dividend portfolio. It is on hold at the moment for last quarter numbers… too expensive. Maybe they get cheaper now…

Today in my gambling portfolio a surprise boring stock did rise a lot: HCSG, Health Care Services Group, like 20% today:

Not my pair of shoes for several reasons. I hope you have a plan and know what to do now. Such movements (in both directions) are almost normal in today’s volatile stock market.

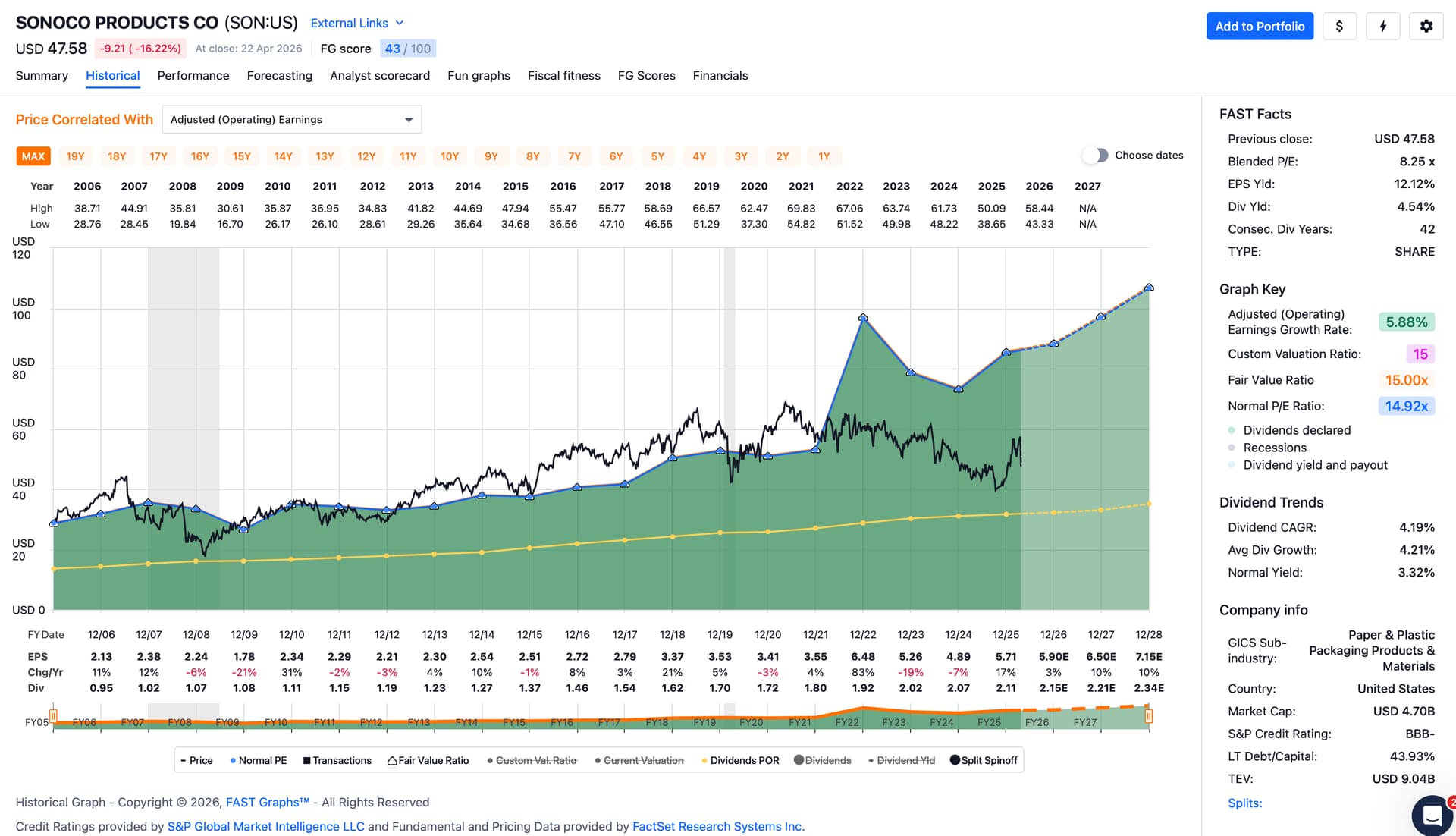

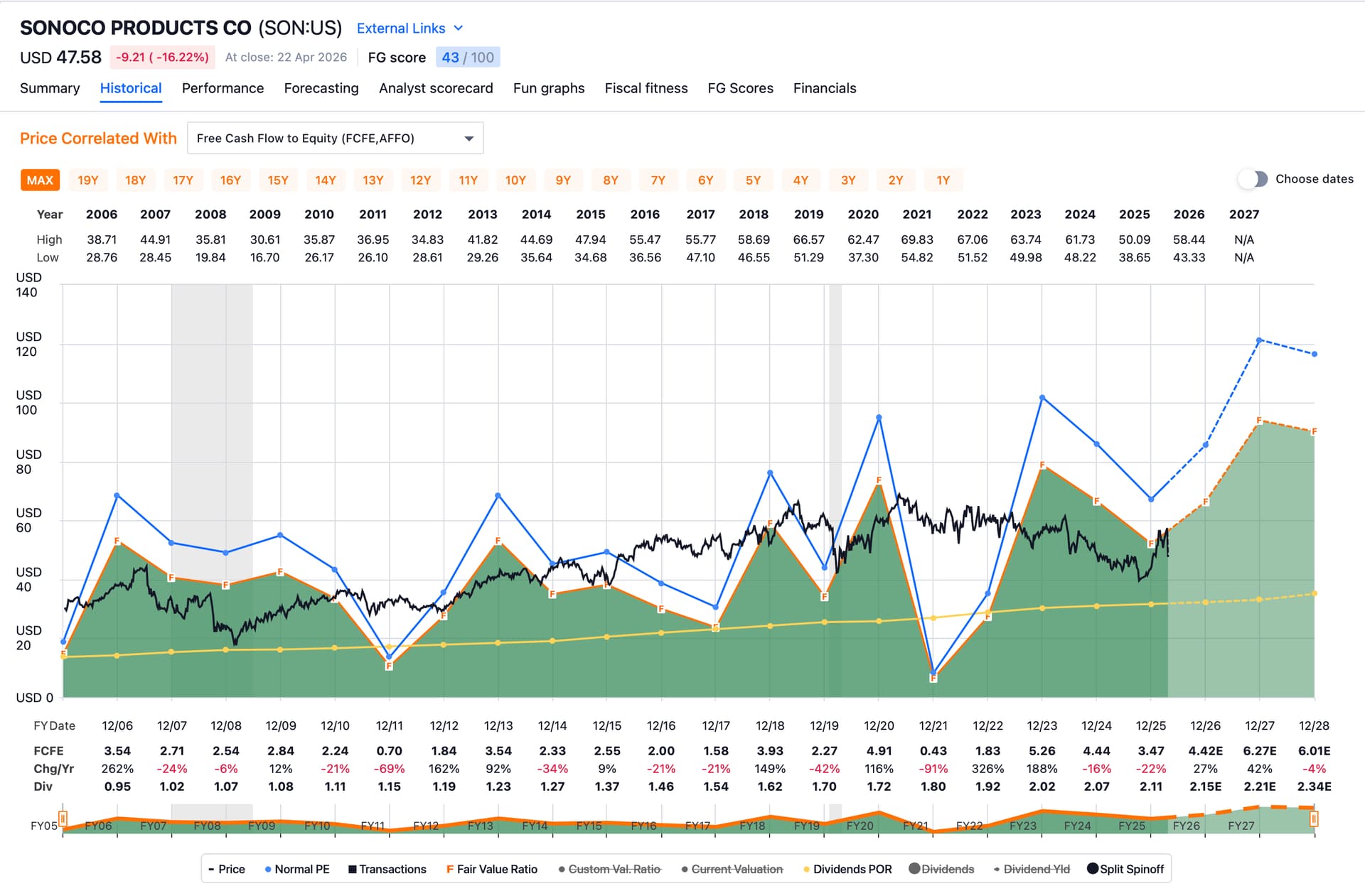

I think they did disappoint with the numbers, negative growth, in addition a (not insured?) fire in one of the plants. That alone would not be a problem for me, but looking at the balance sheet I see a very big goodwill position. It is even bigger than the stockholders equity. In other words: all the stockholders money and a bit more debt was used to buy other companies and this strategy does not seem to work very good (except for the former owners of the bought companies of course).

It looks like management gave weaker yearly guidance on their recent earnings call the day before yesterday and Mr. Market didn’t like that … [$]

If this was a company for my portfolio I probably would have sold a Put wide out of the money for it yesterday. The fear premiums Mr. Market is willing to pay on days when a stock drops 17% are usually really juicy.

Sonoco Products (SON) said it now expects full-year adjusted earnings at the low end of its prior range of $5.80 to $6.20 a share, citing inflationary pressures and weaker demand tied to an uncertain macroeconomic and geopolitical environment.

The company said higher-than-expected inflation is affecting energy, logistics, chemicals, resins and other input costs, while changing market conditions could weigh on industrial and consumer demand.

That softer tone may have overshadowed the quarterly earnings match, helping explain the stock’s after-hours decline.

But it hurts when it should feel good and it feels good when it should hurt.

I passed my Peter Lynch mark which was 29% per year, I am at 30.46% per year since 1.1. 2020. But that is only 6 years and 3 months, Peter did it for 20 years!

@Phil_MCR I hope you have rules in place that tell you what to do with that (and any) position. I am getting old and consult my written rules sometimes, always do so before trading.

Before I came up with the gambling strategy I really tried out some contrarian strategies. That makes sense because I am a contrarian. If you want me to do something, just forbid it!

Em strategies did work, but a lot of risk for not that much performance. Work means they did outperform indices 3 out of 5 years.

But then investing for a living is not a feel-good job. So I did never put a single penny to my contrarian strategy just because my gambling/momentum strategy did and does perform much better.

It’s simply the efficient market doing its thing that it’s best at: pricing things correctly. Something must have changed in their business from yesterday that made the value of their business go down 20% …

/s