The re-allocation based on time (in my example 7 months) means you don’t need market timing and may profit from Shannons demon. That simple plan makes you buy low and sell high, automatically.

1 Like

OK, I understand this concept of reallocation.

However, in my case it’s different. My USD based investment is now around 80% VT and 20% SCHD. The 20% SCHD is market timing: convert VT into SCHD when prices are high (i.e. now) and convert back (from SCHD to VT) when prices are low (i.e. after a crash). My long-term strategy is to only hold VT.

When not keep that allocation forever and rebalance every now and again?

Warnings that shadow banking defaults could double.

Historically debt was defaulted every 7 years or so, business as usual. Because even with the low interest it is impossible for money or debt (which is the same) to grow exponentially for longer periods of time. The compounding effect that is so nice for stockholders works only to a certain degree, there is a top. Now money has a top too and while a stock may slow down and stop it’s growth… debt is just defaulted.

Nice day to charge the rent for XNET in my gambling portfolio. Not many stocks make it over a year, but I charge them every year for their space in my portfolio by selling a bit. Today Xunlei presented good numbers, so charging rent and sell on good news. ![]()

It is very volatile stock but the gain after a year is like 36%; you always pay performance with volatility.

1 Like

Since you don’t mention divided and the initial prices seems to be 2, this is the high-risk portfolio. It’s a penny stock, but that yield is yummy.

I bought Xunlei at $5.02 a year ago and sold a part for $6.88 today, there was no dividend. It was no longer a penny stock when I bought it but then it did spend some time in penny-stock territory.

High was at $11, that is what I call volatility! I hope I’m able to hold this stock for a very long time, but China stocks have political angle; it could be over any minute.

I hold several stocks where the “rent” was already way bigger than what I did pay for them, but I keep enjoying further gains.

As always “Hold as long as possible… but not longer!”.

I try to publish a monthly recap of my strategies, but just found out that this thread is not even a month old.

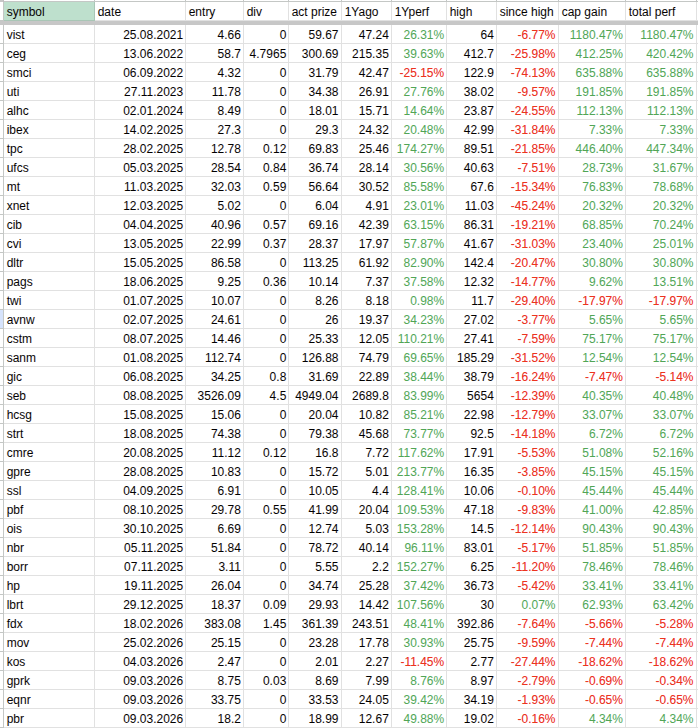

Here is an actual table with my holdings in the gambling strategy. For double positions the lower entry price and the latest buy date is displayed. I know, doing two lines for double positions would be probably more fair. At the moment SMCI and TPC are the only double positions. But then I do partial sells too and ignore them completely in this table:

Note: I did sell some XNET in pre-market today, at the open the gain will rise I suppose. The displayed prices are from the googlefinance function in google calc.

2 Likes

Wow, of this years buys only Petro Brasil is in the green. The penny stock Kosmos Energy (KOS) did push out new shares, hate when that happens. In German this is called “watering down” and I wanted oil, not water!

But then, YTD the strategy is 18.55% in the green already, that is almost too beautiful to be true, to last a whole year. As the Spaniards say “Bonito día, ya veras que viene alguien y te lo jode!”.

Looking at ICTax, I see that SCHD has a taxable dividend yield of 3.79%. VT only has 1.83%. I’m therefore paying higher taxes on SCHD.

As I said, dividends are tax-inefficient but dividend paying companies are less risky.

VT is the holy grail of all the youngster investors, because Mr. Bogle is telling them since decades that they cannot do better. But then Mr. Bogle makes a lot of money with those ETF. And yes, you can easily do better. You just have to switch off emotions, but not your brain.

VT brags about its 10’000 stocks, but that means you invest only very little money in a potential future high flyer. And the market cap based distribution puts 16%(!) into NVDA, AAPL, MSFT, AMZN and GOOG(L). What is left is distributed to the other 9995 companies, leaving only cents or even less to the companies that will rise because it is all already in the companies that did rise. The risk is enormous. I wouldn’t touch the holy grail with gloves!

SCHD in comparison uses a sector and position limit when position sizing. The 100 stocks are selected in a purely mechanical way, very similar to my methods.

2 Likes

I had no strategy on spending money when I retired at 52, that changed 2 years later when I got married! I just sell shares as needed, annual spending is about 200% of my last earnings in 2014 after tax, this is under 4% of capital so my money should not run out in my lifetime.

4 Likes

is that when you delegated the spending? ![]()

I’m keen to know more..

Some basic questions;

- These dividends are pre-infation so it’s not net. So, 3% before tax and inflation, means 1.5% net. How did you get 11.6%?

- When down market come (and its will) ,these dividends will fall. Are you factoring it?

Thanks

Yes please.

Super interested

- I think you mean the total performance. That is dividends plus capital gains minus tax minus debt interest (if debt). It is performance per year, eXtended Internal Rate of Return (XIRR), use the XIRR function in google calc. If you want the growth rate net of inflation you just deduct the yearly inflation for the same period from this number. I do calculate the carry premium too, which is dividends + market dividends - tax - debt interest.

- There were 4 bear markets since I started in 2014. They are included in the performance numbers which exactly now are for the dividend strategy 11.12% per year since 2014 (14% since 2020) and for the gambling strategy 28.77% per year since 2020.

I did describe the why, the how and then the complete rules for the dividend strategy earlier in this thread:

Simply stock trading - #20 by cubanpete

What you call “down markets” are the point where you can make a big difference by using mechanical strategies. Rise the risk when everybody else takes out risk! Buy low and sell high. Buy low, even on credit as I do. But don’t ignore the risks, never. As I said, in my gambling strategy I take very big risks. I can do that because I can stand to lose everything. Don’t do this at home if you are not absolutely sure you can stand this risk!

The question of @Arielt11 may be worth some further digging.

TLDR: XIRR is the correct method to measure performance, but doesn’t include risk.

Everybody lies

If you have read the excellent book How to lie with statistics, you know there are at least 3 different forms of average that whoever publishes it can use to his advantage: mean, median and mode. Later I explain why measuring the financial performance of a stock portfolio needs a bit more.

“The average man does not get pleasure out of an idea because he thinks it is true; he thinks it is true because he gets pleasure out of it.” ~ H. L. Mencken

But first to the averages. My mean average in the gambling strategy is 28.71%. Median average is 22.88% and mode is the same, 22.88% (when doing 10% steps it is 20-30%). All those numbers are rubbish, because they don’t take into account how long how much of the investment was active, how much money was added and how much money taken out.

How much does time weight?

To measure a portfolios performance many funds use time-weighted return. That ignores in- and outflows. But then funds have little control over in- and outflows. But private investors do and therefor should not use time weighted return as measurement.

Money weights more!

I use Money weighted return, taking into account all in- and outflows and the time the money was invested. This number is the interest you would have gotten in a bank account and I think it is the only relevant number for performance.

To calculate this number you can use a function in your preferred calc sheet. In google calc the function is called XIRR for eXtended Internal Rate of Return.

Risky business

Now we have the total performance number. That does say how much money you pocket, but it doesn’t say much about risk. There are several formulas to include risk and on a risk adjusted viewpoint the dream performance does not look that good. I calculated the Sharpe ratio over yearly data because I did not store the daily data. The rate is 1.13. Not that bad, but not exceptionally good. And the long term of 1 year for measuring volatility is bad, daily volatility may be more accurate and would probably result in a much worse Sharpe ratio.

Sorry, no magic involved.

So no, I am not a magician. I use standard methods and add the maximum risk possible for me, which is a lot. I suppose it is more than 99% of investors can stand, because I could lose everything in the gambling strategy and continue my life without any changes.

Under the bridge… (Red Hot Chili Peppers)

The risk is one of the biggest problems for private investors. Actually not the risk, but one’s plan once the risk does it’s damage. If you don’t have a plan you will be lost. Sleepless nights and one investing error after the other can wipe out everything you own! Our brain is just not made for this kind of situation.

For me the only thing that helps is a completely mechanical plan. It includes in any situation what to do, exact trading instructions. The most important part is probably what to do in a bear market. There the difference is made.

1 Like

HF, high frequency or hedge fund?