If only the inflation calculations included health insurance premiums. Switzerland has understated actual inflation for decades using tricks like this.

3 Likes

Same with unemployment rate. People dropping out of RAV and changing to social security (still or even more desperately looking for a job) are no longer mentioned.

1 Like

It’s not just your income that has to be low; you need to have no savings or investments. It’s a system that works well for people who save nothing and spend everything they earn, hardly good housekeeping I would argue.

1 Like

The CPI calculation includes hospital / doctor’s bills (regardless if paid by the health insurance or the patient) and admin costs, so increases in all these prices are directly captured in the CPI. But the increase in basic insurance premiums is by a large part due to more medical services being consumed (as premiums are wholly used for health care, no profit allowed).

But this is not inflation.

By analogy, my electricity bill doubled when I bought an e-car, since the number of kwh I consumed doubled.

Equally, this is not really inflation, if the price per kWh remained the same. What would happen is if this trend continues, the CPI basket of prices would place a higher weight in this category, meaning that households spend a larger proportion of their expenditure on this item.

The Swiss statistics office has a detailed explanation of CPI inflation and Basic Healthcare, in English even :

https://www.bfs.admin.ch/bfs/en/home/statistics/prices/surveys/hvpi/hvpi.assetdetail.20984928.html

1 Like

I have control over my electricity consumption. I have no control over my health care costs.

Not true, if you are sick and do not visit a doctor then you have no additional care costs to pay.

I’ve been talking about the increases in health insurance premiums, which I have little say.

That’s a bet that sometimes pays. Some times it’s worth to endure a bit of discomfort and the body recovers. Other times, waiting only makes things worse.

All we can do is try to make the best choice constrained by circumstances, no more.

2 Likes

How about:

If you are not sick and do not visit a doctor then you have no additional care costs to pay.

And there’s a lot you can do to mitigate both the chance of being ill, and the severity of some illnesses or conditions by lifestyle choices*

So, to some extent you are able to be in control of your healthcare costs.

*But not all, obviously.

Yes, it is (although not officially, as discussed as this is not included in the CPI). Swiss health insurance premiums will rise by an average of 6% in 2025, irrelevant whether you use it more, less or the same. The question is not whether insurers are making a profit on the premium, but how big is the price increase driven by he underlaying services and products.

For adults, the premium will rise by CHF25.30 to CHF449.20 in 2025. New medicines and treatment options as well as rising demand for services have led to this cost surge

I recommend you read the explanation in my link by the Swiss statistical service.

Plus you said it ; premiums are higher because they are linked (used for paying) for services whose prices are surging. Since the CPI already includes these services, it is already included, and it would be double-counting if we add the premiums in the calculation.

What you are describing is an increase in the cost of living. Inflation is not the only reason that we must pay more for something each year. Inflation only accounts for the increase in prices, in a quite strict sense… The cost of living rises due to other reasons, including change of habits and advances in technology.

I am not advocating for this to be part of CPI, I was correcting your erroneous statement that this is not inflation, when it is inflation.

On a slightly different note, imagine Novartis launches a new anti-inflammatory drug, which is, say, 20% more expensive than Voltaren and this is part of the new medicines available as part of your insurance, is this inflation?

Reading your linked article and other media, it’s interesting to note that as there is a move from inpatient to outpatient treatment (partly due to advances in medical treatments), all these costs are born by the compulsory insurance as only this is allowed for outpatient treatment.

People with supplementary insurance have more treatments (and sometimes unnecessary ones) than those with only basic but a percentage of these costs are covered by basic insurance so all are paying for this even though those with basic get no benefit.

More medicines are coming on to the market - these can be expensive. Again, all will be paying for these to an extent even if they only available to those on supplementary insurance.

People are living longer.

Hospitals here generally do not make a profit. There is an urge to push for extra treatments and get bodies in beds.

Again, we all pay a percentage of this.

1 Like

Exactly! I am not commenting whether this is right, wrong, fair or unfair, but that the premiums increase for ALL, irrelevant of how much an individual is using said insurance. Thus, the comparison with fixed price of kWh, but increased use of electricity is inadequate. Its more adequate to say “we increase the price of kWh, because more of you are using more electricity and this will inevitably increase the price even for those who use the same or less”

p.s. We as a family and luckily are quite happy with the medical services we get so I am not complaining at all, in fact, I find the Swiss model one of the better ones out there.

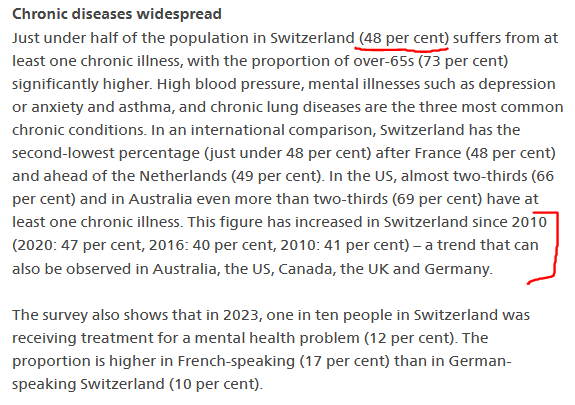

The population changed. Back in 2016, 40% of the population had at least 1 chronic illness. By 2023, that had gone up to 48%. I can’t understand how this changed sooooo fast.

It would be interesting to see the historical evolution of the “fraction of the population that uses health insurance above deductible”. If 1 chronic illness is a proxy for this value, we’re screwed. But, at some point the fraction of the population that uses health insurance above deductible should stabilize and no more increases.

I SUSPECT that this is due to the increased median age. In 2015 if was 41, now its 43. If this is the driver, in 2035 the median will be 46, thus we can expect more premium increases.

1 Like

Way too expensive for the services you get, unless you need a surgery or something like that. There’s this myth that the Swiss health system is very good, but talking with other people it’s very low in prevention for instance.

1 Like

That’s interesting. That may explain a bit the increase in chronic illness.

But, median age cannot go up forever. It should stabilize at some point.

Maybe, what is your country of comparison? Honestly, I haven’t spent much time comparing quality of healthcare vs costs in CH vs other countries as for us this is a given. We are here :).

Btw, preventative for me has always been much more an individual responsibility rather than a systemic question.

Agree. The question is when ![]() If the link I posted is to be trusted, it seems that it does indeed stabilize at around 47 from 2040 onwards all the way to 2100

If the link I posted is to be trusted, it seems that it does indeed stabilize at around 47 from 2040 onwards all the way to 2100 ![]()

It has it’s flaws. From a 2022 study for the WEF (pdf):

… many services covered by SHI may potentially have little scientifically proven clinical value [4] or may have more cost-effective alternatives. This potential inefficiency is a shortcoming of the coverage system that jeopardises long-term financial sustainability

There is also a lack of transparency in the system - partly due to the Federalist system.

A lack of digital data controls communication and inter-cantonal cooperation means resources cannot be shared and are therefore duplicated.

Underuse of generics and bio-equivalents compared with other countries is another factor creating higher costs.

I read a report elsewhere that although the standard of Swiss healthcare is generally excellent (familywise is has been shockingly incompetent in a few cases), it is one of the most inefficient services worldwide.

Perhaps if these inefficiencies were addressed (but not by public vote*), premiums rises wouldn’t need to be so frequent.

*historically, in more than one public vote, the efficient option has not been chosen.

1 Like