The average premium for the mandatory health insurance 2025 increases by 6% to 379.

Find yours here, and if you have cheaper alternatives in your area. There’s no reason not to switch other than keeping your docs in one place, so if you do switch make sure you’ve downloaded what you want to keep.

If your premium doesn’t increase you must cancel by the end of the month, otherwise you have time until November 30. But your old insurer must confirm the switch, so do make sure you have no bills outstanding (not sure at which particular time).

I don’t think people are aware of the cost of operations & hospitals, I had 6 hours of open heart surgery in London, with 8 nights in hospital, not sure the final costs but the bills have exceeded £57,000 to date. With medication & follow up’s the total cost will likely be £60,000-80,000 depending if any small (day case or possibly 1 overnight) for further procedures.

I didn’t realise I’d be paying 5.5k a year. I’ve never used it in 12 years of being in Switzerland, but if something serious happens, I will be glad I have it.

I’m worried about switching now. I have injections to prevent migraines which have to be approved yearly by the insurance. I don’t know how switching works with that. What if I switch, the Dr writes to new insurance for approval, new insurance says no - then I’m screwed.

I’m in the same boat, I’ll see what the new premiums are compared to other insurance companies and hope that my current one is competitive before I go down that rabbit hole.

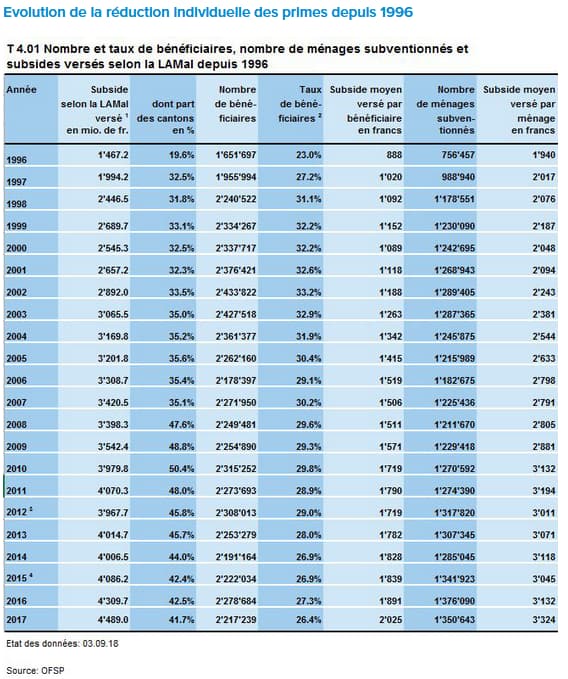

Considering nearly a third of the population in Switzerland (27% in 2019) gets a subsidy to cover the insurance premiums, this is an increase in taxes for everyone.

Evolution of subsidies from 1996 to 2017, average subsidy per person in 2017 around 2k francs per year.

So, the system is broken when 1/3 of the population cannot afford the “mandatory” health insurance. Subsidies are a patch that avoid recognizing the challenge, I guess we’ll see VAT 9%, VAT 10%…

From what I understand the mandatory insurance leaves next to no room for leniency.

With that said, nothing keeps you from enquiring if your prescription is covered, from you getting a Kostengursprache or Garantie de paiement. This happens anyway in advance of a surgery, hospital stay, large treatment, etc.

Perhaps this needs to be done by your doc because they’re intended for the facility bearing the cost so they know they’ll get paid, but you can still enquire.

Where did you get that information from?

Cancellation for mandatory health insurance must be with the insurer November 30. And it’s not the old insurer who must confirm but the new one must confirm to the old one, they usually do that directly.

One cancel mandatory health insurance every year if wanted, whether it increases or not. Also, do you have the information from your insurance yet how much you’ll pay next year? I definitely don’t.

For additional health insurance if one wants to cancel it needs to arrive September 30th as usually the cancellation period is 3 months before end of year.

There are no guarantees, though if you get a cheaper offer that you are considering, you may wish to ask in advance and maybe you get an answer in time. Personally I have changed several times and had no problems with costs that are to some extent discretionary - the regulations regarding this seem to be unclear.

The system is not broken but it is under pressure. It underlines that not all in Switzerland are earning that well and it is a fair system -if you earn less, you pay less and yes, your income has to be quite low to get a subsidy - I am quite happy to be just above the threshold.

There’s no point in doing anything until I’ve had a chance to compare prices. My current insurer is pretty cheap already and I wouldn’t consider changing unless one of the others (other than Assura) was significantly cheaper.

Because Assura require payment upfront and claim for reimbursement and they are slow to pay up.

This treatment costs 1500chf per month so I’d rather the pharmacy billed the insurance directly.

Ah. OK. I’m with Assura, but never claimed anything in the last decade. I just had costs due to my recent illness and the pharmacy charged Assura directly, but of course they billed it right back to me as I have a 2’500chf franchise.

But I also heard bad things about them being reluctant payers.

Assura is known to be really terrible at all admin stuff. Requires up payment and also trigger easy in sending you to Poursuites/Betreibung as soon as a disagreement arises.

In the UK 50% of families get at least 50% of their income from tax credits or benefits, so just 27% of the population getting subsidies would not be unusual elsewhere.