It’s clearly anchored to its fundamentals …

Edit:

Continuing to cut some flowers to soon buy some more weed: sold some more Cummins today …

Still holding on to a fair amount of CMI, but the company yielding just a little of 1% in dividends isn’t my preferred setup.

They’re growing, all right, and that’s great, but better to take a few chips off the table and buy some dividend shitco instead. ![]()

Cummins is a nice cyclic stock. I started buying 2015 at 85 something. Then I continued buying until 2022, last buy at 205.

Then my market dividend concept made my capt’n tell me to sell at 269, 472 and 616. Dividend may not be great but market dividend sure is!

Enbridge is another one in my portfolio that is slowly getting over its skis valuation wise …

… but its dividend yield is still nice, so I’ll hold on to it. Current oil market drama probably also provides a nice tailwind for price appreciation.

Edit:

Iron Mountain is on the sell watchlist, too.

AI hype around data centers driving some earnings, but mostly price. Divvie yield still acceptable, though.

It’s just a REIT, for heaven’s sake!

Edit 2:

And then there’s The Coca Cola Company …

Perennially overvalued and even in recessions – basically the only buying opportunities – you have to buy them above fair value.

The joy I get out of it: it pays me more in dividends than I pay for any of their products. So there’s that.

I mean, looking at this graph, it’s no wonder Buffett calls it the best company in the world.

Came across Xpel today (via FASTgraphs on Twitter).

Total annual rate of return since 2018: 50%

No dividend, alas, but this thing looks like a monster. ![]()

Maybe something for my son’s portfolio …

![]() And easily beating Monster over the same period of time when MNST has been a little monster itself …

And easily beating Monster over the same period of time when MNST has been a little monster itself …

Have had a small holding for years. Paid 4 K and now it worth about 10 K more. They just got into bed with Apple yesterday. But its not the first time.

Next up (in the series of going through my stock picks):

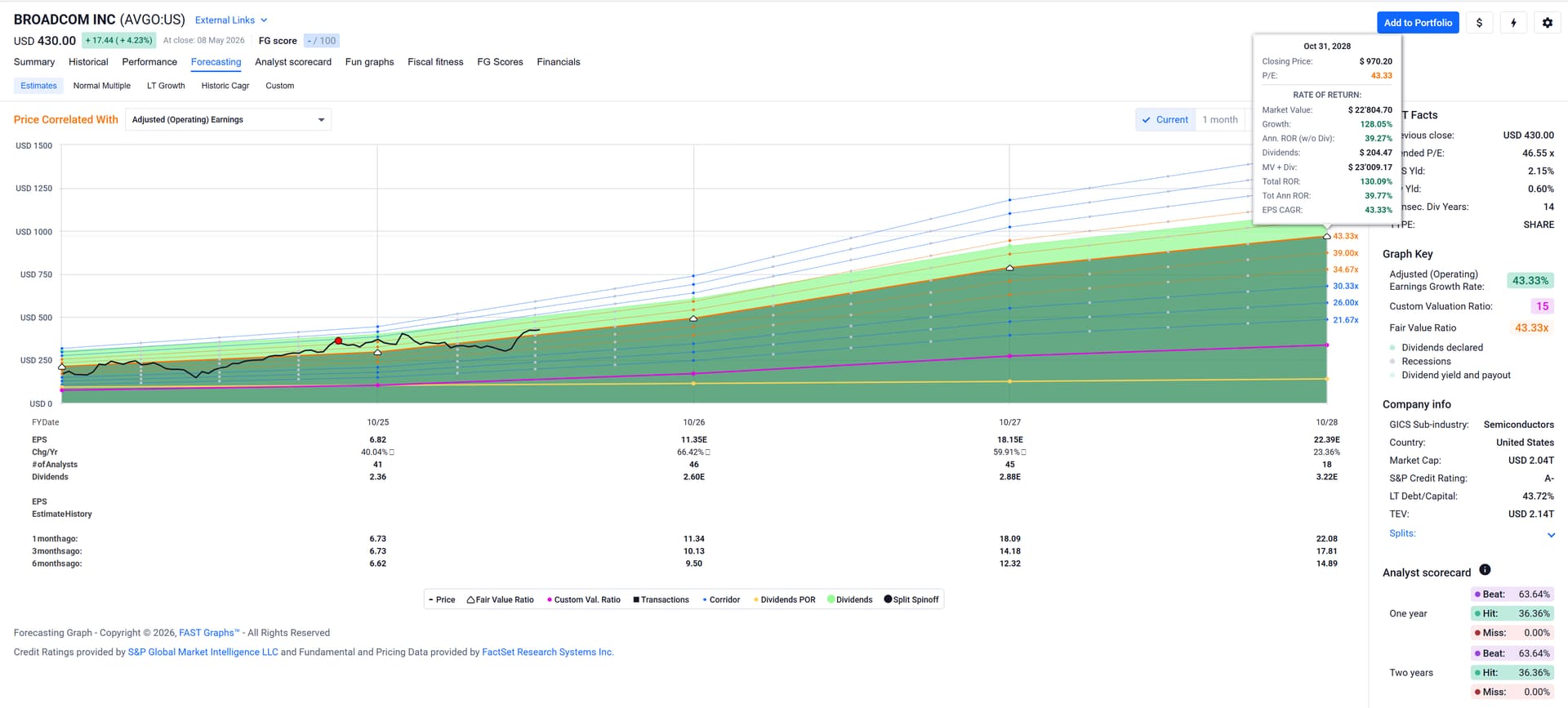

Broadcom Inc. is a global technology company, which designs, develops, and supplies semiconductors and infrastructure software solutions. For company profile details see footnote.[1]

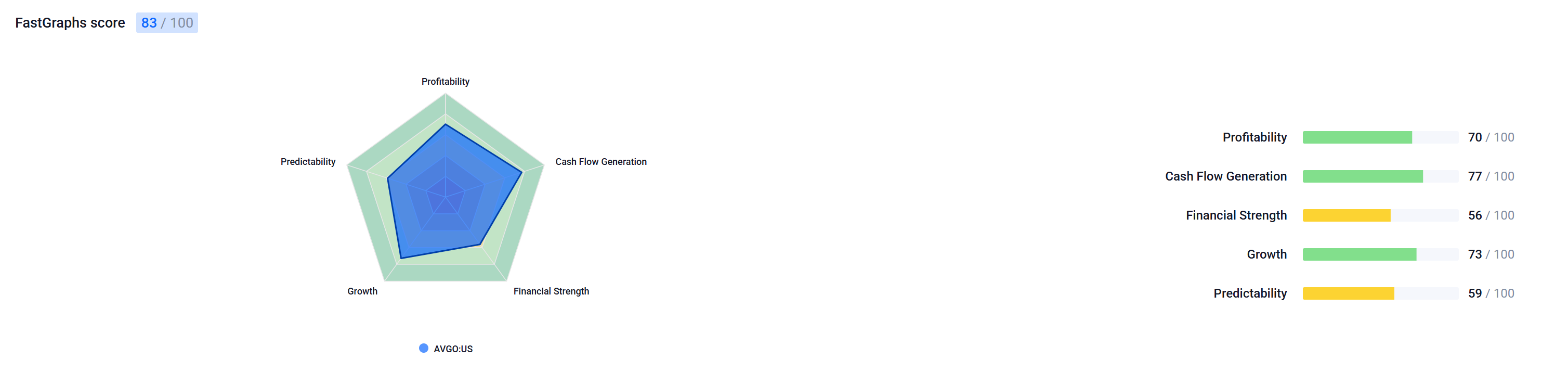

FASTgraphs score:

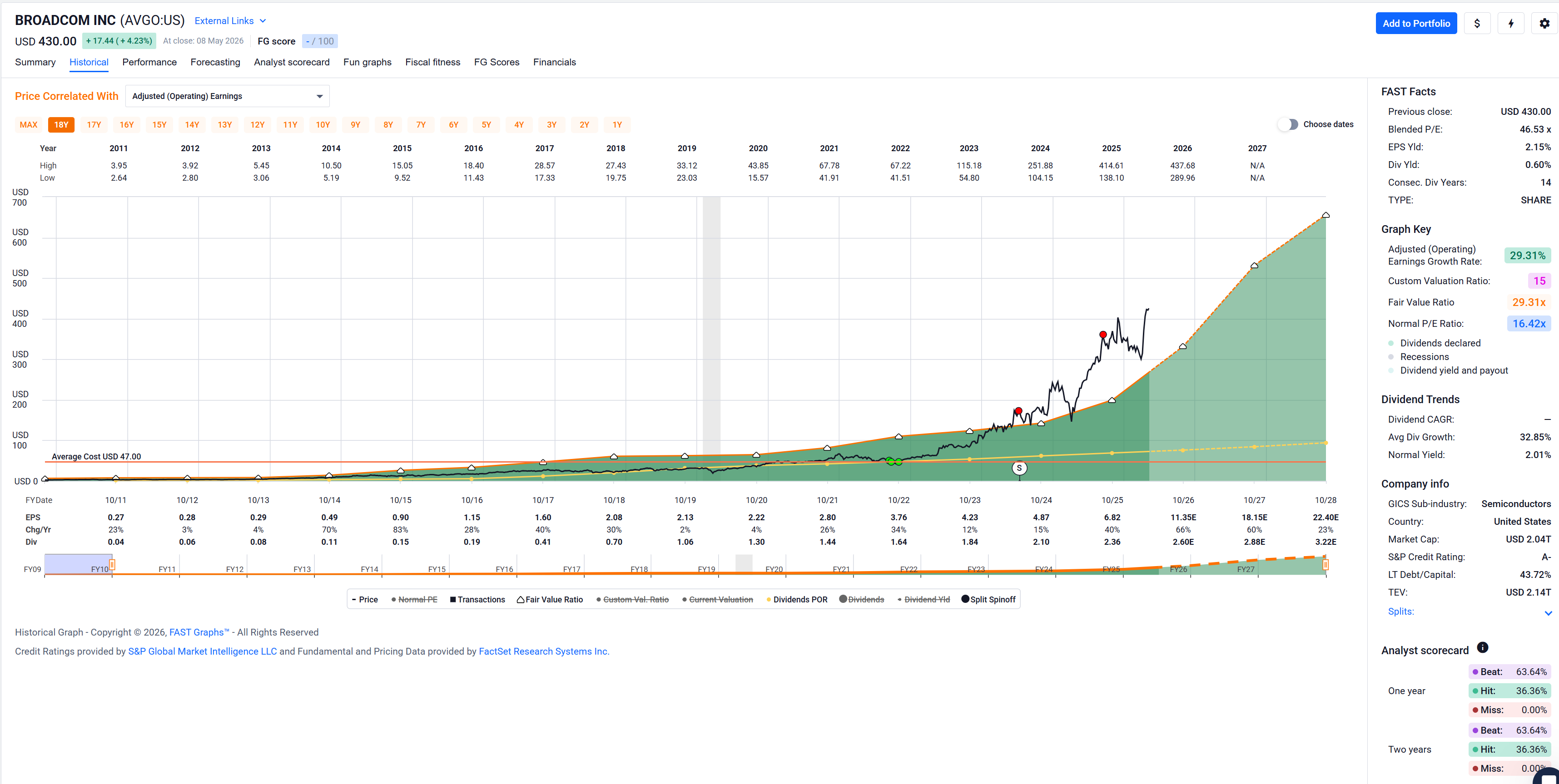

Historical earnings graph, price chart, etc:

Earnings growing at about 30% p.a., equally impressive dividend CAGR, initiated a dividend in 2011 and have been growing it since.

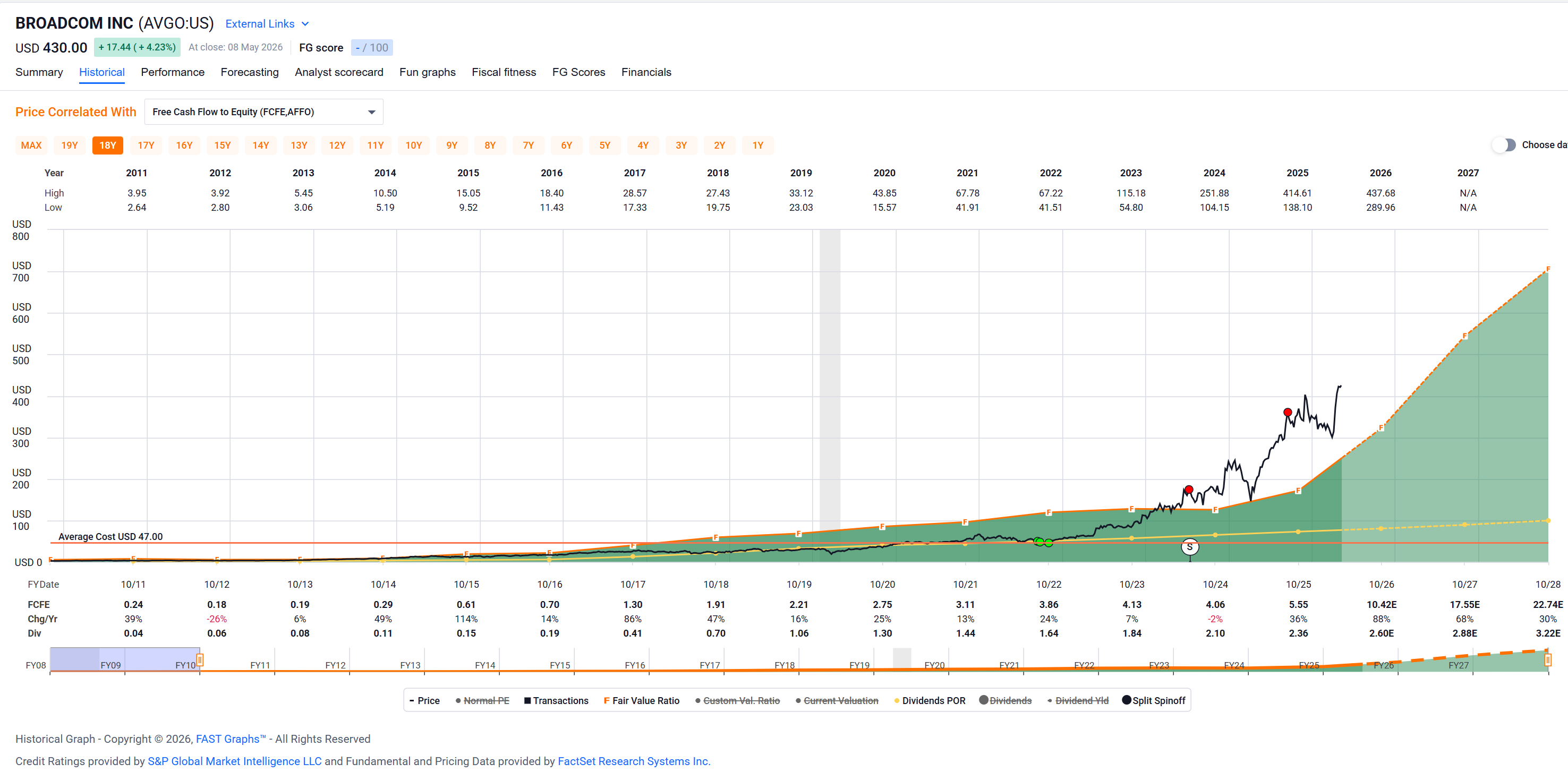

Free Cash Flow looks just as impressive:

Moderate debt, excellent A- S&P credit rating. Never misses analysts’ forecast for earnings.

Forecasting earnings:

Their earnings expectations keep going up bigly.

They’re actually only a little overvalued if they can keep up their earnings growth. But that dividend yield … man. I’ll probably hold on to them regardless unless the AI bubble[2] starts to deflate.

Very strong company in all aspects (except dividend yield).

AVGO is a hold for now in my portfolio.

[1]

Broadcom Inc. is a global technology company, which designs, develops, and supplies semiconductors and infrastructure software solutions. It operates through the Semiconductor Solutions and Infrastructure Software segments. The Semiconductor Solutions segment refers to product lines and intellectual property licensing. The Infrastructure Software segment relates to mainframe, distributed and cyber security solutions, and fibre channel storage area networking business. The company was founded in 1961 and is headquartered in Palo Alto, CA.

Information Technology>Semiconductors & Semiconductor Equipment>Semiconductors & Semiconductor Equipment>Semiconductors

2 “A bubble is a bull market in which you don’t have a position.”

— Eddy Elfenbein

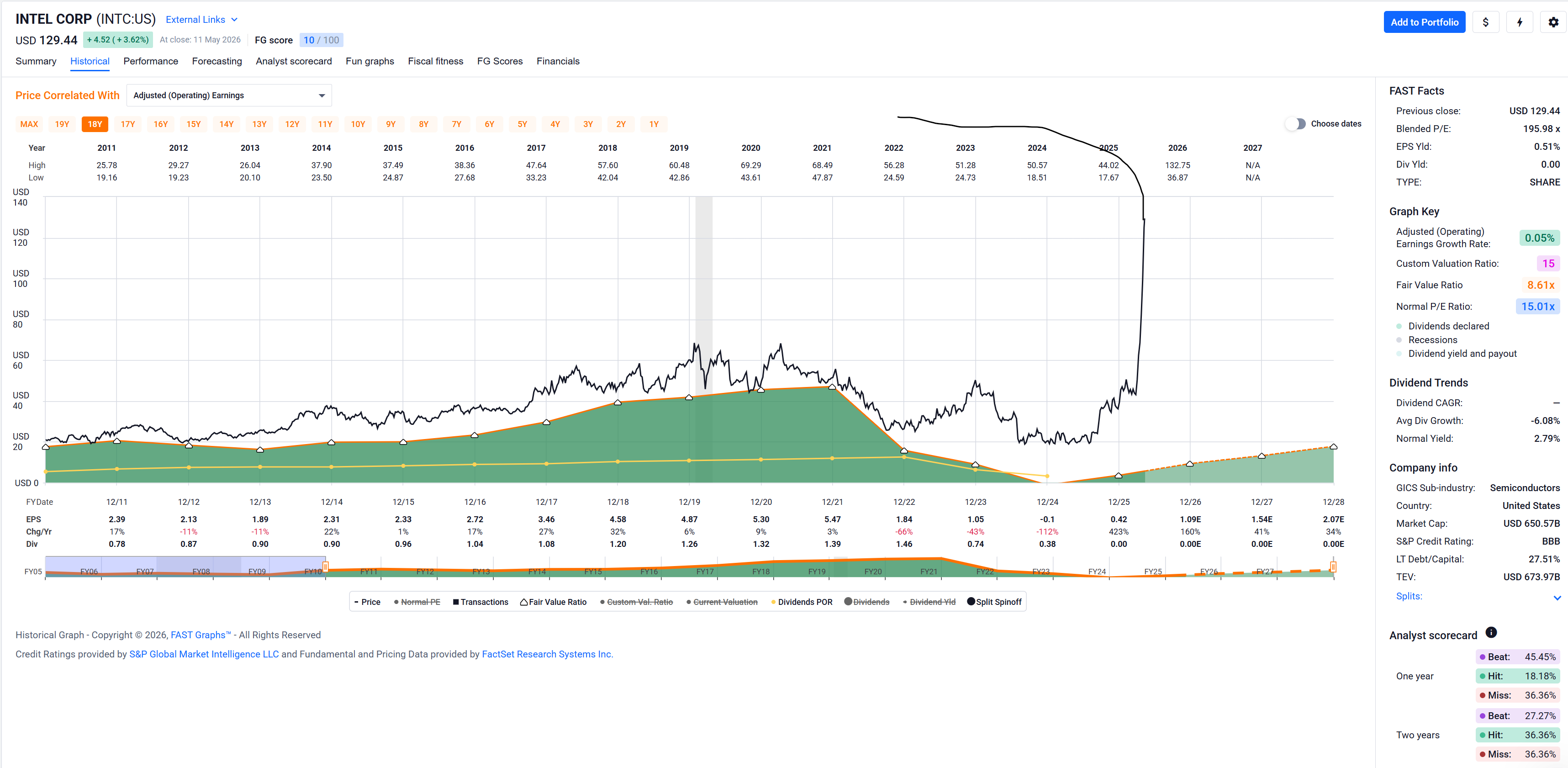

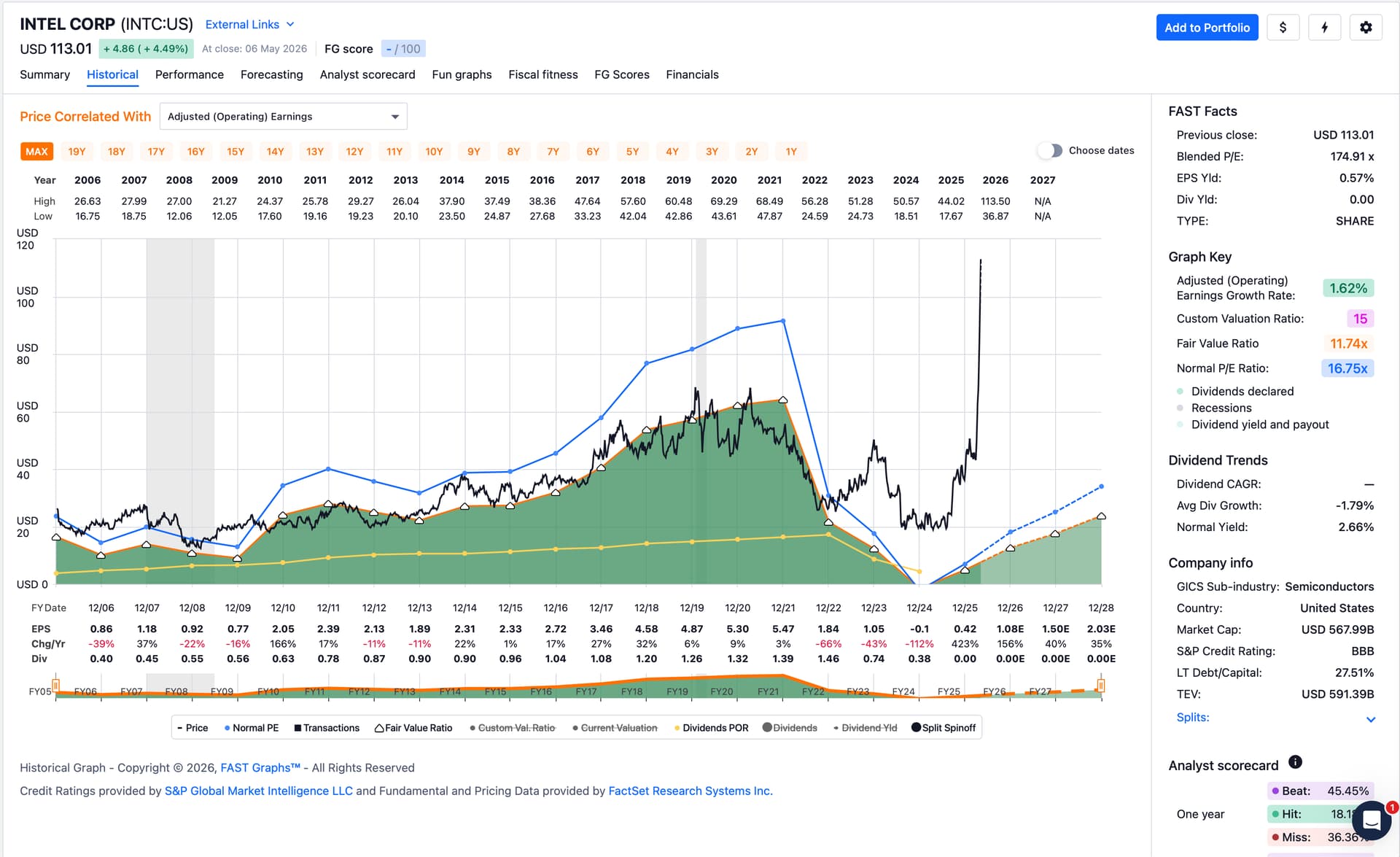

I hold broadcom since 12 years, another of our interfaces.

It is on “sell” because of the value, enterprise value divided by free cash flow is around 76 for the year and 64 for the last quarter. OK, the direction is good but my limit there is 34…

I think this is the single stock that gave me most market dividends. And the decision to get out of Spain was more than good. But it is too expensive. What does not mean that it cannot get much much more expensive!

It has to slip to the lower half of my holdings in momentum, then I sell. Otherwise I just wait and enjoy the price performance.

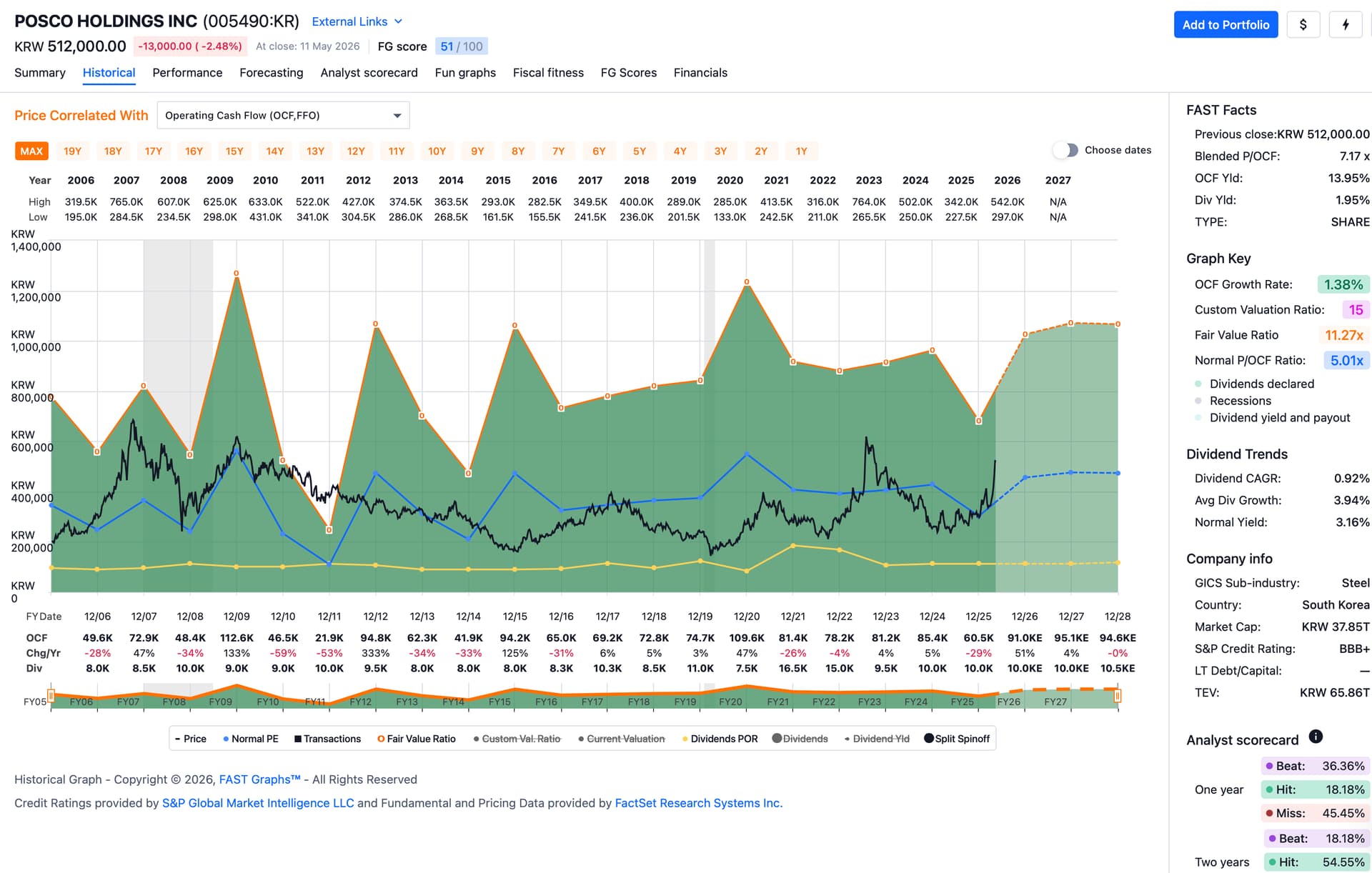

Some action in my gambling portfolio today:

Sold Dollar Tree with a little gain and Strattec with a little loss. The money was used to buy Korean steel giant Posco.

@cubanpete I think you once posted a link for people who are interested in following your portfolio. Could you post this link again? Thanks!

Actually it was a link to a german forum where I think I have seen you. I post more or less the same like here, just in German.

Thanks. Yes, I spent some time on that German forum, but much prefer the conversional style in this forum ![]()

The link in the first post of that forum thread represented your portfolio five years ago. So I probably wrongly thought that that link would represent your updated and current portfolio.

Looks like they’re already above their historic normal valuation, but history also shows that they can go way above their normal valuation occasionally.

Good luck!

And it seems to be a very bad first day with me for Posco. >9% in the red after not-that-bad numbers.

I never learn. Went up 20% since I sold. ![]()

Is there anyone else holding Comcast and scratching their head? I guess best is to stop the bleeding and sell..

Comcast bag holder here. (and CHTR bagholder too).

Still holding. I think they seem OK. Profitable, cheap, decent cash flows, buying back shares.

CHTR feels like a gamble, and maybe I’m missing something, or blinded by the cheap valuation, but heck, if they continue their rate of buy backs, they’ll have bought back all shares within 8 years.

Same same.

Kind of full a position, down a fair bit total return wise.

I don’t see any reason to sell.

YMMV.

I would buy more CMCSA if my risk management (position sizing) would not forbid me to buy more.

Mr. Market must be seeing something I certainly don’t see. Obviously, I hope Mr. Market does not see this as an invitation to punish me some more on Comcast … ![]()